The concept of the “middle class” is one of the most discussed and often debated socio-economic identifiers in modern society. It represents an aspirational benchmark for many, a descriptor of economic stability and opportunity, yet its precise definition remains elusive. Is it solely about income? Or does it encompass a broader set of lifestyle indicators, assets, and future prospects? Understanding how much income is required to be considered middle class is not a straightforward calculation but rather a nuanced exploration of economic data, geographic realities, and personal financial health. This article delves into the various facets that define the middle class, the income thresholds often associated with it, and the financial strategies crucial for maintaining or achieving this status.

Defining the Middle Class: More Than Just a Number

The middle class is often seen as the backbone of an economy, representing a significant portion of the population that enjoys a certain level of financial security and upward mobility. However, pinpointing the exact income range for this group is surprisingly complex, varying based on the source, methodology, and even the cultural context.

The Elusive Definition: Why “Middle Class” Isn’t Fixed

One of the primary challenges in defining the middle class is its inherent fluidity. There isn’t a universally accepted, static income figure that applies across all demographics and locations. Historically, the middle class embodied a set of shared values and aspirations: homeownership, reliable employment, access to quality education and healthcare, and the ability to save for retirement and emergencies. While income is a critical component, these qualitative factors often play a significant role in how individuals perceive their own middle-class status. Sociologists and economists alike grapple with the subjective nature of this designation, often relying on relative income measures rather than absolute figures.

Income Brackets: A Starting Point

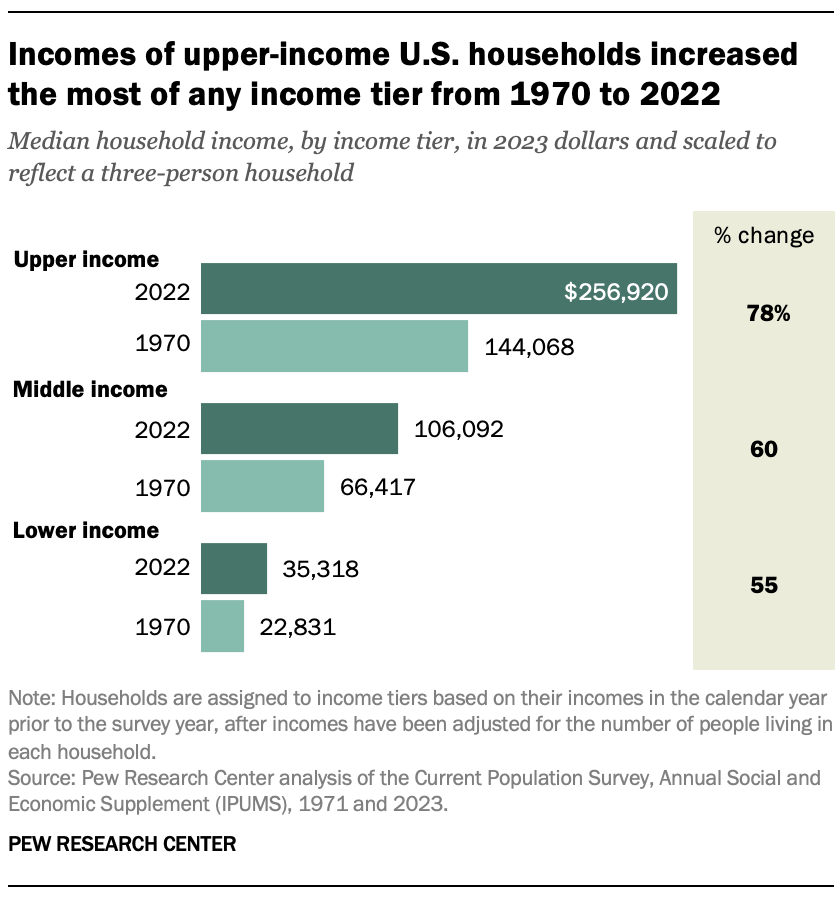

Despite the complexities, various research institutions and government agencies attempt to quantify middle-class income levels, typically by looking at national median income. One of the most widely cited sources is the Pew Research Center, which defines middle-income households as those earning between two-thirds and double the national median household income. The U.S. Census Bureau also provides data, often breaking down income distribution into quintiles.

For example, if the national median household income is $70,000, then a middle-class household, according to Pew’s definition, would generally earn between approximately $46,667 (2/3 of $70,000) and $140,000 (2 times $70,000). These figures are adjusted annually and vary significantly depending on the year and specific economic conditions. It’s crucial to remember that these are national averages and serve only as a baseline. They do not account for critical factors like household size or the dramatically differing costs of living across various regions.

Beyond Income: Lifestyle and Aspirations

While income provides a necessary framework, the middle class experience is undeniably shaped by lifestyle indicators and aspirations. For many, being middle class means more than just earning a certain salary; it implies:

- Homeownership: Often considered a cornerstone of middle-class wealth accumulation and stability.

- Education: The ability to afford higher education for oneself or one’s children without incurring debilitating debt.

- Healthcare: Access to affordable and comprehensive health insurance and medical care.

- Retirement Security: The ability to save adequately for a comfortable retirement.

- Financial Cushion: Having an emergency fund to cover unexpected expenses and maintain financial stability during unforeseen circumstances.

- Leisure and Discretionary Spending: The capacity to afford vacations, dining out, and other non-essential activities that contribute to quality of life.

These elements collectively paint a picture of economic security and social mobility that goes beyond mere earnings, highlighting the qualitative aspects often associated with middle-class life.

The Shifting Sands of Middle-Class Income Thresholds

The static national averages fail to capture the dynamic nature of economic realities across a vast and diverse country. What constitutes a middle-class income in one area might be considered poverty in another, or wealth in a third.

Geographical Variations: Cost of Living Differences

Perhaps the most significant variable impacting middle-class income thresholds is geography. The cost of living varies wildly from one metropolitan area to another, and even between rural and urban regions within the same state. A $100,000 household income in San Francisco, California, for instance, would likely provide a significantly lower standard of living than the same income in Topeka, Kansas, or Little Rock, Arkansas. Housing, transportation, and local taxes are major contributors to these disparities. Consequently, an income range that defines middle class in a high-cost-of-living area will be substantially higher than in a low-cost area. Organizations like the Department of Housing and Urban Development (HUD) often publish area median income (AMI) data, which offers a more localized perspective on income brackets.

Household Size Matters

Another critical adjustment factor is household size. A single individual earning $70,000 per year will have a much higher per capita income and potentially a higher standard of living than a household of four (two adults, two children) earning the same $70,000. Many definitions of middle-class income, especially those provided by research centers like Pew, already account for household size, adjusting the income ranges accordingly. Generally, larger households require a higher income to maintain the same middle-class standard of living as smaller households.

The Impact of Inflation and Cost of Living

Over time, inflation steadily erodes purchasing power. The cost of essential goods and services – housing, food, healthcare, education – has risen significantly faster than wages for many decades. This “cost of living squeeze” means that an income that afforded a comfortable middle-class lifestyle 20 or 30 years ago might no longer be sufficient today, even after adjusting for general inflation. This ongoing challenge necessitates higher nominal incomes to achieve the same real purchasing power, constantly shifting the goalposts for middle-class status.

Generational Differences

The economic landscape has also changed dramatically across generations. Younger generations, particularly Millennials and Gen Z, face different economic realities than their Baby Boomer and Gen X predecessors. Higher student loan debt, a more competitive job market, delayed homeownership, and rising healthcare costs mean that achieving middle-class financial stability can be a more arduous journey, often requiring higher absolute incomes and more sophisticated financial planning than in previous eras.

Key Financial Indicators of Middle-Class Status

Beyond raw income, true middle-class stability is often characterized by a healthy financial picture across several key indicators. These are the markers of sound financial health that enable individuals and families to weather economic storms and build long-term wealth.

Debt-to-Income Ratios

A defining characteristic of financial health, particularly for the middle class, is a manageable debt-to-income (DTI) ratio. This ratio compares your monthly debt payments to your gross monthly income. While some debt, like a mortgage or student loans, is common and often necessary, excessive consumer debt (credit cards, personal loans) can quickly erode a household’s financial stability, regardless of income level. A low DTI indicates that a significant portion of income is available for savings, investments, and discretionary spending, rather than being consumed by debt servicing.

Savings and Investments

A robust emergency fund, typically covering 3-6 months of essential living expenses, is a hallmark of middle-class financial prudence. Beyond that, consistent savings for short-term goals (e.g., a down payment on a car, a vacation) and long-term investments for wealth building (e.g., brokerage accounts, mutual funds, real estate) are crucial. The ability to consistently save and invest, rather than living paycheck to paycheck, is a strong indicator of financial health and the capacity to build intergenerational wealth.

Homeownership and Asset Accumulation

For many, homeownership remains a quintessential symbol of middle-class status and a primary vehicle for asset accumulation. A home often represents the largest single asset for middle-income families, providing not only shelter but also a potential source of equity and long-term wealth growth. Beyond real estate, accumulating other assets like retirement accounts, investment portfolios, and even valuable personal property contributes to a household’s net worth and overall financial security.

Retirement Preparedness

Planning for retirement is a critical component of middle-class financial responsibility. This typically involves contributing consistently to tax-advantaged accounts such as 401(k)s, 403(b)s, and Individual Retirement Accounts (IRAs). The ability to save adequately for retirement indicates a foresight and discipline that allows individuals to maintain their standard of living well into their later years, rather than relying solely on Social Security or other government programs.

Challenges and Strategies for Middle-Class Financial Stability

The road to achieving and maintaining middle-class status is fraught with challenges, yet proactive strategies can significantly bolster financial resilience.

The Squeeze: Stagnant Wages vs. Rising Costs

Many middle-income households face a persistent squeeze: wages have not kept pace with the soaring costs of essential goods and services. Healthcare premiums and out-of-pocket expenses continue to climb, higher education tuition costs seem to have no ceiling, and housing prices in desirable areas are often out of reach for many. This economic reality necessitates careful financial planning and often creative solutions to bridge the gap.

Building Financial Resilience

Creating an emergency fund is the first line of defense against unexpected financial setbacks. Beyond that, diversifying income streams, perhaps through a side hustle or investing in skills that command higher wages, can provide an additional layer of security. Financial resilience also involves having appropriate insurance coverage (health, life, disability, home) to protect against catastrophic losses.

Smart Budgeting and Expense Management

A meticulous budget is the cornerstone of effective money management. Tracking income and expenses, identifying areas for savings, and consciously making spending choices are vital. Automated savings transfers, debt reduction strategies, and avoiding unnecessary consumer debt are practical steps that empower middle-class households to take control of their finances and direct their money towards their goals.

Investing for Growth

For middle-class households, simply saving money in a low-interest bank account is often not enough to keep pace with inflation or achieve significant wealth growth. Investing in diversified portfolios of stocks, bonds, and mutual funds, even with modest amounts, allows money to grow over time through compounding. Understanding basic investment principles and utilizing employer-sponsored retirement plans are crucial steps.

Future-Proofing Your Finances

The economic landscape is constantly evolving. Future-proofing finances involves continuous learning, adapting to new economic realities, and remaining flexible. This might include investing in one’s own education and skills, staying informed about market trends, and periodically reviewing and adjusting financial plans to ensure they align with changing life circumstances and economic conditions.

The Broader Economic Implications of a Robust Middle Class

The health of the middle class is not just a personal finance issue; it has profound implications for the broader economy and society.

Economic Inequality

A shrinking or struggling middle class often correlates with rising economic inequality. When the middle class is squeezed, the gap between the rich and the poor widens, which can lead to social unrest, reduced opportunities, and a less stable society. A strong middle class, conversely, acts as a stabilizing force, bridging the income divide.

Consumer Spending and Economic Health

The middle class traditionally drives a significant portion of consumer spending, which is a key engine of economic growth. When middle-income households have disposable income, they spend it on goods and services, supporting businesses and creating jobs. A weakened middle class can lead to reduced consumer demand, slowing economic expansion.

Policy Considerations

The challenges faced by the middle class often prompt policy discussions around issues like progressive taxation, affordable healthcare initiatives, student loan reform, housing subsidies, and access to quality education. Policymakers frequently examine the state of the middle class as an indicator of overall economic well-being and a guide for legislative priorities aimed at fostering a more equitable and prosperous society.

In conclusion, defining “how much income for middle class” is a complex, multi-faceted endeavor that extends beyond a simple numerical threshold. It involves considering national and local income data, household size, the ever-increasing cost of living, and a host of qualitative factors related to lifestyle, assets, and future security. While the path to middle-class stability can be challenging, understanding these dynamics and adopting sound financial strategies are essential for individuals and families striving to achieve and maintain this vital economic status. Ultimately, a robust and thriving middle class is not just a personal goal but a collective necessity for a healthy and prosperous society.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.