Understanding your Social Security contributions is a crucial aspect of personal finance, offering a clear picture of your potential future retirement income. The Social Security Administration (SSA) tracks every dollar you’ve paid into the system throughout your working life. This accumulated amount forms the basis of your future retirement, disability, and survivor benefits. Knowing your earnings history and estimated benefits empowers you to make informed financial planning decisions, ensuring you can adequately prepare for retirement and other life events.

Accessing Your Social Security Statement: Your Personal Earnings Record

The primary way to determine how much you’ve paid into Social Security is by accessing your official Social Security Statement. This document, provided by the Social Security Administration (SSA), is a personalized summary of your earnings history and an estimate of your future benefits. It’s an invaluable tool for financial planning, allowing you to track your progress towards retirement and understand what to expect from the program.

Creating Your “my Social Security” Account

The most convenient and secure method to access your Social Security Statement is by creating a personal account on the SSA’s official website. This account provides round-the-clock access to your earnings record, benefit estimates, and other important information.

- Eligibility and Setup: To create an account, you’ll need to provide some personal information, including your Social Security number (SSN), date of birth, and mailing address. You’ll also be asked to create a username and password and set up security questions. The SSA employs robust security measures to protect your personal data.

- Navigating Your Account: Once logged in, you’ll find a dashboard that clearly displays your earnings history, broken down by year. For each year, you’ll see the amount of income subject to Social Security taxes. This is the “gross” amount of earnings that contribute to your lifetime earnings record.

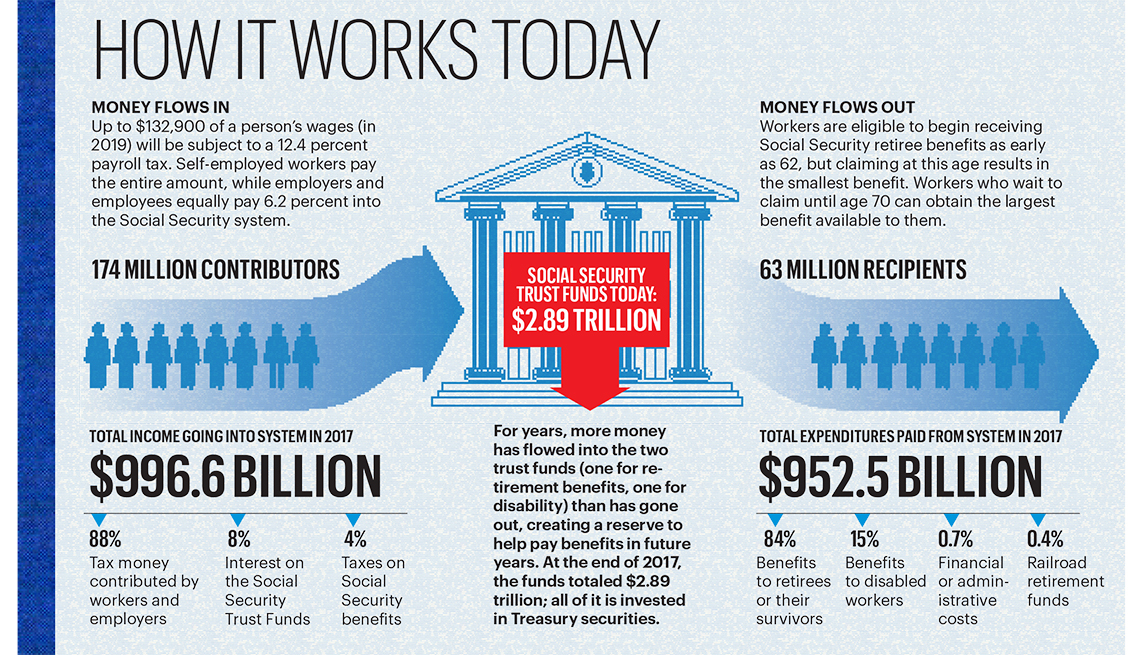

- Understanding Your Contribution: The statement will also show how much has been paid into Social Security on your behalf for each year. This is typically 12.4% of your earnings, split between you (7.65% withheld from your paycheck, including Medicare tax) and your employer (matching 6.2% for Social Security and 1.45% for Medicare). Self-employed individuals pay the full 15.3% (12.4% for Social Security and 2.9% for Medicare). Your “my Social Security” account will primarily focus on the Social Security portion of your contributions for benefit calculation purposes.

Requesting a Paper Statement by Mail

While creating an online account is highly recommended, individuals who prefer not to use online services or are concerned about online security can still request a paper Social Security Statement by mail.

- The Process: This typically involves filling out a specific form, such as the SSA-7004 (Your Social Security Statement). You can usually download this form from the SSA website or request it by calling the SSA directly.

- Information Required: You will need to provide your SSN, name, date of birth, and mailing address. The SSA will then process your request and mail a paper statement to you. This process can take longer than accessing your statement online.

- Limitations: It’s important to note that paper statements are generally provided to individuals who are age 60 or older and not yet receiving benefits. The SSA has shifted towards online access for most beneficiaries to streamline services and reduce paper waste.

Deconstructing Your Social Security Statement: Key Information and Insights

Your Social Security Statement is more than just a number; it’s a detailed record that offers profound insights into your financial future. Beyond simply showing your total contributions, it provides estimates of future benefits and crucial information about your earnings history.

Your Lifetime Earnings Record: The Foundation of Your Benefits

The most fundamental piece of information on your Social Security Statement is your lifetime earnings record. This is a year-by-year breakdown of the income on which you paid Social Security taxes.

- How Earnings are Credited: Social Security credits are earned based on your earnings each year. For 2024, you earn one credit for every $1,730 in earnings, up to a maximum of four credits per year. You generally need 40 credits (equivalent to about 10 years of work) to be eligible for retirement benefits.

- The Importance of Accuracy: It is vital to review your earnings record for accuracy. If you notice any discrepancies, such as missing years or incorrect amounts, you should contact the SSA immediately to have them corrected. Errors can significantly impact your future benefit amount.

- Maximum Taxable Earnings: Social Security taxes are only applied up to a certain income limit each year. This limit, known as the maximum taxable earnings, is adjusted annually. Earnings above this threshold do not contribute to Social Security taxes or benefits. Your statement will reflect this, showing your actual earnings and the portion that was subject to Social Security taxes.

Estimating Your Future Retirement Benefits

One of the most significant features of your Social Security Statement is the projection of your future retirement benefits. The SSA uses your earnings history to calculate an estimated monthly benefit at different retirement ages.

- Primary Insurance Amount (PIA): The PIA is the amount you would receive if you retire at your full retirement age. Your PIA is calculated based on your average indexed monthly earnings (AIME) over your 35 highest-earning years, adjusted for inflation.

- Benefit Estimates at Different Ages: Your statement will typically show estimates for three scenarios:

- Retiring at your Full Retirement Age (FRA): This is the age at which you are eligible to receive 100% of your calculated benefit. Your FRA depends on your birth year, generally ranging from 66 to 67.

- Retiring at Age 62: This is the earliest age you can claim Social Security benefits. However, claiming early will result in a permanently reduced benefit amount.

- Retiring at Age 70: Delaying your retirement benefits beyond your FRA can significantly increase your monthly payments due to delayed retirement credits. The maximum increase is achieved by waiting until age 70.

- Factors Influencing Estimates: It’s crucial to remember that these are estimates. Your actual benefit amount will depend on your earnings in the years leading up to your retirement, changes in Social Security laws, and the accuracy of the earnings reported on your statement.

Maximizing Your Social Security Benefits: Strategic Planning for Retirement

While your Social Security Statement provides valuable information about your contributions and estimated benefits, it also serves as a springboard for strategic financial planning. Understanding how to maximize your benefits can lead to a more comfortable and secure retirement.

The Impact of Continued Earnings on Your Benefit Amount

Your continued earnings throughout your working life have a direct and significant impact on your Social Security benefit.

- Replacing Lower-Earning Years: As you earn more in later years, these higher earnings will replace some of your lower-earning years in the calculation of your 35 highest-earning years. This can effectively increase your AIME and, consequently, your PIA.

- Earning More Credits: Even if you have already accumulated the 40 credits needed for eligibility, earning more credits can still be beneficial. The more credits you have, and the higher your earnings associated with those credits, the stronger your overall earnings record will be.

- The 35-Year Rule: The SSA uses your 35 highest-earning years to calculate your retirement benefit. If you have fewer than 35 years of earnings, the years with zero earnings will be averaged in, significantly lowering your benefit. Therefore, continuing to work and earn income can help you replace those zero or low-earning years.

Strategic Retirement Ages: When to Claim Your Benefits

The decision of when to claim your Social Security benefits is one of the most critical financial choices you will make regarding your retirement. This decision has a profound and lasting impact on your monthly income.

- Early Retirement (Age 62): Claiming at age 62 will result in a permanent reduction in your monthly benefit. This reduction is substantial, and the longer you claim before your full retirement age, the greater the reduction will be. This option might be suitable for individuals with health issues or those who need income sooner, but it requires careful consideration of the long-term financial implications.

- Full Retirement Age (FRA): Reaching your FRA ensures you receive 100% of your calculated benefit. This is often the most straightforward and recommended age for many individuals, providing a stable income stream without penalties.

- Delayed Retirement (Up to Age 70): For every year you delay claiming benefits beyond your FRA, you earn delayed retirement credits, which increase your monthly benefit by a certain percentage. This can be a very attractive strategy for those who can afford to wait, as it provides a higher guaranteed income for the rest of their lives. This is particularly beneficial for individuals who anticipate living a long life, as the increased benefits can accumulate significantly over time.

Understanding Spousal and Survivor Benefits

Social Security doesn’t just provide benefits based on your individual contributions. It also offers crucial protections for spouses and survivors.

- Spousal Benefits: If you are married, you may be eligible for spousal benefits. A spouse can receive up to 50% of the worker’s primary insurance amount (PIA) if they claim benefits at their full retirement age. If the spouse claims earlier, their benefit will be reduced. To be eligible, the worker must be receiving their own retirement benefits.

- Survivor Benefits: If a worker passes away, their surviving spouse, minor children, or dependent parents may be eligible for survivor benefits. The amount of the survivor benefit is a percentage of the deceased worker’s PIA and varies depending on the survivor’s age and relationship to the worker. This is a vital safety net for families.

- Coordination with Your Own Benefits: When considering spousal or survivor benefits, it’s important to understand how they interact with your own retirement benefits. The SSA has rules to ensure you receive the most advantageous benefit available to you, which may be your own benefit, a spousal benefit, or a survivor benefit.

By actively engaging with your Social Security Statement and understanding the factors that influence your benefits, you can make informed decisions that contribute to a secure and prosperous financial future. Regularly reviewing your statement, planning your retirement age strategically, and understanding all available benefit options are essential steps in maximizing the value of your Social Security contributions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.