Determining the exact worth of a global behemoth like Google—legally known as Alphabet Inc.—is a task that requires navigating through complex financial statements, market sentiment, and the intrinsic value of digital real estate. As one of the few elite members of the “Trillion Dollar Club,” Alphabet represents a cornerstone of the modern global economy. However, “worth” is a multifaceted term. To a retail investor, it is the share price; to an institutional analyst, it is the enterprise value; and to the broader market, it is the potential for future cash flows.

Understanding how much Google is worth today requires a deep dive into its financial architecture, its diverse revenue streams, and the macroeconomic variables that influence its market capitalization.

The Financial Pillars of Google’s Net Worth

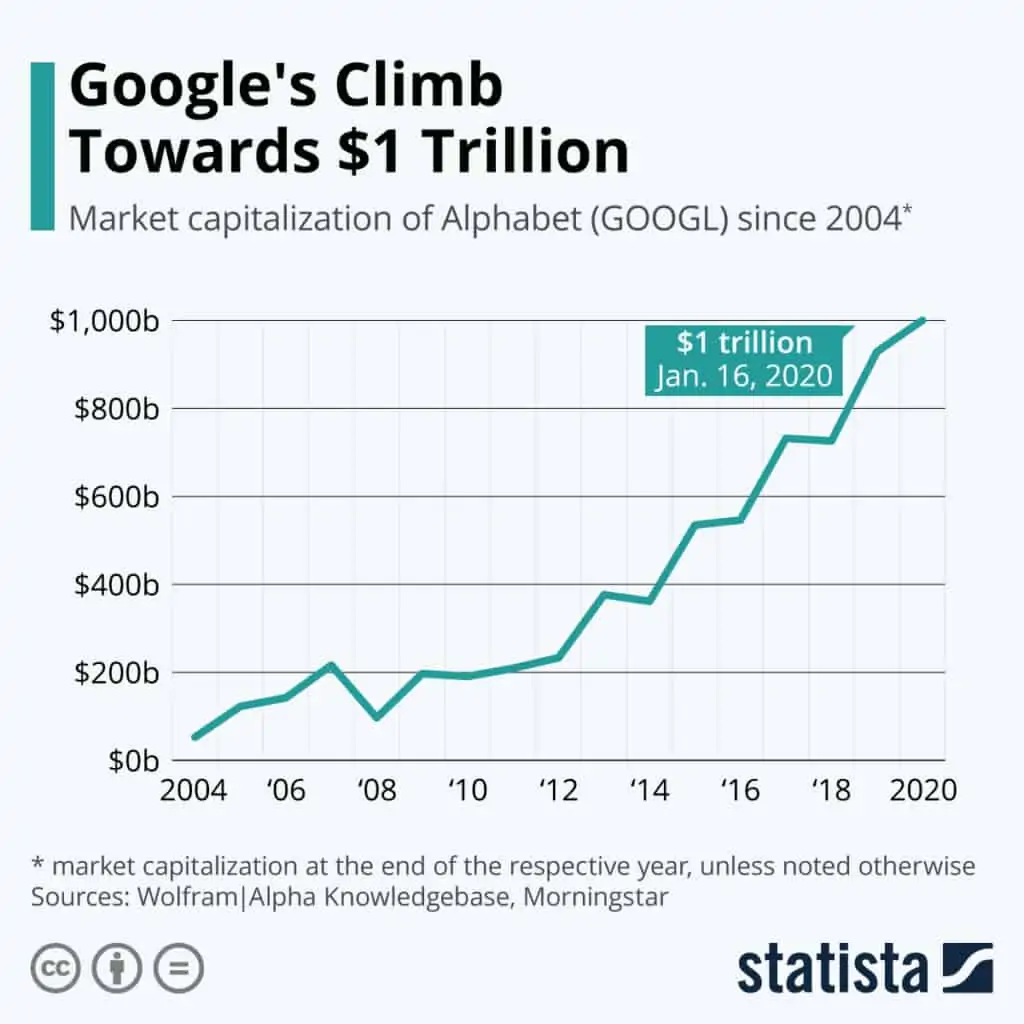

When discussing the worth of a public company, the most common metric used is market capitalization. This is calculated by multiplying the total number of outstanding shares by the current market price of a single share. Alphabet Inc. operates with a dual-class share structure (GOOGL and GOOG), and its total market cap has historically fluctuated between $1.5 trillion and $2 trillion.

Understanding Market Capitalization vs. Enterprise Value

While market capitalization provides a snapshot of equity value, “Enterprise Value” (EV) is often considered a more accurate measure of a company’s total worth. EV includes market cap but adds total debt and subtracts cash and cash equivalents. Alphabet is unique because of its massive cash reserves—often exceeding $100 billion. This “fortress balance sheet” means that Google’s enterprise value is actually lower than its market cap, signifying that the company is effectively “self-funded” and carries significantly less risk than competitors burdened by high leverage.

Revenue Streams: The Power of Search and AdSense

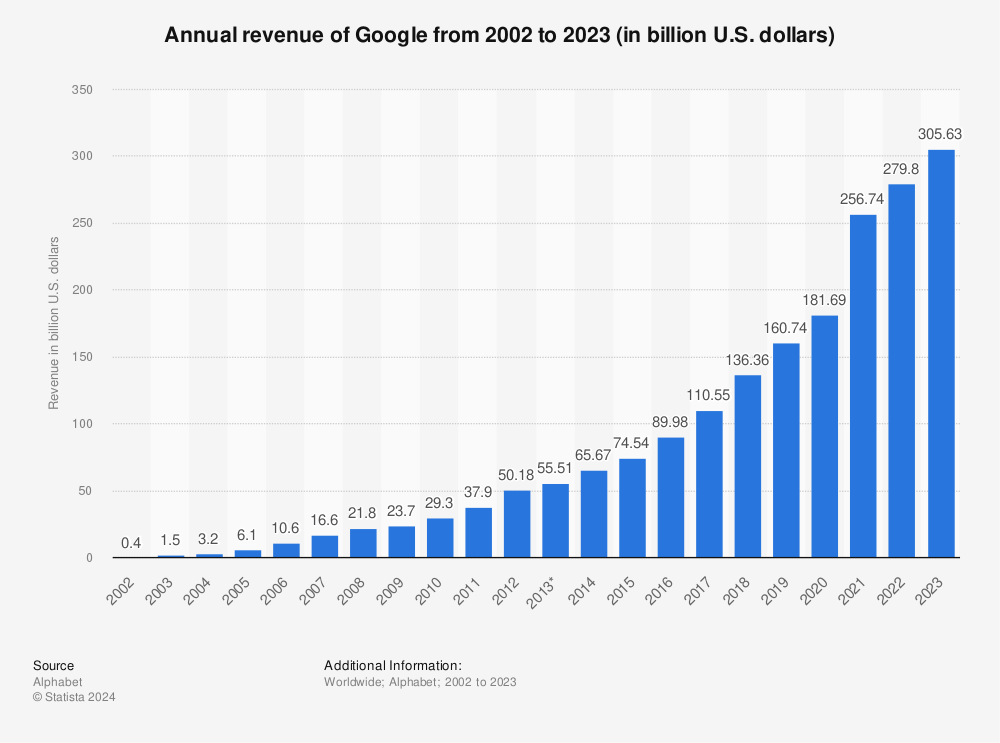

The bedrock of Google’s valuation is its advertising ecosystem. Google Search remains the most profitable piece of digital real estate in history. Unlike social media platforms that rely on passive scrolling, Search captures “intent.” When a user types a query, they are often looking to solve a problem or make a purchase, making those ad slots incredibly valuable.

The Google Network (AdSense) further extends this reach, placing ads on millions of third-party websites. Together, these segments generate over 75% of Alphabet’s total revenue. The consistent, high-margin cash flow from advertising provides the capital necessary for Google to invest in more speculative ventures, effectively acting as the engine that drives the entire corporate machine.

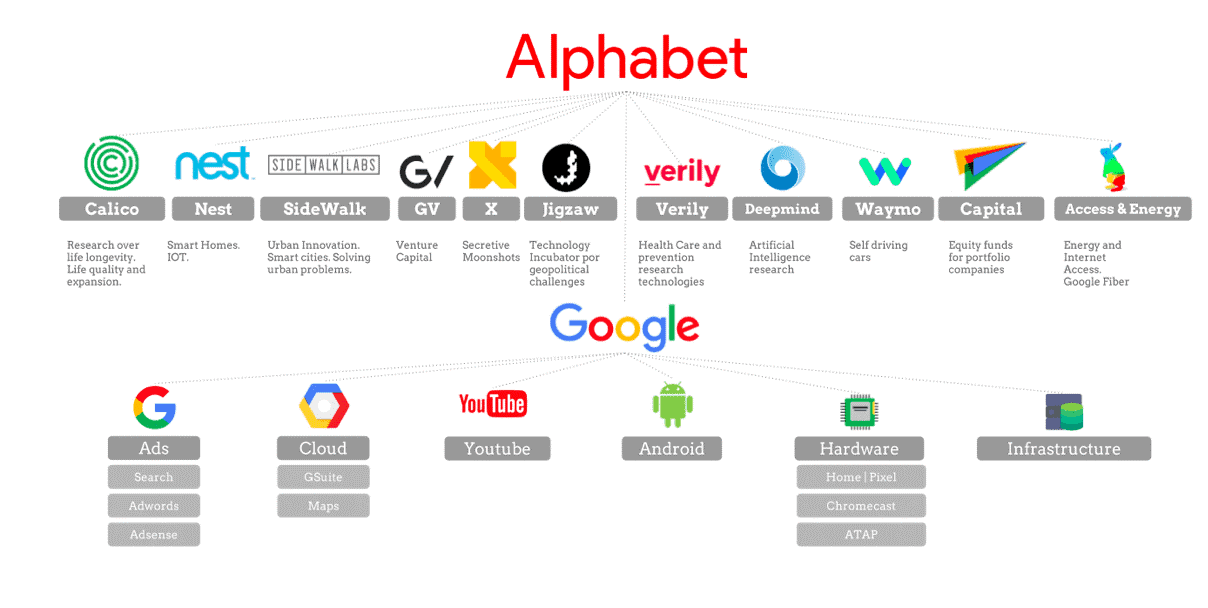

Beyond Search: The Value of Alphabet’s Diversified Portfolio

To understand why Google is worth nearly $2 trillion, one must look beyond the search bar. Alphabet has successfully diversified into sectors that are expected to dominate the next decade of technological and economic growth.

Google Cloud: The High-Growth Engine

For years, Google Cloud was a loss-leader, trailing behind Amazon Web Services (AWS) and Microsoft Azure. However, recent fiscal years have seen Google Cloud reach a turning point of profitability. Currently generating tens of billions in annual revenue, the Cloud division is valued by many analysts as a standalone entity worth several hundred billion dollars. Its value lies in the enterprise shift toward digital transformation and the infrastructure required to host modern AI applications.

YouTube’s Standalone Valuation Potential

YouTube is often cited as one of the greatest acquisitions in corporate history. Purchased for $1.65 billion in 2006, YouTube now generates upwards of $30 billion in annual ad revenue alone, not including its subscription services like YouTube Premium and YouTube TV. If YouTube were a standalone company, financial analysts estimate its valuation could exceed $400 billion. Its worth is tied to its dominance in the attention economy, serving as both a search engine and a primary entertainment hub for younger demographics.

“Other Bets”: Speculative Value in Waymo and Verily

Alphabet’s “Other Bets” segment includes moonshot projects like Waymo (autonomous driving) and Verily (life sciences). While these divisions currently operate at a loss, they represent the “option value” of the company. For example, Waymo is a leader in the robotaxi space. If autonomous driving becomes a standardized global utility, Waymo alone could eventually be worth as much as the core search business today. Investors bake this future potential into the current stock price, contributing to the overall “worth” of the parent company.

Key Financial Metrics and Valuation Ratios

In the world of finance, worth is relative. To determine if Google is “expensive” or “cheap,” investors look at valuation multiples compared to historical averages and industry peers.

P/E Ratio and PEG Ratio: Assessing Fair Value

The Price-to-Earnings (P/E) ratio is a primary tool for measuring valuation. Alphabet typically trades at a P/E ratio between 20x and 30x. While this is higher than the average S&P 500 company, it is often lower than peers like Microsoft or Amazon.

The Price/Earnings-to-Growth (PEG) ratio is perhaps a more telling metric for Google. Because Alphabet continues to grow its bottom line at a double-digit rate, its PEG ratio often suggests that the company is undervalued relative to its growth potential. This “valuation gap” is a frequent topic of discussion among value investors who believe the market consistently underestimates Google’s durability.

Free Cash Flow: The Engine of Stock Buybacks

A company’s true worth to its shareholders is found in its Free Cash Flow (FCF). Alphabet generates staggering amounts of FCF—often over $60 billion annually. This liquidity allows the company to engage in massive share buyback programs. By reducing the number of shares outstanding, Alphabet increases the “worth” of each remaining share, effectively returning value to investors without the tax implications of a traditional dividend (though Alphabet did recently initiate its first dividend in 2024).

External Factors Influencing Google’s Worth

No company exists in a vacuum. External economic and legal forces play a significant role in determining how much Google is worth on any given day.

The Macroeconomic Environment and Interest Rates

As a growth-oriented tech giant, Google’s valuation is sensitive to interest rates. When the Federal Reserve raises rates, the “discount rate” applied to future earnings increases, which can lower the present value of the stock. Additionally, Google’s primary revenue source—advertising—is cyclical. During economic downturns, corporations slash marketing budgets, which can lead to temporary dips in Google’s valuation.

Regulatory Risks and Antitrust Lawsuits

Perhaps the greatest threat to Google’s worth is regulatory intervention. The Department of Justice (DOJ) and the European Union have levied numerous antitrust lawsuits against the company, alleging monopolistic behavior in search and advertising technology. A court-ordered breakup of Alphabet—such as forcing the sale of the Chrome browser or the AdTech business—could fundamentally alter the company’s valuation. Paradoxically, some analysts argue that a breakup might “unlock” value, as the individual parts (YouTube, Cloud, Search) might be worth more separately than they are as a single conglomerate.

The Future Outlook: Investing in the Age of AI

The final component of Google’s worth is its future-proofing. In the current financial landscape, a company’s value is increasingly tied to its roadmap for Artificial Intelligence (AI).

AI Integration and Its Impact on Long-term Valuation

The emergence of generative AI posed an existential question: Will AI chatbots replace traditional search? Alphabet’s response—integrating Gemini (its proprietary LLM) across its ecosystem—is vital to maintaining its valuation. By evolving Search into a “Search Generative Experience” (SGE), Google aims to maintain its dominance in intent-based queries.

The market currently views Google’s AI capabilities as a double-edged sword. On one hand, AI increases the efficiency of its Cloud and Ad platforms, driving higher margins. On the other hand, the high capital expenditure (CapEx) required to build AI data centers pressures short-term cash flows. However, long-term investors generally agree that Google’s vast data moats and custom-built AI chips (TPUs) provide a competitive advantage that secures its multi-trillion-dollar valuation for the foreseeable future.

Conclusion: Summing Up the Value

So, how much is Google worth? Financially, it is a $2 trillion entity defined by an impenetrable advertising moat, a burgeoning cloud business, and a leadership position in the AI revolution. But beyond the numbers, Google’s worth is defined by its utility; it has become a fundamental infrastructure of the internet. While regulatory hurdles and macroeconomic shifts will cause the numbers to fluctuate, the underlying profitability and cash-generating power of Alphabet Inc. ensure that it remains one of the most valuable assets in the history of global business. For the investor, Google’s worth is not just a reflection of where it is today, but a bet on the digital future of the human race.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.