When navigating the world of personal finance, you will inevitably encounter situations where a standard personal check or a simple debit card swipe won’t suffice. Whether you are closing on a home, purchasing a used vehicle from a private seller, or paying a significant security deposit on a high-end rental, you will likely be asked for a cashier’s check.

Understanding the costs associated with this financial instrument—and the logistics of how to acquire one—is essential for managing your liquidity and ensuring your transactions proceed smoothly. While the fee for a cashier’s check might seem like a minor detail, it is a component of your broader banking relationship that reflects the value of the services you receive.

Breaking Down the Costs: What to Expect at Major Banks

The most direct answer to “how much for a cashier’s check” is that it typically ranges from $0 to $15, depending entirely on where you bank and what type of account you hold. Unlike money orders, which are often sold at post offices or retail stores for a couple of dollars, cashier’s checks are premium financial instruments issued and guaranteed by the bank itself.

Big Banks vs. Local Credit Unions

Traditional “Big Four” banks in the United States—such as JPMorgan Chase, Bank of America, Wells Fargo, and Citibank—generally sit at the higher end of the pricing spectrum. For a standard checking account holder, the fee for a single cashier’s check is usually $10 or $15.

In contrast, credit unions and smaller community banks often offer more competitive pricing. It is not uncommon for a credit union to charge between $2 and $5 for the service. Because credit unions are member-owned institutions, they frequently pass savings on to their members in the form of lower transactional fees. If you find yourself needing cashier’s checks frequently, the fee structure of your institution is a valid metric to consider when choosing where to keep your capital.

The Impact of Account Tiers on Fees

One of the most effective ways to avoid the cost of a cashier’s check altogether is through “relationship banking.” Most major financial institutions offer tiered account structures. If you maintain a premium or “gold” level account—usually defined by maintaining a high minimum balance (e.g., $10,000 to $25,000) or having a mortgage linked to the account—the bank will often waive the fee for cashier’s checks, money orders, and even wire transfers.

Before you head to the teller, check your account’s “Schedule of Fees” or mobile app. You may find that your specific account type entitles you to a certain number of free official checks per month. This is a small but notable perk of consolidating your assets within a single institution.

When and Why You Should Use a Cashier’s Check

It is important to distinguish why someone would demand a cashier’s check over a personal check. The primary reason is guaranteed payment. When you write a personal check, the recipient has no immediate way of knowing if the funds are actually in your account. If the check “bounces,” the recipient is left with a fee and no payment.

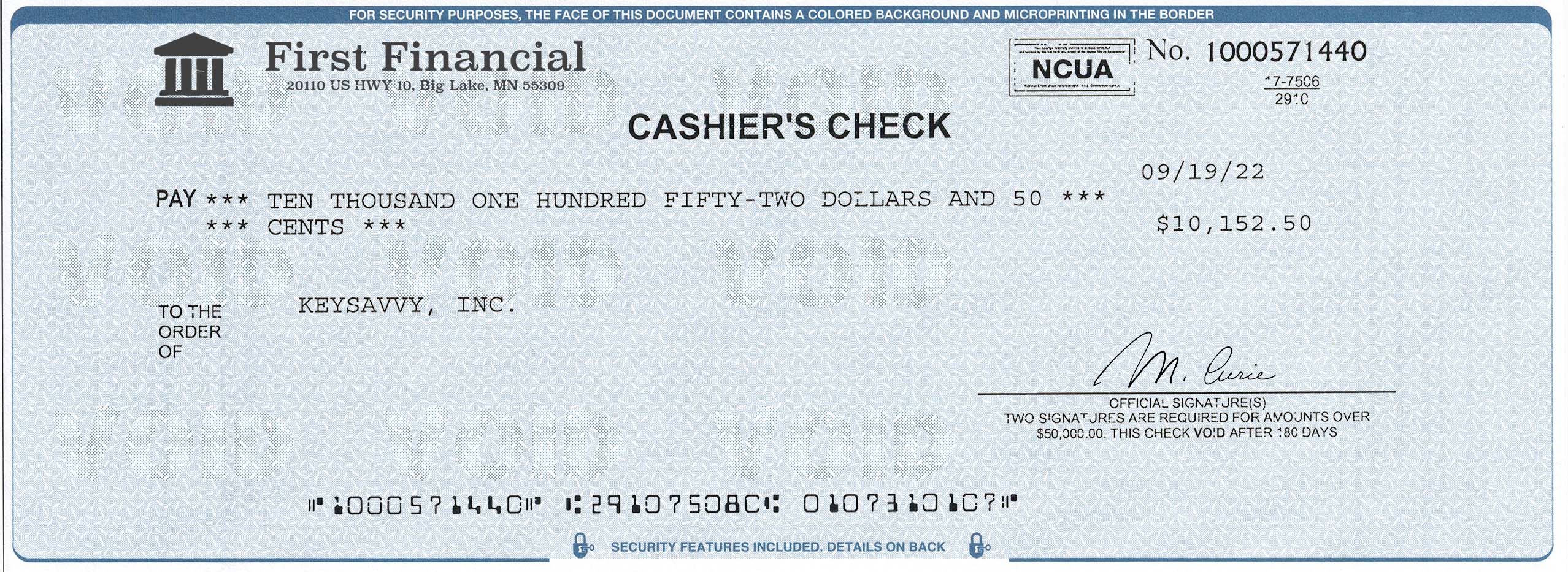

A cashier’s check, however, is drawn against the bank’s own funds. When the bank issues the check, they immediately withdraw the amount from your account and move it into their own internal coffers. Therefore, the check is backed by the credit of the financial institution, not the individual.

Real Estate and Large Private Purchases

In the real estate industry, “cleared funds” are a legal requirement for closing. Because a cashier’s check is considered as good as cash, it allows the title company or escrow agent to disburse funds immediately to the seller, the mortgage company, and the taxing authorities. Without this guarantee, the closing process could be delayed by several days while a personal check clears the banking system.

Similarly, if you are buying a car from a private individual, the seller will likely insist on a cashier’s check. It provides them with the security that the thousands of dollars promised for the vehicle will actually manifest in their account, allowing them to sign over the title with peace of mind.

Guaranteed Funds: The Seller’s Perspective

From a business finance perspective, accepting a cashier’s check mitigates the risk of “non-sufficient funds” (NSF). For large-scale transactions, the $10 or $15 fee paid by the buyer is a small price for the professional security it provides to the seller. It signals that the buyer is serious and has the liquid capital necessary to complete the deal.

How to Get a Cashier’s Check: A Step-by-Step Process

Securing a cashier’s check is more formal than simply writing a check from your own book. Because the bank is taking on the liability for the payment, they require a specific protocol to be followed.

Verification and Identification Requirements

To obtain a cashier’s check, you must go to a physical branch of a bank where you have an account. You will need to bring:

- Valid Government ID: A driver’s license or passport is required to verify your identity.

- The Payee’s Name: You must know exactly who the check is being made out to. Unlike a personal check, you cannot leave the “Pay to the Order Of” line blank or make it out to “Cash” in most instances.

- Available Funds: The full amount of the check, plus the fee, must be “available” in your account. This means that if you just deposited a large check from another source, you may have to wait for those funds to clear before the bank will issue a cashier’s check against them.

The teller will print the check with the recipient’s name and the exact amount, and it will be signed by a bank representative (hence the name “cashier’s” check).

Can You Get a Cashier’s Check Online?

While we live in an increasingly digital world, getting a cashier’s check online is still somewhat rare and depends on your bank’s capabilities. Some online-only banks (like Ally or Charles Schwab) allow you to request a cashier’s check through their website. They will then mail the check to your registered address or directly to the payee via overnight mail.

However, if you are in a rush—such as needing to close a deal this afternoon—the online route is usually too slow. In most cases, a cashier’s check is an “in-person” financial tool. If you do not have a physical bank branch nearby, you might need to look into wire transfers as a digital alternative.

Comparing Alternatives: Money Orders, Certified Checks, and Wires

If the $15 fee or the trip to the bank seems inconvenient, there are other financial tools available. However, they are not always interchangeable with a cashier’s check.

When a Money Order is Better

Money orders are generally used for smaller amounts, typically capped at $1,000 per order. They are much cheaper than cashier’s checks, often costing less than $2 at a grocery store or the Post Office. If you need to pay a utility bill or a small rent payment and don’t have a checking account, a money order is the way to go. However, for a $5,000 car purchase, a money order is usually not an option because of the low maximum limits.

Wire Transfers: Speed vs. Cost

A wire transfer is the fastest way to move money, often settling within hours. However, it is also the most expensive. Domestic wire fees typically range from $25 to $30, while international wires can exceed $50. If you are in a different state from the recipient, a wire transfer is more practical than mailing a physical cashier’s check, but you will pay a premium for that speed and convenience.

Certified Checks: The Middle Ground

A certified check is a personal check that the bank “certifies.” The bank stamps the check and verifies that the signature is genuine and that the funds are in the account. While similar to a cashier’s check, many banks have moved away from certified checks in favor of cashier’s checks because the latter is easier for their internal accounting to track.

Safety First: Preventing Cashier’s Check Fraud

Despite their reputation for being “as good as cash,” cashier’s checks are a frequent target for scammers. Because people trust them, they often lower their guard.

Common Red Flags in Check Scams

A common scam involves a buyer sending you a cashier’s check for more than the purchase price of an item you are selling. They will then ask you to wire back the “excess” funds. Days later, the bank discovers the cashier’s check was a sophisticated forgery. Because the bank is required by law to make funds available quickly, you might have already withdrawn and sent the “excess” money before the check is flagged as fake. Once it is flagged, the bank will deduct the full amount from your account, leaving you responsible for the loss.

Verifying the Legitimacy of a Check

If you receive a cashier’s check from someone you don’t know, do not rely solely on the fact that your bank “cleared” the funds. Take the extra step to verify the check. Look up the phone number of the issuing bank (don’t use the number printed on the check, as it could be fake) and call them to verify the check number and the amount. Most banks are happy to confirm if an official instrument was indeed issued by their branch.

In the landscape of personal finance, the cashier’s check remains a vital tool for significant life milestones. While the fee—whether it’s $5 or $15—is a small administrative cost, the security and guarantee it provides are invaluable. By understanding how to navigate these fees and the proper procedures for using these checks, you can ensure that your largest financial transactions are handled with the professional rigor they deserve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.