In the modern digital economy, the way we handle peer-to-peer (P2P) transactions has shifted from physical envelopes of cash to instantaneous digital transfers. Cash App, owned by Block, Inc., has emerged as a titan in the financial tools sector, offering users a seamless way to send, receive, and invest money. However, for many users, the convenience of the platform comes with a recurring question: how much does it actually cost to move money from the app to a traditional bank account?

Understanding the fee structure of Cash App is not merely about knowing a single percentage; it is about mastering your personal finance ecosystem. When you “cash out,” you are essentially navigating the bridge between digital liquidity and traditional banking. This guide explores the intricate details of Cash App’s withdrawal fees, the mechanics of their transfer speeds, and strategic ways to minimize costs while maximizing financial efficiency.

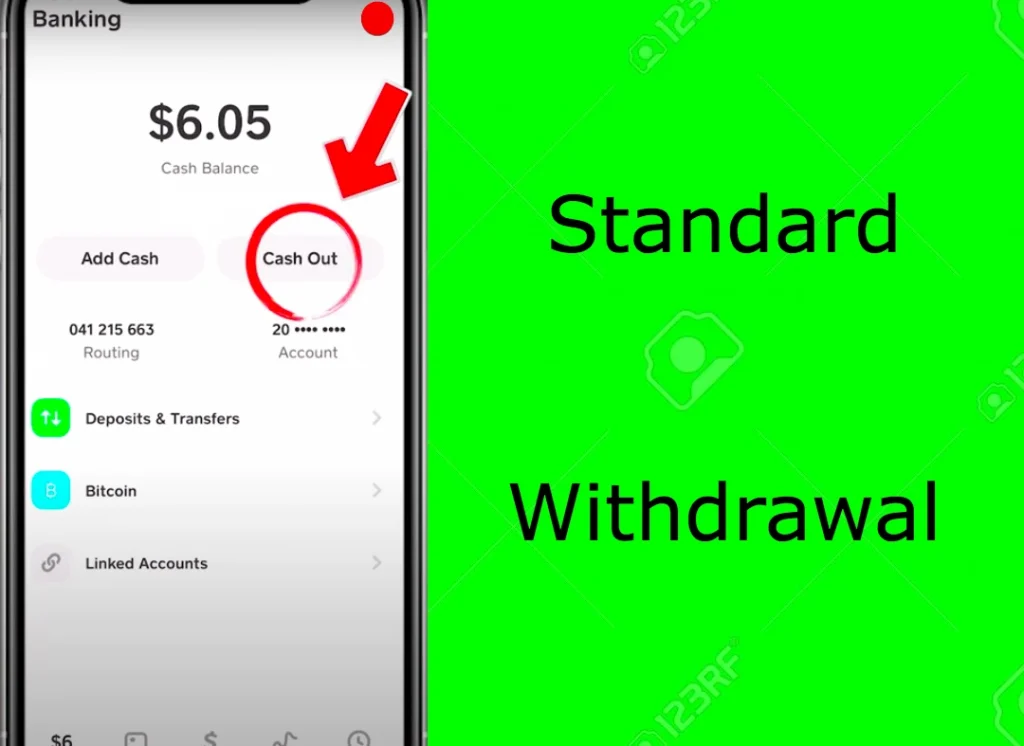

The Mechanics of Cashing Out: Standard vs. Instant Transfers

When you have a balance in your Cash App account, you essentially have two pathways to move those funds into your linked bank account or debit card. These two options—Standard and Instant—represent the classic trade-off in personal finance: time versus money.

Standard Deposits: The Cost-Free Route

For the budget-conscious user, the Standard deposit is the primary tool for maintaining a fee-free experience. When you select a Standard deposit, Cash App processes the transaction through the Automated Clearing House (ACH) network. Because this network operates on a batch-processing system, the funds typically take one to three business days to arrive in your bank account.

The primary advantage here is that Cash App charges $0.00 for this service. From a personal finance perspective, planning your withdrawals 72 hours in advance is one of the simplest ways to avoid eroding your principal balance through micro-fees.

Instant Deposits: Speed for a Fee

There are moments when financial urgency outweighs the desire to avoid fees. Whether it is an impending bill, an emergency expense, or simply the need for immediate liquidity, the Instant Deposit feature allows users to send funds to their linked supported debit card immediately.

Unlike the Standard route, the Instant Deposit relies on different processing rails that facilitate real-time transfers. For this convenience, Cash App charges a fee. It is important to note that these transfers are subject to your bank’s processing times, though they are usually functional within minutes.

Breaking Down the Fee Structure

To manage your money effectively, you must understand the arithmetic behind the “Instant” convenience. Cash App does not use a flat fee for all transactions; instead, it utilizes a percentage-based model that scales with the amount of money you are moving.

How the 0.5% – 1.75% Fee is Calculated

As of the current financial landscape, Cash App typically charges a fee ranging from 0.5% to 1.75% for Instant Deposits. This percentage is applied to the total amount you wish to cash out. For example, if you are cashing out $100 at a 1.75% rate, you will receive $98.25 in your bank account, while $1.75 is retained by the platform as a service fee.

This percentage-based model is common among financial tools, but it requires users to be vigilant. While a 1.75% fee might seem negligible on a $10 transaction ($0.17), it becomes a significant consideration when moving larger sums, such as $1,000, where the fee would be $17.50.

Minimum and Maximum Fee Thresholds

Cash App also implements a “floor” for their fees. Regardless of how small the percentage calculation is, Instant Deposits are generally subject to a minimum fee of $0.25. This means that if you are cashing out a very small amount—say, $5—the 1.75% calculation ($0.08) is ignored in favor of the $0.25 minimum.

From a strategic standpoint, cashing out very small amounts via the “Instant” method is the least efficient way to use the platform, as the $0.25 minimum can represent a disproportionately high percentage of the total transfer.

Maximizing Your Money: Strategies to Avoid Fees

A sophisticated approach to personal finance involves minimizing “leakage”—the small, recurring fees that quietly drain your wealth over time. By understanding the Cash App ecosystem, you can utilize several strategies to keep your money intact.

Utilizing the Cash Card for Direct Spending

One of the most effective ways to “cash out” without actually cashing out is by using the Cash Card. The Cash Card is a free, customizable Visa debit card linked directly to your Cash App balance. Instead of paying a fee to move money to a traditional bank, you can simply spend your balance directly at any retailer that accepts Visa.

Furthermore, the Cash Card offers “Boosts”—instant discounts at specific merchants. By using the card instead of cashing out, you not only avoid the 1.75% fee but can actually save money on your daily purchases, turning a potential expense into a financial gain.

Planning Ahead with Standard Transfers

The “Standard” transfer remains the gold standard for fee avoidance. By treating your Cash App balance like a secondary savings or checking account, you can build a habit of requesting transfers on Tuesdays or Wednesdays. This timing usually ensures that the funds are available by the weekend, preventing the “Friday afternoon panic” that often leads users to pay for an Instant Deposit.

Leveraging Direct Deposit for Free Benefits

Cash App has evolved into a more robust financial tool by offering direct deposit services. Users who choose to have their paychecks deposited directly into Cash App often gain access to additional perks. In some instances, platforms offer “early” access to paychecks or waived fees for certain services (like ATM withdrawals) if a specific amount is direct-deposited monthly. Integrating Cash App more deeply into your financial life can often unlock these “Power User” benefits that mitigate standard costs.

Comparing Cash App to Other Peer-to-Peer (P2P) Financial Tools

In the landscape of personal finance, it is essential to look at the competition to determine if you are getting the best deal. Cash App exists in a crowded market alongside Venmo, PayPal, and Zelle.

Cash App vs. Venmo: Who Wins on Fees?

Venmo and Cash App have remarkably similar fee structures. Both platforms typically offer free standard transfers (1–3 days) and charge a percentage for instant transfers. Currently, Venmo’s instant transfer fee is also around 1.75% with a similar minimum and maximum cap. Choosing between the two often comes down to social preference and which platform your peers use, rather than a significant difference in withdrawal costs.

PayPal and Zelle: Alternative Liquidity Options

PayPal, the parent company of Venmo, also charges a 1.75% fee for instant transfers to bank accounts or debit cards. However, Zelle stands out in the “Money” category as a unique outlier. Because Zelle is integrated directly into the infrastructure of most major banks, it typically offers instant transfers for free.

If your primary goal is moving money between bank accounts without any fees, Zelle is the superior financial tool. However, Zelle lacks the “wallet” features of Cash App, such as the ability to hold a balance, buy Bitcoin, or trade stocks, which makes Cash App a more comprehensive financial ecosystem for many users.

Security and Financial Best Practices

Managing your money on digital platforms requires a focus on security. A “cash out” is only successful if the funds reach the intended destination securely.

Protecting Your Balance from Unauthorized Access

Because Cash App functions much like a bank account, it is a target for phishing and scams. Always ensure that you have “Security Lock” enabled, which requires your passcode or biometric data for every transfer. Additionally, enable notification alerts so you are informed the moment a transaction—especially a cash-out—is initiated.

Understanding Limits and Verification

To move significant amounts of money, you must verify your identity within the app using your full name, date of birth, and the last four digits of your Social Security Number. Unverified accounts have much lower limits on how much they can send or cash out. From a personal finance management perspective, completing the verification process is essential to ensure that your funds aren’t “trapped” in the app during a high-value transaction.

In conclusion, while Cash App’s “Instant” fee of 1.75% is a standard industry practice, it is a cost that can be entirely avoided through strategic planning. By utilizing Standard deposits, the Cash Card, and understanding the timing of the ACH network, you can ensure that your hard-earned money stays exactly where it belongs: in your pocket. As with all financial tools, the key to success lies in understanding the rules of the game and using them to your advantage.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.