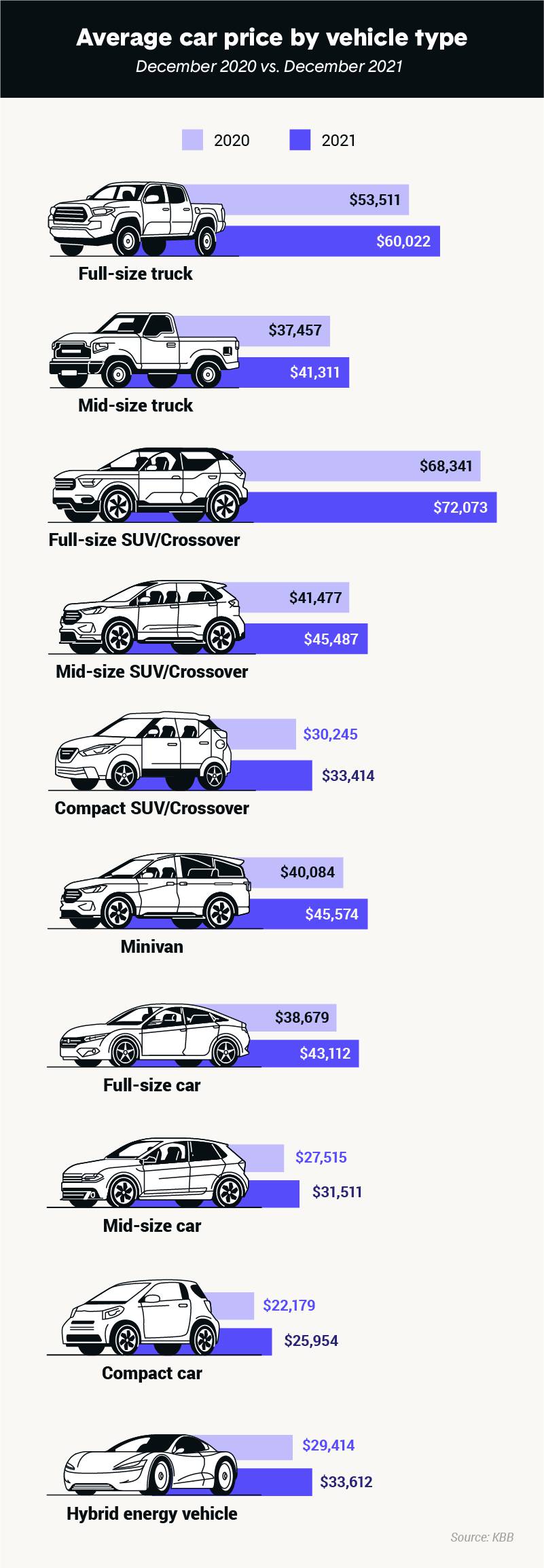

When most consumers ask, “How much does an auto cost?” they are usually referring to the sticker price—the Manufacturer’s Suggested Retail Price (MSRP) displayed prominently on a dealership window. However, from a financial planning perspective, the purchase price is merely the tip of the iceberg. True vehicle ownership involves a complex web of recurring expenses, hidden drains on net worth, and variable operating costs that can significantly impact a household budget.

To truly understand the financial commitment of owning a vehicle, one must look past the initial transaction and analyze the Total Cost of Ownership (TCO). This guide explores the various financial dimensions of vehicle ownership, categorized into purchase mechanics, fixed recurring costs, variable operating expenses, and the often-overlooked impact of depreciation.

1. The Initial Investment: Beyond the Sticker Price

The first step in calculating auto costs is the acquisition phase. While the advertised price sets the baseline, the actual cash outflow or debt obligation is influenced by several financial variables.

New vs. Used: The Financial Trade-off

Choosing between a new and a used vehicle is the most significant decision affecting the initial cost. A new car offers the security of a manufacturer’s warranty and the latest safety features, but it comes with a premium price tag. Conversely, a used vehicle—ideally one that is three to five years old—allows the buyer to avoid the steepest part of the depreciation curve. From a wealth-building perspective, the lower entry price of a used vehicle reduces the amount of capital tied up in a depreciating asset, allowing those funds to be invested elsewhere.

The Hidden Costs of Financing and Interest Rates

Unless you are paying in cash, the cost of the car includes the interest paid over the life of the loan. In an environment of fluctuating interest rates, the Annual Percentage Rate (APR) can add thousands of dollars to the total cost. For example, a $35,000 car financed at 3% over 60 months costs significantly less than the same car financed at 8%. Furthermore, longer loan terms (72 or 84 months) might lower the monthly payment, but they dramatically increase the total interest paid and increase the risk of becoming “underweight” on the loan—where you owe more than the car is worth.

Sales Tax and Dealership Fees

Many buyers forget to budget for the “out-the-door” costs. Sales tax varies by state and municipality but can easily add 5% to 10% to the purchase price. Additionally, documentation fees, title and registration fees, and “dealer preparation” charges can add several hundred, or even thousands, of dollars to the final invoice.

2. Fixed Recurring Expenses: The Cost of Keeping the Car

Fixed costs are the expenses you must pay regardless of whether you drive 10 miles or 10,000 miles in a month. These are the “non-negotiables” of vehicle ownership that must be factored into a monthly financial plan.

Insurance Premiums: Protecting Your Asset

Insurance is often the second largest expense after the loan payment. Premiums are influenced by your credit score, driving record, age, and the type of vehicle. Financing a car usually requires “full coverage,” including collision and comprehensive insurance, which is substantially more expensive than the state-mandated minimum liability coverage. Over time, as the vehicle ages and the loan is paid off, an owner might choose to increase their deductible to lower the premium, but this requires having an emergency fund to cover potential out-of-pocket costs.

Registration and Annual Taxes

Depending on your jurisdiction, you may be required to pay annual registration fees or personal property taxes on your vehicle. Some states calculate these fees based on the vehicle’s weight, while others use its current market value. These are predictable annual expenses, but they can be a significant “lump sum” shock if not accounted for in a monthly savings “sinking fund.”

3. Variable Operating Costs: The Price of Mobility

Variable costs fluctuate based on usage. The more you drive, the higher these costs become. Understanding these variables is essential for accurate monthly budgeting.

Fuel and Energy Consumption

For internal combustion engine (ICE) vehicles, fuel costs are a primary concern, dictated by global oil markets and the vehicle’s fuel efficiency (MPG). For electric vehicles (EVs), the cost shifts to residential electricity rates or public charging fees. While EVs generally offer lower “per mile” energy costs, the initial higher purchase price of the vehicle is the trade-off. A savvy vehicle owner should calculate their expected annual mileage and multiply it by the current energy rates to estimate this monthly outflow.

Maintenance, Repairs, and Wear-and-Tear

No vehicle is maintenance-free. Routine services like oil changes, tire rotations, and brake replacements are the “preventative” costs of ownership. However, as a vehicle exits its warranty period, the risk of “remedial” repairs increases. Financial experts recommend setting aside a specific “auto maintenance” fund—typically $50 to $100 per month—to cover both scheduled maintenance and the inevitable unexpected repair, such as a failed alternator or an AC compressor.

Tires: The Periodic Large Expense

Tires are a unique variable cost because they represent a significant one-time expense every three to five years. Depending on the vehicle type (SUVs and performance cars have more expensive tires), a set of four can cost anywhere from $600 to $1,500. Failing to budget for this can lead to a sudden financial strain or, worse, driving on unsafe tires to avoid the expense.

4. The Invisible Drain: Understanding Depreciation

Depreciation is the most significant “cost” of owning a vehicle, yet it is rarely discussed because it doesn’t result in a monthly bill. It is the difference between what you paid for the car and what you can sell it for later.

Why Your Car is a Depreciating Asset

A vehicle is a tool, not an investment. Most cars lose approximately 15% to 20% of their value in the first year alone. By the five-year mark, many vehicles have lost 60% of their original value. This “phantom cost” represents a massive loss in net worth. If you buy a $40,000 car and sell it five years later for $16,000, that car cost you $24,000 in lost value, or $4,800 per year, before you even factor in gas or insurance.

Strategies to Mitigate Value Loss

While depreciation is inevitable, it can be managed. Purchasing brands known for high resale value (reliability leaders) can slow the drain. Furthermore, keeping a vehicle for a longer duration—ten years instead of five—allows you to “realize” the value of the car over a longer period, reducing the annualized cost of depreciation. The most expensive way to own a car is to trade it in every two to three years, as you are constantly paying for the steepest part of the depreciation curve.

5. Smart Financial Planning for Vehicle Ownership

To ensure that an auto purchase doesn’t derail your long-term financial goals, such as retirement or home ownership, it is vital to apply rigorous budgeting rules.

The 20/4/10 Rule for Car Budgeting

A classic personal finance benchmark for car buying is the 20/4/10 rule:

- 20% Down: Put at least 20% down to avoid being “underwater” on the loan immediately.

- 4-Year Term: Finance the car for no more than four years (48 months) to limit interest and ensure you are paying it off faster than it depreciates.

- 10% of Income: Your total transportation costs (loan, insurance, fuel, maintenance) should not exceed 10% of your gross monthly income.

Following this rule ensures that the “cost of auto” remains a manageable part of your financial life rather than a burden that prevents wealth accumulation.

The Power of the Sinking Fund

The most financially savvy way to handle auto costs is the “sinking fund” method. Instead of being surprised by a $1,000 repair or a $600 insurance renewal, you calculate your total annual expected costs (including a projected replacement for the car itself) and divide by 12. By automating this transfer into a high-yield savings account, you turn “variable” and “unexpected” costs into a steady, predictable monthly line item.

In conclusion, the question “How much does auto cost?” cannot be answered with a single number. It is a dynamic sum of the purchase price, the cost of capital, recurring overhead, and the relentless march of depreciation. By looking at a vehicle as a Total Cost of Ownership proposition rather than a monthly payment, you can make informed decisions that protect your cash flow and your long-term financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.