When potential buyers ask, “How much do Teslas cost?” they are often looking for more than a simple MSRP. In the world of personal finance and strategic investing, the sticker price of a vehicle is merely the entry point into a complex equation of assets, liabilities, and long-term value. Purchasing a Tesla is not just a lifestyle choice; it is a significant financial decision that involves navigating tax incentives, fluctuating energy costs, and unique depreciation curves.

To truly understand the financial commitment of owning a Tesla, one must look past the initial transaction and analyze the Total Cost of Ownership (TCO). This article breaks down the current pricing structures, the impact of government subsidies, and the operational savings that define the Tesla financial experience.

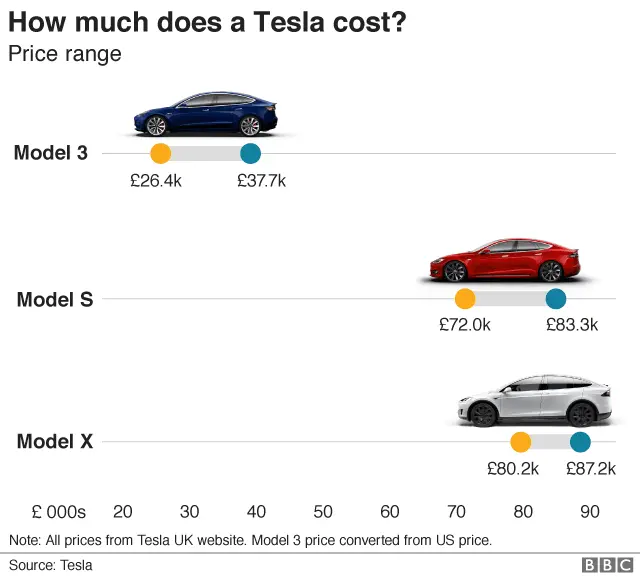

Understanding the Upfront Investment: Tesla’s Current Pricing Tiers

The first step in any financial evaluation is assessing the capital required for the initial purchase. Tesla’s pricing strategy is famously dynamic, often shifting in response to supply chain efficiencies and market demand. Unlike traditional dealerships with opaque “market adjustments,” Tesla utilizes a direct-to-consumer model with transparent, albeit moving, price points.

Entry-Level Accessibility: The Model 3 and Model Y

For the budget-conscious professional or the family looking to optimize their transport expenses, the Model 3 and Model Y represent the primary points of entry. The Model 3, a compact sedan, typically starts in the high $30,000 to mid $40,000 range, depending on the trim (Rear-Wheel Drive vs. Long Range).

The Model Y, currently the world’s best-selling vehicle, commands a slight premium, usually starting in the mid $40,000s. From a financial planning perspective, these models offer the highest utility-to-cost ratio, as they provide access to the Tesla ecosystem and Supercharging network at the lowest possible capital outlay.

Premium Performance and Luxury: The Model S and Model X

Moving up the ladder, the Model S and Model X cater to the high-net-worth individual or the luxury-focused consumer. With prices often starting between $75,000 and $80,000 and scaling well north of $100,000 for “Plaid” performance variants, these vehicles represent a different class of asset.

When evaluating these models, the financial focus shifts from “savings” to “value retention and luxury tax.” While the operational costs remain low, the initial depreciation on an $80,000 luxury EV is significantly higher in absolute terms than on a $38,000 sedan. Investors must weigh the prestige and performance against the opportunity cost of that additional $40,000 in capital.

The Cybertruck and Future Valuation

The introduction of the Cybertruck has added a new layer to Tesla’s financial landscape. With “Foundation Series” pricing reaching into the $100,000+ range, it currently exists as a low-volume, high-margin asset. For business owners, the Cybertruck may offer specific tax advantages, such as Section 179 deductions for heavy vehicles (depending on Gross Vehicle Weight Rating), which can drastically alter the net cost of the vehicle for a profitable enterprise.

Navigating Government Incentives and Tax Credits

In the realm of personal finance, few things are as impactful as a direct reduction in tax liability. The “actual” cost of a Tesla is frequently lower than the MSRP due to aggressive federal and state incentives designed to accelerate EV adoption.

The Federal EV Tax Credit (Section 30D)

The most significant financial lever is the Federal Clean Vehicle Credit. Under the Inflation Reduction Act (IRA), qualifying New Model 3 and Model Y variants may be eligible for a credit of up to $7,500. For the savvy financier, the most critical recent development is the “point-of-sale” credit. As of 2024, buyers can transfer this credit directly to the dealer (Tesla) to reduce the purchase price at the time of sale, rather than waiting to claim it on their annual tax return.

However, this is subject to strict income caps: $300,000 for married couples filing jointly and $150,000 for individuals. Understanding your Modified Adjusted Gross Income (MAGI) is essential to determine if the “cost” of the Tesla is effectively $7,500 lower than the listed price.

State-Level Rebates and Local Incentives

Beyond federal help, states like California, Colorado, and Massachusetts offer additional rebates that can range from $2,000 to $5,000. Some local utility companies also provide incentives for installing home charging stations. When these are stacked, the effective cost of a Model 3 can occasionally drop into the high $20,000s—a price point that competes directly with entry-level internal combustion engine (ICE) vehicles like the Toyota Camry or Honda Accord, but with a much lower operating cost.

Operational Savings vs. Traditional Internal Combustion Engines (ICE)

The “Money” argument for a Tesla is solidified in the operational phase. While the purchase price might be higher than a comparable gas car, the delta is often narrowed or erased over a five-year holding period through reduced energy and maintenance expenditures.

Fuel Cost Analysis: Charging vs. Gasoline

The most immediate impact on a monthly budget is the elimination of gasoline expenses. On average, charging a Tesla at home costs about one-third to one-fourth the price of fueling a 30-MPG gasoline vehicle. For an individual driving 12,000 miles per year, this can translate to annual savings of $1,000 to $2,000 depending on local electricity rates.

From an investment perspective, this is akin to a tax-free dividend. By shifting “fuel” costs to a lower-cost utility, the owner frees up cash flow that can be redirected into other income-producing assets.

Maintenance and Long-Term Reliability

The mechanical simplicity of a Tesla is a significant financial hedge against inflation and rising labor costs. With no oil changes, spark plugs, timing belts, or emissions checks, the routine maintenance schedule is minimal. The most significant recurring costs are tires and cabin air filters.

Furthermore, Tesla’s use of regenerative braking significantly extends the life of brake pads and rotors, often lasting well over 100,000 miles. For a long-term holder, the avoidance of “catastrophic” engine or transmission repairs common in aging ICE vehicles provides a level of financial predictability that is highly valued in personal budgeting.

The Hidden Financial Variables: Insurance, Resale, and Financing

To conclude a professional financial analysis, one must look at the “hidden” costs that can either erode or enhance the value proposition of a Tesla.

Insurance Premiums for High-Tech Vehicles

One area where Tesla owners may see higher costs is insurance. Because Teslas are categorized as high-tech luxury vehicles with specialized repair requirements (aluminum bodies and sensor-heavy components), insurance premiums are often 20% to 30% higher than for a standard sedan.

Strategic buyers should utilize “Tesla Insurance” in states where it is available, as it uses real-time driving behavior to price premiums, potentially offering significant savings for safe drivers. Failing to account for insurance in the TCO can lead to an unpleasant surprise in monthly cash flow.

Depreciation Curves and Resale Value

Depreciation is the largest “silent” expense of any vehicle. Historically, Teslas held their value better than almost any other brand. However, recent price cuts by Tesla to gain market share have led to a more volatile used market.

For the financially astute, this means two things: first, buying a used Tesla can be an incredible “value play” as the initial owner has absorbed the steepest part of the depreciation curve. Second, for new buyers, the holding period matters. The longer you keep the vehicle, the less the annual depreciation impacts your net worth, as the “fuel” and maintenance savings eventually outweigh the loss in resale value.

Interest Rates and Financing Strategies

In a high-interest-rate environment, the method of acquisition is paramount. Financing a $50,000 vehicle at 7% APR adds thousands of dollars to the total cost over the life of the loan. Tesla occasionally offers promotional financing (such as 0.99% or 1.99% APR) on specific models to move inventory.

From a wealth-management standpoint, taking advantage of these low-interest promotional rates allows a buyer to keep their capital deployed in the market (where it might earn 7–10% in an index fund) while paying off the car with “cheap” debt. This arbitrage strategy is a hallmark of sophisticated financial planning when purchasing a high-ticket item like a Tesla.

Conclusion

So, how much does a Tesla cost? The answer is a moving target that depends on your tax bracket, your annual mileage, and your ability to leverage financing. While the initial investment ranges from $38,000 to $100,000+, the effective cost is often much lower once you factor in the $7,500 federal credit, state incentives, and the thousands of dollars saved on fuel and maintenance.

For the disciplined investor, a Tesla is more than a car; it is a tool for optimizing transport expenses and reducing long-term liabilities. By treating the purchase as a data-driven financial decision rather than an emotional one, owners can enjoy the benefits of cutting-edge technology while maintaining a healthy and efficient balance sheet.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.