Navigating the landscape of real estate finance can be both exhilarating and overwhelming. For most aspiring homeowners, the journey begins not with a house hunt, but with a math problem: “How much do I qualify for?” Understanding your mortgage qualification is the cornerstone of a successful property acquisition. It dictates your budget, influences your negotiation power, and ultimately determines the long-term health of your personal finances.

Mortgage qualification is not a singular, static number. It is a dynamic calculation performed by lenders to assess risk. In the eyes of a financial institution, your “qualification” is a measure of their confidence in your ability to repay a substantial debt over fifteen to thirty years. To arrive at this figure, lenders scrutinize several key pillars of your financial life, including your debt-to-income ratio, credit history, capital reserves, and the current economic climate.

The Pillars of Mortgage Qualification: DTI and Credit Health

The first step in determining your loan eligibility involves a deep dive into two critical metrics: your Debt-to-Income (DTI) ratio and your credit score. These numbers serve as the primary indicators of your financial discipline and your capacity to take on more debt.

Understanding the Debt-to-Income (DTI) Ratio

The DTI ratio is perhaps the most significant factor in mortgage underwriting. Lenders use it to measure how much of your monthly gross income is already committed to debt payments. There are two types of DTI ratios that lenders evaluate:

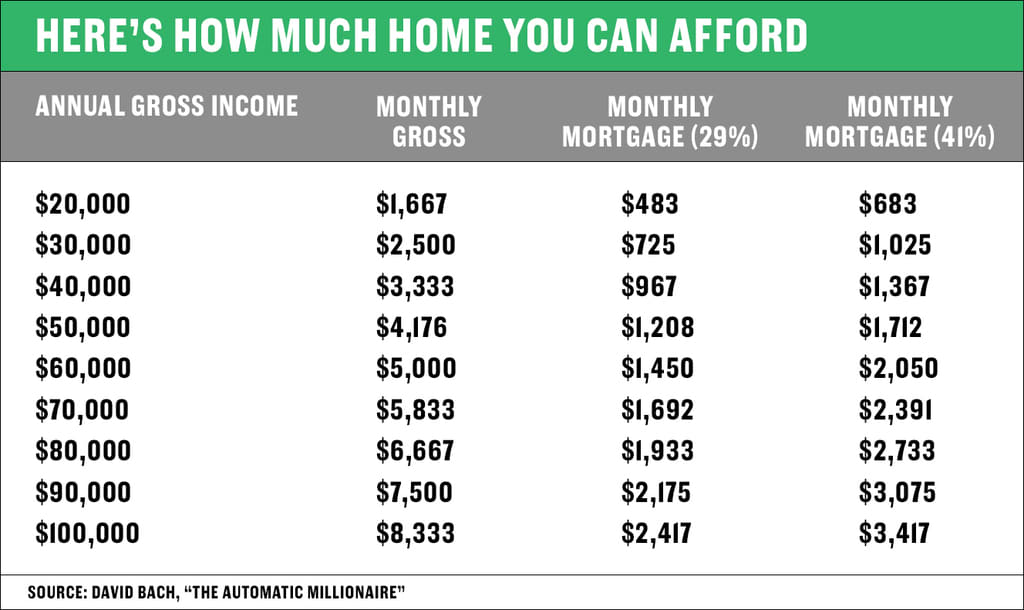

- Front-End Ratio: This represents the percentage of your gross monthly income that would go toward your future housing expenses, including the mortgage principal, interest, taxes, and insurance (PITI). Most lenders prefer this to stay below 28%.

- Back-End Ratio: This is a more comprehensive look at your finances. it includes your projected mortgage payment plus all other recurring monthly debts, such as car loans, student loans, and credit card minimums. Standard guidelines often suggest a back-end ratio of 36% or less, though some government-backed programs allow for ratios as high as 43% or even 50% in specific circumstances.

To calculate your potential loan amount based on DTI, a lender will work backward. If you earn $8,000 a month and the lender allows a 36% back-end ratio, your total monthly debt cannot exceed $2,880. If your current debts (car, student loans) total $800, you have $2,080 left for your mortgage payment.

The Role of Your Credit Score

While DTI determines how much you can borrow, your credit score determines how much it will cost you to borrow. Your credit score is a numerical representation of your creditworthiness based on your history of managing debt.

A higher credit score typically translates to lower interest rates. A difference of even 1% in interest can impact your qualification amount by tens of thousands of dollars. For instance, on a $400,000 loan, a lower interest rate reduces the monthly payment, which in turn improves your DTI ratio and allows you to qualify for a larger purchase price. Lenders generally look for a minimum score of 620 for conventional loans, while FHA loans may accept scores as low as 580 with a slightly higher down payment.

Employment History and Income Stability

Lenders don’t just care about how much you make; they care about how consistently you make it. Standard qualification requires at least two years of steady employment, ideally within the same industry. For salaried W-2 employees, verification is straightforward. However, for those who are self-employed or work in the “gig economy,” qualification requires more documentation, such as two years of comprehensive tax returns. Lenders look for a stable or upward trend in income; significant dips in annual earnings can lead a lender to “average” your income downward, reducing your qualification limit.

Assets, Down Payments, and the Loan-to-Value (LTV) Ratio

The second major component of qualification involves the “skin in the game”—how much cash you are bringing to the table. Your assets influence both the interest rate and the total loan amount you can secure.

The Impact of the Down Payment

The down payment is your initial equity stake in the property. Traditionally, a 20% down payment was the gold standard, as it allows borrowers to avoid Private Mortgage Insurance (PMI) and secures better interest rates. However, modern personal finance offers more flexibility.

- Low Down Payment Programs: Options like FHA loans (3.5% down) or Conventional 97 (3% down) make homeownership accessible.

- VA and USDA Loans: These programs offer 0% down options for eligible veterans or those purchasing in designated rural areas.

It is important to remember that the less you put down, the higher your loan-to-value (LTV) ratio. A high LTV represents a higher risk for the lender, which is why low-down-payment loans often come with stricter DTI requirements or mandatory mortgage insurance premiums that increase your monthly costs.

Closing Costs and Cash Reserves

Qualification also depends on your “liquidity” after the down payment is made. Lenders want to see that you aren’t “house poor” the moment the keys are handed over. Most lenders require “reserves”—liquid assets (savings, stocks, or 401k balances) that can cover several months of mortgage payments in case of an emergency.

Furthermore, you must account for closing costs, which typically range from 2% to 5% of the home’s purchase price. If you have $50,000 saved and plan to use it all for a down payment, you might actually disqualify yourself because you haven’t budgeted for the $10,000 in closing costs. A savvy financial strategy involves balancing the down payment with the need for a safety net.

Private Mortgage Insurance (PMI) and Monthly Costs

If you qualify for a loan with less than 20% down, you must factor in PMI. This is an insurance policy that protects the lender—not you—in case of default. PMI is an added monthly cost that must be included in your DTI calculation. By understanding how PMI affects your monthly payment, you can more accurately estimate the total home price you can afford.

Market Conditions and Loan Product Selection

Your qualification isn’t just about your personal finances; it is also subject to the broader economic environment and the specific financial tools you choose.

The Impact of Prevailing Interest Rates

Interest rates are the “price” of money. When the Federal Reserve adjusts rates, it has a ripple effect on mortgage products. In a high-interest-rate environment, your purchasing power diminishes. For every 1% increase in mortgage rates, your purchasing power typically drops by about 10%.

For example, if you qualify for a $500,000 home at a 4% interest rate, you might only qualify for a $450,000 home at a 5% interest rate, even if your income and debts remain exactly the same. Monitoring market trends is essential for timing your entry into the housing market.

Conventional vs. Government-Backed Loans

The type of loan you choose significantly alters the qualification criteria:

- Conventional Loans: These are not insured by the federal government. They generally require higher credit scores and lower DTI ratios but offer more competitive long-term costs for “strong” borrowers.

- FHA Loans: These are insured by the Federal Housing Administration. They are designed for borrowers with lower credit scores or smaller down payments. Because the government insures these loans, lenders are willing to accept higher risk (higher DTI and lower scores).

- Jumbo Loans: If you are looking at luxury real estate or high-cost areas, you may need a Jumbo loan. These exceed the conforming loan limits set by Fannie Mae and Freddie Mac. Qualification for Jumbo loans is significantly more rigorous, often requiring a 20% down payment, a credit score over 720, and extensive cash reserves.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

A 30-year fixed-rate mortgage is the most common product because of its stability. However, some borrowers look to ARMs to increase their initial qualification amount. ARMs typically offer a lower “teaser” interest rate for the first 5, 7, or 10 years. Because the initial rate is lower, the monthly payment is lower, which can help a borrower qualify for a larger loan today. However, this is a sophisticated financial move that requires a clear exit strategy (selling or refinancing) before the rate resets.

Preparing for the Qualification Process: A Strategic Roadmap

Once you understand the math, the final step is moving from theoretical qualification to a formal commitment from a lender.

Pre-Qualification vs. Pre-Approval

It is vital to distinguish between these two terms.

- Pre-Qualification is a cursory look at your finances. You provide the numbers to a lender, and they give you a ballpark estimate of what you might get. It is not a guarantee and carries little weight in a competitive market.

- Pre-Approval is a rigorous process where the lender verifies your income, runs your credit, and analyzes your tax returns. A pre-approval letter is a powerful financial tool that shows sellers you are a serious and capable buyer.

Documentation Requirements

To finalize your qualification, you will need to organize a “financial passport.” This typically includes:

- The last 30 days of pay stubs.

- W-2 forms from the last two years.

- Federal tax returns (personal and business) for the last two years.

- Bank statements for the last 60 days.

- Documentation for any “gift funds” used for a down payment.

Strategies to Increase Your Loan Amount

If you find that you don’t qualify for the amount you need, there are several financial levers you can pull:

- Reduce Consumer Debt: Paying off a car loan or a credit card can drastically lower your DTI, immediately increasing your mortgage ceiling.

- Increase the Down Payment: Bringing more cash to the closing table reduces the loan amount and the LTV, potentially lowering your interest rate and eliminating PMI.

- Improve Your Credit Score: Sometimes, waiting six months to clean up errors on your credit report or pay down balances can move you into a higher credit tier, saving you hundreds of dollars a month.

- Consider a Co-Borrower: Adding a spouse or a family member with a strong income can increase the total “household” income considered by the lender.

By understanding these mechanics, you transition from a passive participant to an empowered investor. Qualifying for a home loan is not just about finding out what a bank will give you; it is about analyzing your personal financial landscape to ensure that your home remains an asset, rather than a burden, for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.