The question “How much do I owe in federal taxes?” is one of the most common—and often anxiety-inducing—inquiries for individuals across all income levels. It’s a crucial aspect of personal finance that impacts budgeting, savings, and overall financial well-being. Far from being a simple calculation, determining your federal tax liability involves understanding a complex interplay of income sources, deductions, credits, and filing status. This comprehensive guide aims to demystify the process, providing a professional and insightful look into the factors that shape your tax bill and how you can proactively manage your obligations.

Understanding your tax liability is more than just fulfilling a civic duty; it’s about financial empowerment. When you grasp the mechanics of federal taxation, you can make informed decisions throughout the year that optimize your financial position, potentially reducing your tax burden legally and ensuring you’re prepared for tax season. From the moment you earn your first dollar to the complexities of investment income and retirement planning, federal taxes play a significant role. Let’s delve into the core components that dictate what you owe, equipping you with the knowledge to approach tax time with confidence, not consternation.

Understanding Your Federal Tax Obligation

At its core, federal income tax is a levy imposed by the U.S. government on financial income generated by individuals and businesses. For most Americans, this primarily refers to taxes on wages, salaries, and other forms of earnings. However, the exact amount you owe is not just a straightforward percentage of your gross income. The system is designed with various layers and considerations, which, while complex, also offer avenues for strategic financial planning.

The Basics of Taxable Income and the Progressive System

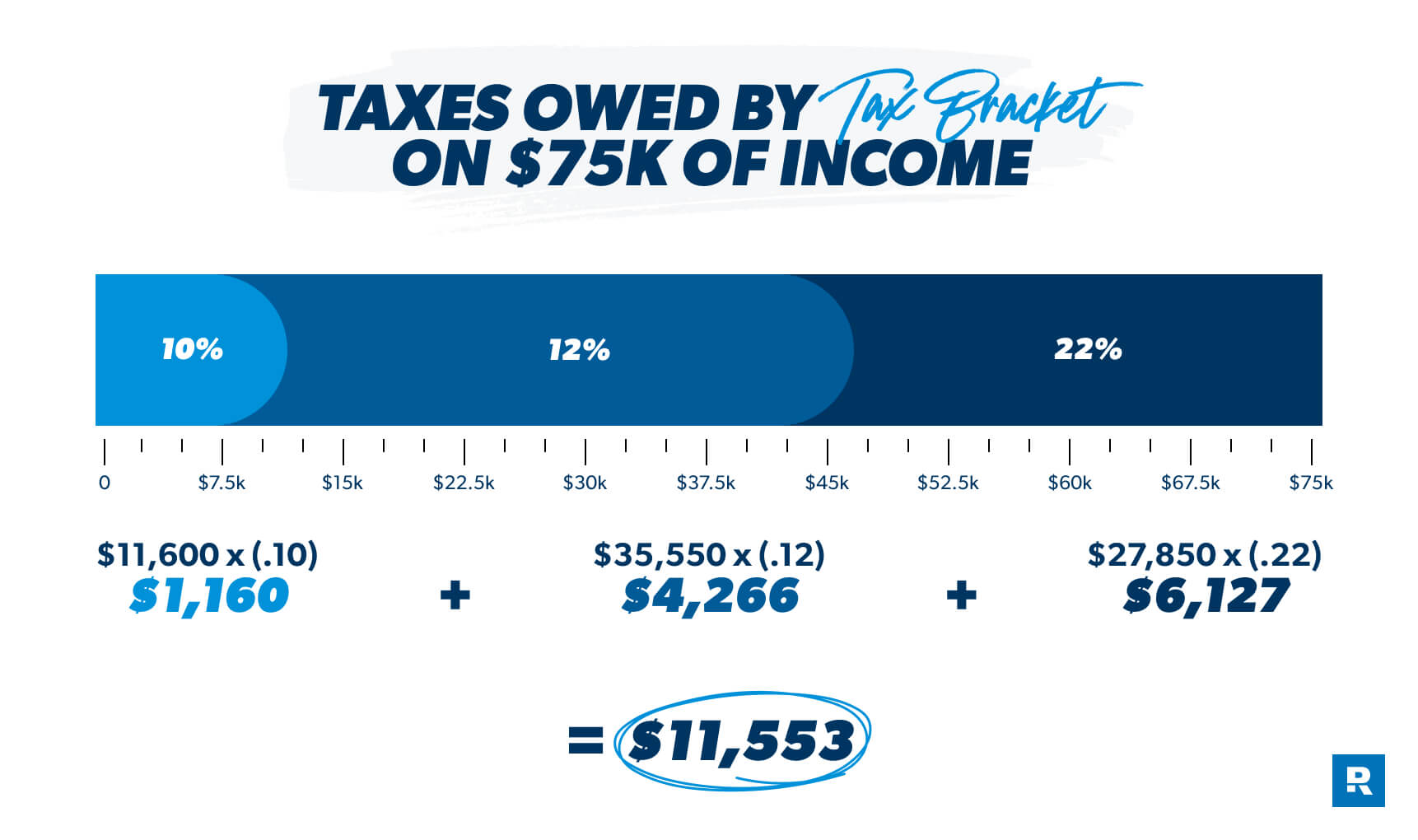

Your journey to calculating federal taxes begins with understanding what constitutes taxable income. This is generally your gross income—all the money you earn from various sources—minus certain allowable deductions. It’s not your entire paycheck, as some contributions (like to a 401(k) or health savings account) might be pre-tax. The U.S. employs a progressive tax system, meaning that as your income increases, you pay a higher percentage of that income in taxes. This is often misunderstood as simply moving into a “higher tax bracket” where all your income is taxed at the higher rate. In reality, different portions of your income are taxed at different marginal rates, only the income falling within a particular bracket is taxed at that bracket’s rate. For example, if you’re in the 22% tax bracket, only the portion of your income that falls into that bracket is taxed at 22%, while the income in lower brackets is taxed at their respective lower rates. This foundational understanding is critical to accurately assessing your tax burden.

Different Types of Federal Taxes

While “federal taxes” often defaults to income tax, it’s essential to recognize other significant components. FICA taxes (Federal Insurance Contributions Act) fund Social Security and Medicare. If you are an employee, your employer typically withholds half of your FICA tax, and you pay the other half through payroll deductions. For the self-employed, however, the burden is greater. Self-Employment Tax encompasses both the employer and employee portions of FICA taxes, amounting to 15.3% on net earnings up to a certain threshold for Social Security, plus 2.9% for Medicare, and an additional Medicare tax for higher earners. Beyond these, you might encounter federal taxes on capital gains from investments, excise taxes on certain goods and services, and estate taxes, though these are less common for the average taxpayer. Recognizing these different streams helps paint a complete picture of your overall federal tax obligation.

Key Factors Influencing Your Tax Liability

Determining your federal tax liability is a highly individualized process, shaped by a multitude of personal and financial circumstances. No two taxpayers will have the exact same tax situation, even with identical incomes, due to the unique interplay of factors like filing status, income sources, and the strategic use of deductions and credits. A deeper dive into these elements reveals how they collectively contribute to your final tax bill.

Your Filing Status and Sources of Income

Your filing status is one of the most fundamental determinants of your tax liability. The IRS recognizes five primary statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Widow(er). Each status comes with its own standard deduction amount, tax bracket thresholds, and eligibility for certain credits, significantly impacting your taxable income and the overall tax rate applied. For instance, a Head of Household typically enjoys a larger standard deduction and more favorable tax brackets than a Single filer. Choosing the correct filing status, especially after life events like marriage, divorce, or having children, is paramount.

Equally critical are your sources of income. While wages and salaries from employment are common, many individuals have diverse income streams that factor into their tax calculations. This can include self-employment income from a side hustle, rental income from properties, interest earned from savings accounts, dividends from stocks, capital gains from selling investments, and even retirement distributions from IRAs or 401(k)s. Each type of income may be treated differently by the tax code, with some subject to specific rules or preferential tax rates, such as qualified dividends or long-term capital gains. A comprehensive accounting of all income sources is the first step towards an accurate tax assessment.

Deductions vs. Credits: Understanding the Difference

Perhaps the most impactful tools for reducing your tax liability are deductions and credits, though they function in fundamentally different ways. Understanding this distinction is crucial for effective tax planning.

Deductions reduce your taxable income. This means they lower the amount of income subject to tax, effectively moving a portion of your income into a lower tax bracket (or out of taxation entirely). For example, if you have a $1,000 deduction and are in the 22% tax bracket, that deduction will save you $220 ($1,000 * 0.22) in taxes. Taxpayers generally choose between taking the standard deduction (a fixed dollar amount based on filing status, adjusted annually for inflation) or itemizing deductions (listing specific eligible expenses, such as mortgage interest, state and local taxes (SALT) up to a limit, and medical expenses exceeding a certain percentage of AGI). Most taxpayers find the standard deduction more beneficial due to its increasing size and simplicity. Additionally, there are “above-the-line” deductions, which reduce your Adjusted Gross Income (AGI) before considering standard or itemized deductions, such as contributions to traditional IRAs, health savings accounts (HSAs), and student loan interest.

Credits, on the other hand, provide a dollar-for-dollar reduction of your actual tax liability. If you have a $1,000 tax credit, it directly reduces the amount of tax you owe by $1,000. This makes credits generally more valuable than deductions. Credits can be non-refundable, meaning they can reduce your tax liability to zero but won’t result in a refund if the credit amount exceeds your tax due. Examples include the Child and Dependent Care Credit or the Credit for Other Dependents. Refundable credits, however, can reduce your tax liability below zero, potentially generating a refund even if you owed no tax. The Earned Income Tax Credit (EITC) and a portion of the Child Tax Credit are prime examples of refundable credits, often providing significant relief to low and moderate-income taxpayers. Strategic utilization of both deductions and credits, based on your eligibility, is key to minimizing your federal tax burden.

Calculating Your Estimated Tax Burden

Calculating your federal tax burden can seem like a daunting task, but by breaking it down into manageable steps, it becomes much clearer. The process essentially follows a logical flow from your total earnings to your final tax liability, with various adjustments along the way. Understanding these steps is fundamental, whether you’re using tax software, working with a professional, or attempting it yourself.

Step-by-Step Calculation Process

The journey to your estimated tax burden typically unfolds as follows:

- Determine Your Gross Income: Begin by tallying all sources of income for the year, including wages, salaries, business profits, rental income, interest, dividends, capital gains, and any other taxable earnings.

- Calculate Your Adjusted Gross Income (AGI): From your gross income, subtract “above-the-line” deductions. These are deductions that reduce your income before your standard or itemized deductions are considered. Common examples include contributions to traditional IRAs, student loan interest payments, HSA contributions, and self-employment tax deductions. Your AGI is a crucial figure, as it determines your eligibility for many tax credits and other deductions.

- Choose Your Deduction Method: Decide whether to take the standard deduction (a fixed amount based on your filing status) or itemize deductions (listing specific expenses like mortgage interest, state and local taxes, and medical expenses). You should choose the method that results in the larger deduction.

- Calculate Your Taxable Income: Subtract your chosen deduction (standard or itemized) from your AGI. This final figure is your taxable income—the amount truly subject to federal income tax.

- Apply Tax Brackets: Using your taxable income and filing status, apply the progressive tax bracket rates to determine your initial tax amount. Remember, only the income within each bracket is taxed at that bracket’s specific marginal rate.

- Subtract Tax Credits: From the initial tax amount calculated in step 5, subtract any eligible tax credits. As discussed earlier, these are dollar-for-dollar reductions of your tax liability and can significantly lower what you owe.

- Add Other Taxes (If Applicable): Finally, add any additional taxes you might owe, such as self-employment tax (if you’re self-employed), Additional Medicare Tax, or the Alternative Minimum Tax (AMT). The AMT is a separate tax system designed to ensure higher-income individuals pay a minimum amount of tax, regardless of deductions and credits.

Utilizing Tax Software and Professionals

While the step-by-step process provides a conceptual framework, executing it accurately can be complex, especially with numerous income sources or deductions. This is where tax software (like TurboTax, H&R Block, or TaxAct) and tax professionals (CPAs or Enrolled Agents) become invaluable. Tax software guides you through the process with user-friendly interfaces, asking questions and automatically performing calculations based on your inputs. They also keep up-to-date with the latest tax laws, minimizing errors.

For more complex situations, such as significant investment activity, business ownership, or major life changes, consulting a tax professional is highly recommended. They can offer personalized advice, identify often-overlooked deductions and credits, and ensure compliance with all applicable tax laws. Their expertise can not only save you money but also provide peace of mind.

Understanding Withholding and Estimated Payments

Calculating your estimated tax burden is only half the battle; the other half is ensuring you’ve paid enough throughout the year to avoid penalties. For most employees, taxes are automatically deducted from each paycheck via withholding. The amount withheld is determined by the W-4 form you complete for your employer. It’s crucial to review and adjust your W-4 annually, especially after significant life events or income changes, to ensure your withholding accurately reflects your current tax situation. Under-withholding can lead to an unexpected tax bill and potential penalties, while over-withholding means you’re giving the government an interest-free loan throughout the year.

For individuals with income not subject to withholding (e.g., self-employment income, rental income, significant investment income), estimated tax payments are required. These are typically paid quarterly using Form 1040-ES to the IRS. The goal is to pay at least 90% of your current year’s tax liability or 100% (110% for higher earners) of your previous year’s tax liability through withholding and estimated payments to avoid underpayment penalties. Accurately estimating these payments requires proactive tax planning throughout the year, ensuring you stay compliant and avoid surprises.

Strategies for Managing and Paying Your Taxes

Effectively managing your federal tax obligations goes beyond simply filing your return by the deadline. It involves a year-round approach to financial planning that can significantly impact your bottom line. Proactive strategies, diligent record-keeping, and an understanding of payment options can transform tax season from a source of stress into a manageable financial task.

Proactive Tax Planning and Record Keeping

The most effective way to manage your tax liability is through proactive tax planning. This means not waiting until January to start thinking about your taxes, but rather integrating tax considerations into your financial decisions throughout the year. For instance, before making a significant investment, understand its tax implications (e.g., capital gains vs. ordinary income). If you anticipate a large bonus, consider adjusting your W-4 or making an estimated payment. Contributing to tax-advantaged accounts like 401(k)s, IRAs, or HSAs not only boosts your savings but also reduces your taxable income. Donating to charity or making large medical expenditures also have tax consequences that can be planned for. Year-end tax moves, such as tax-loss harvesting for investments, can be particularly impactful.

Alongside proactive planning, meticulous record keeping and documentation are indispensable. The IRS requires you to maintain records for a certain period, typically three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. This includes W-2s, 1099s, receipts for deductible expenses, bank and investment statements, and any other documents related to your income or deductions. Organizing these documents digitally or in a physical filing system throughout the year will save you countless hours during tax season, make it easier to substantiate claims if audited, and ensure no valuable deduction or credit is missed.

Payment Options, Deadlines, and Avoiding Penalties

When it comes time to pay your taxes, the IRS offers several convenient payment options. The easiest and often preferred method is through IRS Direct Pay, which allows you to make payments directly from your checking or savings account. Other options include paying by debit card, credit card, electronic federal tax payment system (EFTPS) for businesses, or even check or money order via mail. Understanding these options, and choosing the one that best suits your needs, can streamline the payment process.

Crucially, taxpayers must be aware of key deadlines. The primary deadline for filing federal income tax returns and paying any taxes owed is typically April 15th of each year (or the next business day if April 15th falls on a weekend or holiday). If you need more time to file, you can request an extension, which usually pushes the filing deadline to October 15th. However, an extension to file is not an extension to pay. If you owe taxes, they are still due by the April deadline, and failing to pay by then can incur penalties and interest. Estimated tax payments also have specific quarterly deadlines: April 15, June 15, September 15, and January 15 of the following year.

Avoiding penalties is a significant aspect of tax management. The IRS can impose penalties for underpayment of estimated tax, late filing, and late payment. To avoid the underpayment penalty, ensure that you pay at least 90% of your current year’s tax liability or 100% (or 110% if your AGI was over $150,000 in the prior year) of your previous year’s tax liability through withholding and estimated payments. To avoid late filing penalties, file your return or an extension request by the deadline. To avoid late payment penalties, pay any taxes owed by the April deadline. If you foresee being unable to meet these obligations, it’s vital to communicate with the IRS proactively to explore options like payment plans, which can mitigate or prevent severe penalties.

Navigating Common Tax Scenarios

Life is dynamic, and your tax situation is likely to evolve over time. Major life events and unexpected financial shifts can significantly alter your tax liability. Understanding how these scenarios impact what you owe can help you adapt your tax strategy accordingly and avoid surprises.

Changes in Life Circumstances

Life events often come with significant tax implications that require immediate attention. Marriage typically changes your filing status to Married Filing Jointly or Married Filing Separately, impacting your standard deduction and tax brackets. It’s often beneficial to run a “tax projection” to see which filing status provides the most advantage. Divorce also shifts filing status, potentially to Single or Head of Household, and can affect deductions for alimony (for agreements prior to 2019) or child-related tax benefits. The birth or adoption of a child can introduce valuable credits like the Child Tax Credit and potentially change your filing status to Head of Household, offering substantial tax relief.

A new job or a significant raise will alter your income and likely push you into a higher marginal tax bracket, necessitating an adjustment to your W-4 to ensure adequate withholding. Conversely, job loss can mean fewer earnings, but also potential eligibility for unemployment benefits (which are taxable) and specific deductions related to job searching. Retirement brings a new landscape of income, primarily from pensions, 401(k)s, IRAs, and Social Security, each with different tax treatments. Planning withdrawals strategically is key to minimizing taxes in retirement. Even seemingly minor changes, like moving to a new state, can have federal tax implications if it affects your state tax deductions. Proactively reviewing your tax situation after any major life change is a crucial step in managing your federal tax obligation.

Dealing with Unexpected Income or Expenses and What to Do If You Can’t Pay

Sometimes, financial circumstances arise that are less predictable than life events. Receiving a windfall, such as lottery winnings, a large inheritance, or a significant bonus, will increase your taxable income. For large sums, especially those not subject to withholding, it may be necessary to make estimated tax payments to avoid underpayment penalties. Similarly, selling a major asset like real estate or a business can trigger substantial capital gains taxes, requiring careful planning to manage the tax impact. On the other hand, unexpected large expenses, such as significant unreimbursed medical bills or property damage from a natural disaster, might create new deduction opportunities, though these are subject to specific thresholds and rules. Keeping meticulous records of these financial shocks is essential for accurate tax reporting.

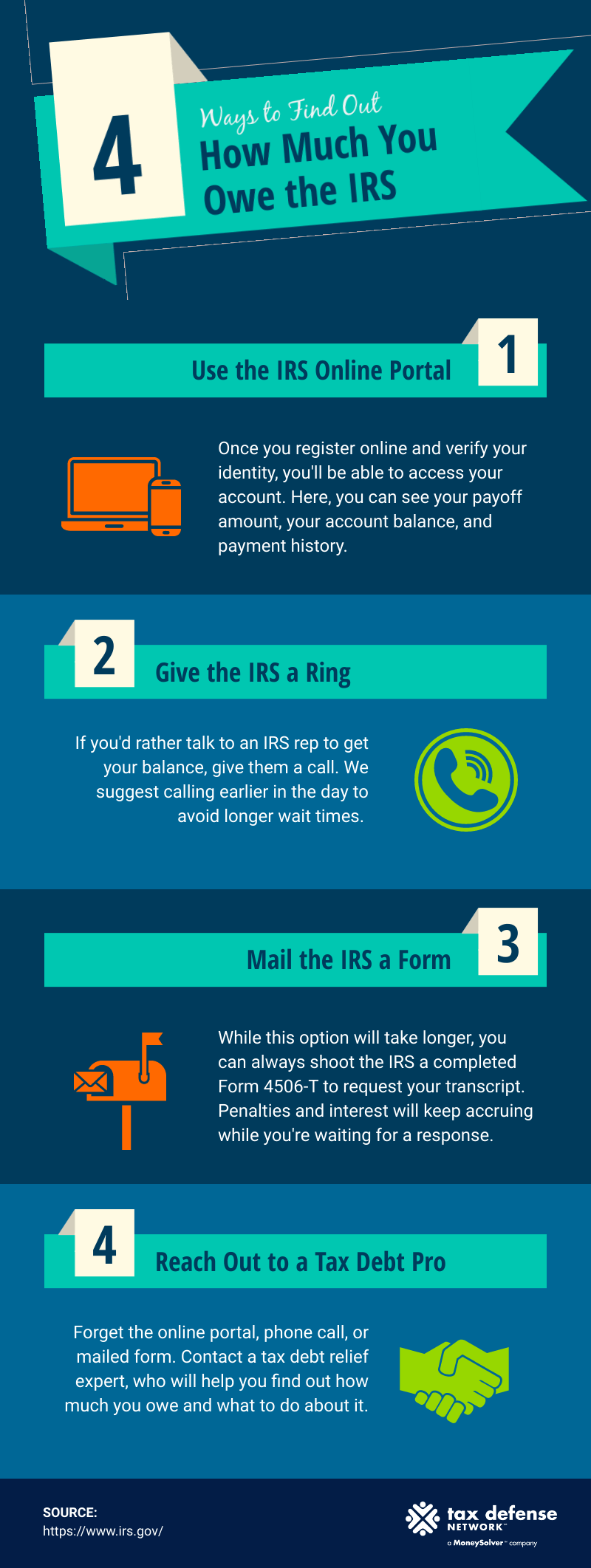

Finally, one of the most stressful scenarios is realizing you cannot pay your federal taxes by the deadline. It is absolutely critical not to ignore this. The worst thing you can do is avoid filing or communicating with the IRS. If you can’t pay, file your tax return on time anyway. This avoids the late filing penalty, which is often much higher than the late payment penalty. Then, contact the IRS to explore your options. They offer several programs designed to help taxpayers facing financial hardship. An installment agreement allows you to make monthly payments for up to 72 months. An Offer in Compromise (OIC) allows certain taxpayers to settle their tax debt for a lower amount than they originally owed, typically when they are in severe financial distress and unable to pay the full amount. In some cases, a temporary delay in collection may be granted if payment would cause significant hardship. Proactive communication and exploring these options can prevent escalating penalties and interest, providing a pathway to resolving your tax debt responsibly.

Conclusion

Understanding “how much do I owe in federal taxes” is a fundamental component of sound personal finance. It requires a comprehensive grasp of income sources, filing status, the power of deductions and credits, and the intricacies of the progressive tax system. While the process can seem daunting, breaking it down into manageable steps, utilizing available resources like tax software or professional advice, and engaging in proactive tax planning throughout the year can transform uncertainty into clarity.

Your federal tax obligation is not a static figure; it’s a dynamic calculation influenced by every financial decision you make and every life event you experience. By staying informed, meticulously organizing your records, and adapting your strategies to changing circumstances, you can effectively manage your tax burden. Remember, the goal isn’t just to pay your taxes, but to pay the right amount, ensuring compliance while optimizing your financial position. Armed with this knowledge, you are better equipped to navigate the complexities of federal taxation with confidence, contributing responsibly to the nation’s fiscal health while safeguarding your own.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.