For many Americans, Social Security represents the foundation of a stable retirement. Yet, despite its importance, the system is often shrouded in complexity. When people ask, “How much can you make on Social Security?” the answer is rarely a single number. It is a calculation derived from decades of work history, the timing of your application, and your marital status. Understanding these variables is not just an academic exercise; it is a critical component of personal finance that can result in a difference of hundreds of thousands of dollars over the course of a retirement.

This guide explores the mechanics of Social Security, the strategic implications of timing, and how to integrate these benefits into a holistic financial plan.

Understanding the Mechanics of Social Security Benefits

The Social Security Administration (SSA) uses a specific formula to determine your monthly benefit, known as the Primary Insurance Amount (PIA). To understand how much you can make, you must first understand how the government evaluates your career.

The Role of the Primary Insurance Amount (PIA)

Your PIA is the base amount you are entitled to receive if you claim benefits at your Full Retirement Age (FRA). To calculate this, the SSA looks at your Average Indexed Monthly Earnings (AIME). This isn’t a simple average of your lifetime earnings; rather, the SSA “indexes” your past earnings to account for changes in average wages over time. This ensures that the $20,000 you earned in 1985 is weighted fairly against the $80,000 you earn today.

How Your 35 Highest-Earning Years Impact Your Check

The AIME is calculated based on your 35 highest-earning years. If you worked for 40 years, the lowest five years are dropped. However, if you worked for only 30 years, the SSA will factor in five years of “zero” earnings. This significantly lowers your average and, consequently, your monthly check. For those looking to maximize their income, working long enough to replace low-earning years from early in their career with higher-earning years later in life is one of the most effective strategies available.

The Timing Strategy: When to Claim for Maximum Payouts

One of the most significant decisions a retiree will make is choosing the age at which to begin receiving benefits. While you can claim as early as age 62, the financial implications of doing so are permanent.

Early Filing at Age 62: The Cost of Convenience

Filing at 62 is tempting for those who wish to retire early or need the cash flow. However, doing so results in a permanent reduction in benefits. If your Full Retirement Age is 67, claiming at 62 means your monthly check will be reduced by roughly 30%. While you receive checks for five additional years, the cumulative “break-even” point usually occurs in your late 70s. If you expect to live a long life, filing early is often a losing financial proposition.

Full Retirement Age (FRA): The Baseline Standard

Your FRA is the age at which you receive 100% of your earned benefit. For anyone born in 1960 or later, the FRA is 67. At this age, you can also work and earn an unlimited amount of income without having your Social Security benefits temporarily withheld. For many, the FRA represents the “sweet spot” of balancing immediate income with a respectable monthly amount.

Delayed Retirement Credits: The Power of Waiting Until Age 70

For every year you delay claiming benefits beyond your FRA up until age 70, your benefit increases by 8% annually. This is a guaranteed, inflation-adjusted return that is virtually impossible to match in the private market. By waiting until age 70, a person with an FRA of 67 would receive 124% of their PIA. For a high earner, this could mean the difference between a $3,000 monthly check and a $3,720 monthly check, significantly increasing the “maximum” one can make.

Exploring Additional Benefit Streams

Social Security is not limited to your own work record. The system is designed with “social insurance” features that provide benefits to family members, which can significantly increase a household’s total income.

Spousal and Survivor Benefits

If you are married, you may be eligible for a spousal benefit. This allows a lower-earning spouse to receive up to 50% of the higher-earning spouse’s PIA. This does not reduce the higher earner’s benefit. Furthermore, survivor benefits are a critical component of estate planning. When one spouse passes away, the survivor has the option to switch to the deceased spouse’s higher benefit amount, provided they have reached the required age.

Benefits for Divorced Spouses

Many individuals are unaware that they can claim benefits based on an ex-spouse’s work record. If the marriage lasted at least 10 years, the claimant is at least 62, and they are currently unmarried, they may be entitled to a benefit equal to 50% of their ex-spouse’s benefit. This provides a vital financial safety net and does not impact the ex-spouse’s own benefit or the benefits of their current spouse.

Disability and Child Benefits

Social Security also provides for Social Security Disability Insurance (SSDI). If a worker becomes disabled before retirement age, they may receive their full PIA immediately. Additionally, if a parent receives retirement or disability benefits, their minor children (or adult children disabled before age 22) may also be eligible for auxiliary benefits, further increasing the total family take-home.

Navigating Taxes and Earnings Limits

“How much you make” isn’t just about the gross number on the check; it’s about how much you keep after taxes and adjustments.

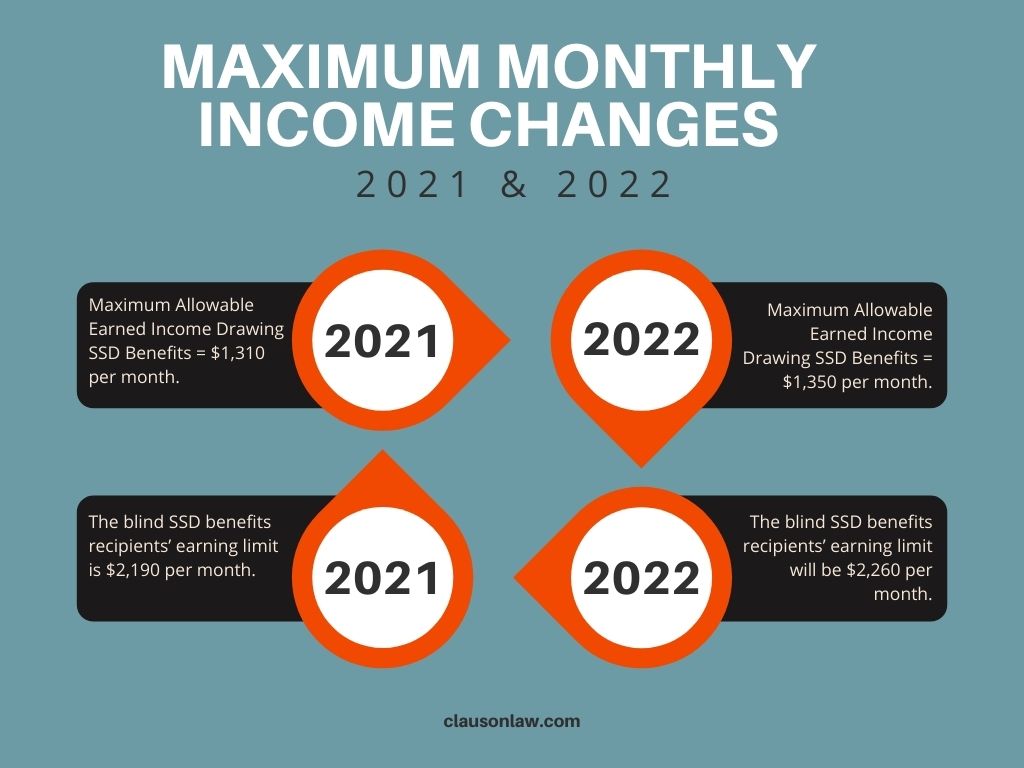

The Social Security Earnings Test

If you claim benefits before your FRA and continue to work, you are subject to the Social Security Earnings Test. For 2024, if you earn over $22,320, the SSA will withhold $1 in benefits for every $2 you earn above that limit. While these withheld benefits are eventually added back to your check once you reach FRA, the immediate reduction in cash flow can be a shock to those who haven’t planned for it.

Taxation of Benefits: The Combined Income Threshold

Depending on your total income, up to 85% of your Social Security benefits may be subject to federal income tax. This is determined by your “combined income,” which is the sum of your adjusted gross income, non-taxable interest, and half of your Social Security benefits. If this total exceeds $34,000 for individuals or $44,000 for couples filing jointly, the 85% tax bracket applies. Understanding this “tax torpedo” is essential for high-net-worth individuals who are balancing withdrawals from 401(k)s and IRAs alongside Social Security.

Long-Term Financial Planning and Sustainability

To truly maximize what you make on Social Security, you must view it as one piece of a larger financial puzzle. It is an inflation-protected annuity that serves as a hedge against market volatility.

Cost-of-Living Adjustments (COLA) and Inflation Protection

One of the most valuable features of Social Security is the annual COLA. Unlike most private pensions or fixed-income investments, Social Security benefits are adjusted annually based on the Consumer Price Index. In years of high inflation, these adjustments can be substantial, ensuring that your purchasing power remains relatively stable even as the cost of goods and services rises.

Integrating Social Security into Your Total Portfolio

In professional wealth management, Social Security is often treated as a “bond-like” asset. Because it provides a guaranteed income stream, it may allow retirees to take slightly more risk in their personal investment portfolios (equities) to combat long-term inflation. Furthermore, by strategically choosing when to claim, retirees can manage their tax brackets more effectively—perhaps drawing down taxable accounts while delaying Social Security to 70 to maximize the tax-deferred growth of the benefit itself.

Ultimately, the answer to “how much can you make on Social Security” depends on your patience and your planning. By maximizing your 35 highest-earning years, understanding the impact of filing ages, and leveraging spousal or survivor benefits, you can turn a standard government benefit into a robust engine for financial independence. While the maximum possible check for a high earner at age 70 in 2024 is approximately $4,873 per month, the real “win” is found in the strategy that ensures your benefits last as long as you do.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.