For many, buying a home is the quintessential American dream, representing stability, a significant investment, and a place to create lasting memories. However, before the exciting journey of house hunting can begin, a crucial question looms large: “How much can I get for a home loan?” Understanding your borrowing capacity is not just about crunching numbers; it’s about setting realistic expectations, empowering your search, and ultimately, securing a home that aligns with your financial well-being.

The answer isn’t a simple figure that applies to everyone. Lenders assess a multitude of factors to determine how much they are willing to lend you. This article will demystify the home loan qualification process, delving into the core determinants, various loan programs, the lender’s perspective, and practical steps you can take to maximize your eligibility, all while maintaining a clear focus on what you can genuinely afford.

The Core Determinants of Your Loan Amount

When you apply for a home loan, lenders meticulously evaluate your financial profile to gauge your ability to repay the debt. This assessment boils down to several key factors, each playing a critical role in shaping the final loan amount.

Income Stability and Employment History

Your income is arguably the most significant factor lenders consider. They want to see a consistent, reliable income stream that demonstrates your capacity to make monthly mortgage payments. This typically involves reviewing your last two years of employment history, looking for stability and growth. Lenders consider various types of income, including salaries, wages, bonuses, commissions, self-employment income, and even certain types of benefits (like Social Security or disability). However, self-employment income often requires more extensive documentation and a longer track record to prove consistency. The overall stability of your employment—how long you’ve been at your current job and in your industry—also plays a crucial role in reassuring lenders about your future earning potential.

Credit Score and History

Your credit score is a three-digit summary of your financial trustworthiness. It reflects your past behavior in managing debt, including how consistently you’ve paid bills, the types of credit you’ve used, the length of your credit history, and your credit utilization. A higher credit score (generally above 740) signals a lower risk to lenders, often translating into better interest rates and more favorable loan terms, which can indirectly allow you to qualify for a larger loan amount or reduce your monthly payments for the same loan size. Conversely, a lower score might lead to higher interest rates, stricter requirements, or even loan denial. Lenders will pull a comprehensive credit report that details your payment history, outstanding debts, and any bankruptcies, foreclosures, or collections.

Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio is a critical metric that lenders use to assess your ability to manage monthly payments and repay debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. There are two types:

- Front-end DTI: This ratio considers only your proposed housing expenses (mortgage principal and interest, property taxes, homeowner’s insurance, and HOA fees, if applicable) relative to your gross monthly income.

- Back-end DTI: This more comprehensive ratio includes all your monthly debt obligations—credit card payments, car loans, student loans, personal loans—in addition to your proposed housing expenses, relative to your gross monthly income.

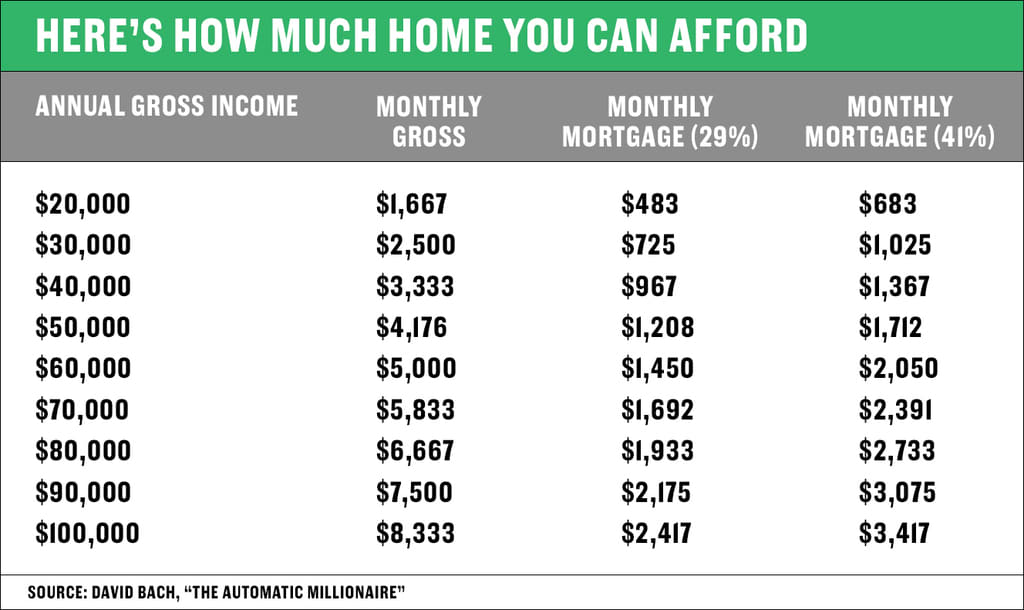

Lenders typically prefer a back-end DTI ratio of 36% or lower for conventional loans, though some programs may allow up to 43-50% in certain circumstances. A lower DTI indicates you have more disposable income to cover your mortgage, making you a less risky borrower.

Down Payment and Assets

The size of your down payment directly impacts the loan amount you need and can significantly influence the terms you receive. A larger down payment reduces the amount you need to borrow, lowers your monthly payments, and can help you avoid Private Mortgage Insurance (PMI) if you put down 20% or more on a conventional loan. Beyond the down payment, lenders also look at your available assets or reserves. These are funds you have in savings, checking, or investment accounts after your down payment and closing costs are paid. Reserves demonstrate that you have a financial cushion to fall back on in case of unexpected expenses or income disruptions, further reducing the lender’s risk. Gift funds from family members are often permissible, but typically require specific documentation.

Understanding Loan Programs and Their Impact

The type of home loan you choose can significantly influence how much you can borrow and the qualifying criteria you’ll need to meet. It’s not a one-size-fits-all world; different loan programs cater to different financial situations and borrower profiles.

Conventional Loans

Conventional loans are not insured or guaranteed by the government. They are the most common type of mortgage and are offered by private lenders. Qualifying for a conventional loan typically requires a good to excellent credit score (generally 620+), a stable income, and a DTI ratio that falls within specific limits (often 36-43%). While 20% down is ideal to avoid PMI, conventional loans can be secured with as little as 3-5% down, though PMI will be required. These loans offer flexibility in terms and conditions but generally have stricter credit and income requirements compared to government-backed options.

Government-Backed Loans (FHA, VA, USDA)

These loans are designed to make homeownership more accessible, especially for individuals who might not qualify for conventional loans.

- FHA Loans: Insured by the Federal Housing Administration, FHA loans are popular among first-time homebuyers and those with less-than-perfect credit. They allow for down payments as low as 3.5% and have more lenient credit score requirements (often as low as 580). However, they require borrowers to pay upfront and annual mortgage insurance premiums, regardless of the down payment size.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, VA loans are an incredible benefit for eligible service members, veterans, and surviving spouses. They offer 100% financing (no down payment required), competitive interest rates, and no private mortgage insurance. While they have a funding fee, this can sometimes be waived for those with service-connected disabilities.

- USDA Loans: Backed by the U.S. Department of Agriculture, USDA loans are designed for low-to-moderate-income individuals purchasing homes in designated rural areas. They also offer 100% financing and generally have lower interest rates and mortgage insurance compared to FHA loans. Income and property eligibility requirements are specific to these programs.

Jumbo Loans

When the amount you need to borrow exceeds the conventional loan limits set by the Federal Housing Finance Agency (FHFA), you’re looking at a jumbo loan. These loans are used for high-value properties and often come with more stringent qualification requirements. Lenders typically demand higher credit scores (often 700+), larger down payments (10-20% or more), lower DTI ratios, and greater cash reserves compared to conventional loans, due to the increased risk associated with the larger loan amount.

First-Time Homebuyer Programs

Many states, counties, and cities offer specific programs designed to assist first-time homebuyers. These can include down payment assistance grants, forgivable loans, reduced interest rates, or tax credits. Eligibility often depends on income limits, property location, and completion of homebuyer education courses. These programs can significantly boost your buying power by reducing your upfront costs or lowering your monthly payments, effectively allowing you to “get more” for a home loan within your budget.

The Lender’s Perspective: What Underwriters Look For

While the factors above outline your financial profile, it’s crucial to understand how lenders, particularly their underwriters, synthesize this information to make a final decision. They are performing a comprehensive risk assessment.

The “Four Cs” of Credit

Lenders often evaluate loan applicants based on the “Four Cs” of Credit, a traditional framework for assessing creditworthiness:

- Capacity: Your ability to repay the loan, primarily judged by your income stability, employment history, and DTI ratio.

- Capital: Your financial reserves and down payment, demonstrating your financial stake in the property and ability to weather financial setbacks.

- Collateral: The property itself. Lenders want to ensure the home’s value is sufficient to secure the loan.

- Character: Your willingness to repay, primarily reflected by your credit history and score. This tells lenders how reliably you’ve managed past debts.

Property Valuation and Appraisal

Even if you’re a stellar applicant, the property you intend to purchase must also meet the lender’s standards. Before approving a loan, lenders require an independent appraisal of the property. This ensures that the home’s market value supports the loan amount. If the appraisal comes in lower than the agreed-upon purchase price, it can impact the loan amount, potentially requiring you to bring more cash to the closing table or renegotiate with the seller. Lenders won’t lend more than the appraised value, regardless of your personal financial strength.

Risk Assessment and Mitigating Factors

Underwriters look for red flags and mitigating factors. A recent job change might be a flag, but if it comes with a significant promotion and salary increase in the same industry, it could be a mitigating factor. Gaps in employment, high credit card balances, or a history of late payments will increase perceived risk. Conversely, a large down payment, substantial reserves, or a long history of paying debts on time will mitigate risk, making you a more attractive borrower and potentially qualifying you for a larger loan or better terms. The underwriter’s job is to weigh all these elements to determine if the loan fits within the lender’s risk appetite.

Practical Steps to Maximize Your Loan Eligibility

Understanding the factors is the first step; taking proactive measures to improve your financial standing is the next. By strategically preparing, you can enhance your chances of securing the maximum possible home loan with favorable terms.

Improve Your Credit Score

Start by obtaining your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) and dispute any errors. Pay all bills on time, every time, as payment history is the most significant factor in your score. Reduce your credit utilization by paying down credit card balances, aiming to keep them below 30% of your available credit. Avoid opening new credit accounts or closing old ones before applying for a mortgage, as both can negatively impact your score.

Reduce Your Debt

Lowering your overall debt burden is crucial for improving your DTI ratio. Focus on paying down high-interest debts like credit cards and personal loans. Consider creating a debt repayment plan, such as the snowball or avalanche method, to systematically tackle your obligations. Even small reductions in monthly debt payments can significantly improve your DTI, allowing you to qualify for a larger mortgage or simply making your financial picture more appealing to lenders.

Increase Your Down Payment

Saving a larger down payment is one of the most impactful ways to increase your loan eligibility and reduce your monthly costs. A larger down payment reduces the principal amount you need to borrow, potentially opening doors to more favorable interest rates and helping you avoid PMI. Explore strategies like automating savings, cutting discretionary expenses, or even considering gift funds from family members (ensuring proper documentation is provided). The more you put down, the less risky you appear to lenders.

Get Pre-Approved

Before you start seriously looking at homes, get pre-approved for a mortgage. Pre-approval is a formal process where a lender reviews your financial information (income, credit, assets) and gives you a conditional commitment for a specific loan amount. This step provides a clear understanding of how much you can borrow, what your interest rate might be, and what your monthly payments will look like. It also makes you a more attractive buyer to sellers, as it demonstrates your financial readiness and seriousness. A pre-approval letter strengthens your offer in a competitive market.

Beyond the Loan Amount: What You Can Truly Afford

While a lender might pre-approve you for a substantial loan, it’s vital to distinguish between what you can get and what you can comfortably afford. Overextending yourself financially can lead to stress and compromise your long-term financial goals.

The Difference Between Pre-Approval and Affordability

A pre-approval tells you the maximum loan amount a lender is willing to offer based on their risk assessment. Your personal affordability goes a step further, factoring in your lifestyle, financial goals, and comfort level. Just because a lender approves you for a $400,000 loan doesn’t mean a $400,000 home fits your budget after considering all other expenses. It’s about finding a balance where your housing costs don’t consume too large a portion of your income, leaving room for savings, emergencies, and discretionary spending.

Hidden Costs of Homeownership

The mortgage principal and interest are just two components of your monthly housing expense. Homeownership comes with several other significant costs that must be factored into your budget:

- Property Taxes: These are typically assessed by local governments and can vary widely.

- Homeowner’s Insurance: Required by lenders, this protects your home against damage and liability.

- Private Mortgage Insurance (PMI): If your down payment is less than 20% on a conventional loan.

- Homeowners Association (HOA) Fees: If you live in a community with shared amenities.

- Utilities: Often higher than apartment living due to larger space.

- Maintenance and Repairs: A crucial, often underestimated cost. Experts recommend budgeting 1-3% of your home’s value annually for maintenance.

Personal Budgeting and Financial Comfort

Create a detailed budget that includes all your income and expenses. After factoring in your estimated mortgage payment (including taxes, insurance, and HOA), utilities, and a realistic maintenance fund, ensure you still have enough left for food, transportation, savings, entertainment, and other personal needs. Many financial advisors suggest keeping total housing costs (PITI + HOA + insurance + maintenance) below 28-30% of your gross monthly income. This allows for flexibility and reduces the risk of being “house poor.” Your comfort level with your monthly payments is paramount to a sustainable and enjoyable homeownership experience.

Conclusion

Understanding “how much can I get for a home loan” is a complex yet crucial step on the path to homeownership. It requires a thorough understanding of your financial health, the various loan programs available, and the intricate evaluation process lenders undertake. By focusing on your income stability, credit score, DTI ratio, and down payment, you can significantly influence your borrowing capacity.

However, true financial wisdom lies not just in securing the maximum loan, but in thoughtfully determining what you can genuinely afford without sacrificing your overall financial comfort and future goals. Take the time to prepare, research, and seek advice from financial professionals and mortgage lenders. With a clear understanding of your options and a disciplined approach to your finances, you can confidently navigate the home loan process and step into a home that truly enhances your life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.