Social Security stands as a cornerstone of retirement planning for millions of Americans, providing a crucial safety net against the financial uncertainties of old age, disability, and even death. For many, understanding how their benefits are calculated is paramount to effective financial planning. One of the most common questions, and perhaps one of the most fundamental, is “how many years is Social Security based on?” The answer isn’t a simple single number, but rather a sophisticated formula designed to reflect a lifetime of work, aiming to provide a fair and progressive benefit.

At its heart, the Social Security Administration (SSA) primarily uses a worker’s 35 highest-earning years to calculate their retirement benefits. This “best 35 years” rule is a critical component of the benefit formula, impacting everything from your average monthly earnings to your ultimate monthly payout. However, the calculation involves more than just selecting 35 years; it incorporates concepts like indexing, bend points, and various claiming age factors that profoundly influence the final amount. Navigating these intricacies is essential for anyone looking to optimize their retirement strategy and ensure they receive the maximum benefits they are entitled to. This article will delve deep into the mechanics of how Social Security benefits are determined, shedding light on the “years” question and its broader implications for your financial future.

Decoding the Core: The “Best 35 Years” Rule

The foundation of your Social Security retirement benefit lies in your earnings record, specifically how your wages from decades of work are compiled and averaged. The “best 35 years” rule is the bedrock of this calculation, designed to reflect your most productive working years while accommodating various career paths and life events.

The Foundation of Your Future Benefit

When you work and pay Social Security taxes, the SSA keeps a detailed record of your earnings. This record is crucial because it forms the basis of your future benefits. The SSA doesn’t simply average all your working years; instead, it specifically looks for the 35 years in which you had the highest taxable earnings. This approach is beneficial for individuals who might have had periods of unemployment, lower earnings early in their careers, or taken time off for caregiving or further education. By focusing on the peak earning years, the system attempts to provide a more accurate reflection of your lifetime earning potential and a more generous benefit than if all years, including those with zero or low earnings, were included in a straight average.

Understanding Covered Earnings and Indexing

“Covered earnings” refer to the income you’ve earned up to the Social Security taxable maximum for any given year, on which you paid Social Security taxes. It’s important to note that earnings above this annual maximum are not subject to Social Security taxes and, therefore, do not count towards your benefit calculation.

A critical step in determining your average earnings is “indexing.” Because a dollar earned in 1980 had significantly more purchasing power than a dollar earned in 2023, the SSA adjusts your historical earnings to reflect changes in the national average wage level over time. This process ensures that your past earnings are expressed in terms of current dollar values, providing a fair comparison across decades. For example, an income of $20,000 in 1985 would be “indexed” upward to a much higher amount in today’s dollars, reflecting inflation and general wage growth. This indexing typically applies up to age 60; earnings from age 60 onward are usually counted at their nominal value. This mechanism is vital for accurately calculating the average that will determine your benefits, as it prevents your benefit from being unduly diminished by historical low-dollar earnings.

What Happens with Fewer Than 35 Years?

While the “best 35 years” rule is standard, not everyone works for 35 years. Some individuals might have shorter careers, take extended breaks, or enter the workforce later in life. If you have fewer than 35 years of covered earnings, the SSA will still use a 35-year period for the calculation. However, for any years in which you had no earnings, those years will be entered into the calculation as zero. For example, if you worked for 30 years, five years of zero earnings would be added to your record to complete the 35-year span. This naturally lowers your overall average indexed monthly earnings and, consequently, your Primary Insurance Amount (PIA). This underscores the importance of a long and consistent work history in maximizing your Social Security benefits. Even a few years of high earnings can significantly impact your benefit if they replace years of zero or very low earnings in the 35-year calculation.

Calculating Your Primary Insurance Amount (PIA)

Once your indexed earnings are established, the next crucial step is calculating your Primary Insurance Amount (PIA). The PIA is the monthly benefit you would receive if you start receiving benefits at your Full Retirement Age (FRA). It’s the benchmark from which early or delayed retirement benefits are adjusted.

From Indexed Earnings to Average Indexed Monthly Earnings (AIME)

With your 35 highest-earning years (after indexing) identified, the SSA sums these indexed earnings and divides the total by 420 (which is 35 years multiplied by 12 months). The result is your Average Indexed Monthly Earnings (AIME). This figure represents your average monthly earnings over your most productive working years, adjusted for inflation. The AIME is not your actual monthly benefit, but rather an intermediate step, a key input into the final benefit formula. It’s a critical metric because a higher AIME directly translates to a higher PIA, assuming all other factors remain constant. Understanding your AIME allows you to gauge the potential value of your future benefit before adjustments for claiming age.

Bend Points: Progressivity in Action

The Social Security benefit formula is designed to be progressive, meaning it replaces a higher percentage of pre-retirement earnings for lower-income workers than for higher-income workers. This is achieved through a system called “bend points.” The PIA calculation involves applying three different percentage factors to segments of your AIME. For any given year, there are specific “bend points” – dollar amounts that delineate these segments.

For example, for someone turning 62 in 2024:

- 90% of the first $1,174 of their AIME

- 32% of their AIME between $1,174 and $7,078

- 15% of their AIME above $7,078

These bend points are adjusted annually based on the national average wage index. This progressive structure ensures that even those with lower lifetime earnings receive a meaningful benefit, providing a vital safety net, while still allowing higher earners to receive a larger absolute benefit, albeit a smaller percentage of their pre-retirement income. The goal is to strike a balance between social adequacy and individual equity.

The Result: Your Basic Monthly Benefit

The sum of these three calculations – 90% of the first segment, 32% of the second, and 15% of the third – yields your Primary Insurance Amount (PIA). This is the amount you are entitled to receive each month if you claim your benefits precisely at your Full Retirement Age (FRA). It’s crucial to remember that the PIA is a starting point. It doesn’t account for any adjustments due to claiming benefits early or late, or for Cost-of-Living Adjustments (COLAs) that may have occurred after your initial benefit determination. Your PIA is the core value from which all other calculations, such as spousal benefits or survivor benefits, are typically derived. Understanding how your PIA is calculated empowers you to better estimate your future income in retirement and plan accordingly.

The Impact of Claiming Age: Early, Full, and Delayed Retirement

While your PIA is determined by your earnings history, the actual amount you receive each month can vary significantly based on when you decide to start claiming your Social Security benefits. This decision is one of the most critical factors in determining your total lifetime benefits.

Full Retirement Age (FRA): The Benchmark

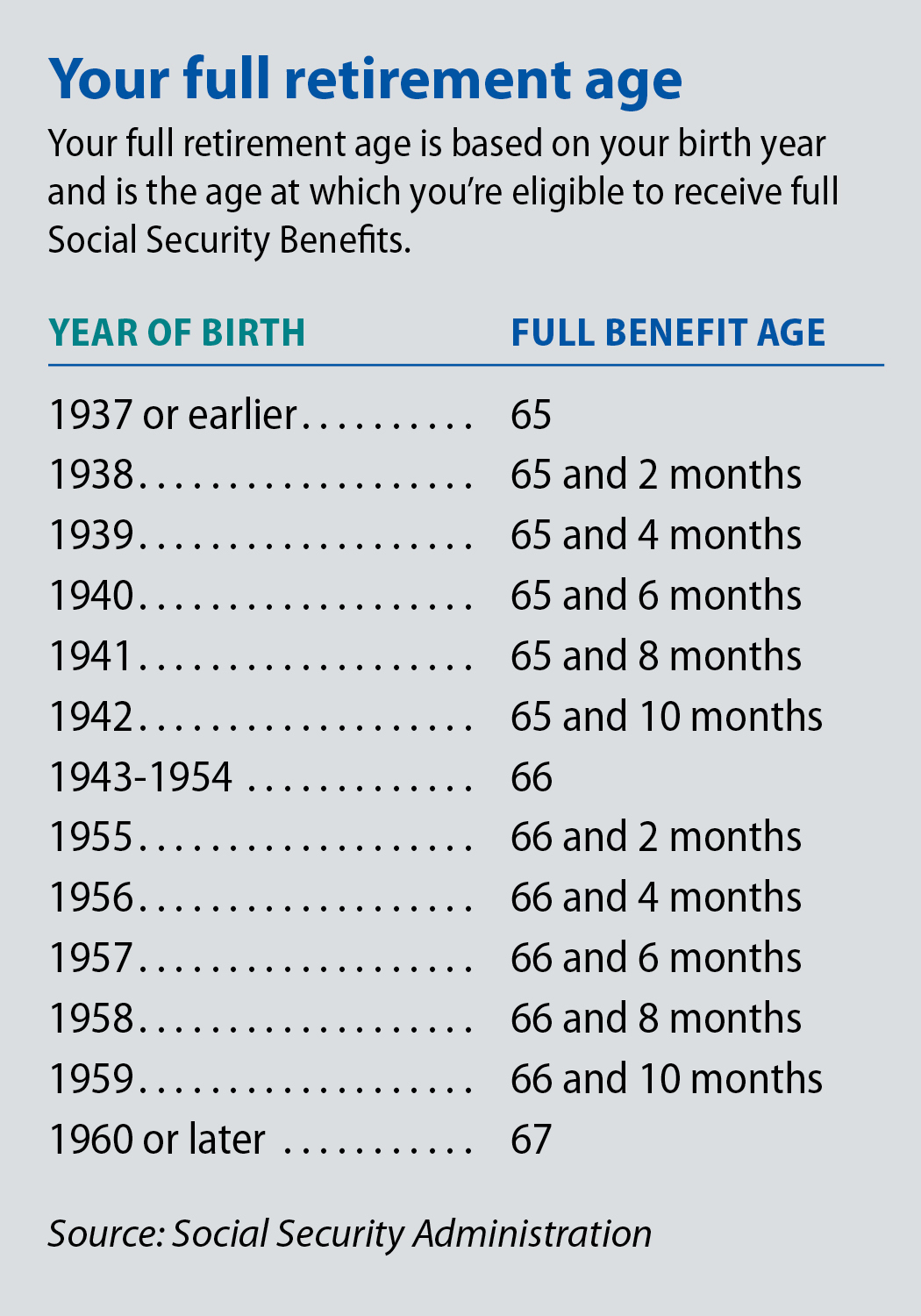

Your Full Retirement Age (FRA) is the age at which you are entitled to receive 100% of your Primary Insurance Amount (PIA). This age varies depending on your birth year. For those born between 1943 and 1954, FRA is 66. For those born in 1960 or later, FRA is 67. For birth years in between, it gradually increases from 66 to 67. Knowing your specific FRA is fundamental, as it serves as the benchmark against which early or delayed claiming adjustments are made. Claiming exactly at your FRA means you receive precisely your calculated PIA, without any reduction or increase for age. It’s the neutral point in the claiming decision.

Claiming Early: Reductions and Long-Term Implications

You can begin receiving Social Security retirement benefits as early as age 62. However, choosing to claim before your FRA results in a permanent reduction of your monthly benefit. The reduction amount depends on how many months prior to your FRA you start receiving benefits. For example, if your FRA is 67 and you claim at 62, your benefit would be reduced by approximately 30%. This reduction is applied to your PIA and generally remains in effect for the rest of your life. While claiming early provides income sooner, it means accepting a lower monthly payment for potentially many years. This decision often appeals to individuals who need the income, face health challenges, or prefer to retire sooner. However, it’s a trade-off that should be carefully considered against your expected lifespan and overall financial needs.

Claiming Late: Maximizing Benefits with Delayed Retirement Credits

Conversely, if you delay claiming your Social Security benefits past your FRA, you can earn “Delayed Retirement Credits” (DRCs). These credits permanently increase your monthly benefit amount. For each year you delay claiming beyond your FRA, up to age 70, your benefit increases by a certain percentage, typically 8% per year. This means that if your FRA is 67 and you delay claiming until age 70, your monthly benefit would be 124% of your PIA (100% + 3 years * 8% per year). There is no additional benefit increase for delaying past age 70, so there’s no financial incentive to wait beyond that point. Delaying benefits is often a powerful strategy for individuals who are in good health, have other sources of income, and expect to live a long life, as it provides a significantly larger guaranteed income stream for the rest of their retirement. This strategy can act as a form of longevity insurance, protecting against the risk of outliving other savings.

Beyond Your Own Earnings: Spousal, Survivor, and Disability Benefits

Social Security isn’t just for primary earners; it extends its protective umbrella to family members and those who become disabled, offering derivative benefits that are tied to a worker’s earnings record. Understanding these additional facets is crucial for comprehensive financial planning.

Derivative Benefits: How Family Members Can Qualify

Beyond an individual’s own retirement benefit, Social Security provides benefits to certain family members based on that individual’s work record. These are known as derivative benefits.

- Spousal Benefits: A spouse can claim benefits based on their living spouse’s work record if it’s higher than their own. Generally, a spouse can receive up to 50% of the higher-earning spouse’s PIA. To qualify, the spouse must typically be at least 62 or caring for a child under age 16 or disabled.

- Survivor Benefits: If a worker dies, their surviving spouse, dependent children, or even dependent parents may be eligible for benefits. A surviving spouse can receive up to 100% of the deceased worker’s benefit if they claim at their own FRA (or at a reduced rate if claiming earlier, starting at age 60, or 50 if disabled). Minor children (under 18 or 19 if still in high school) and disabled adult children may also receive benefits.

- Divorced Spousal Benefits: A divorced spouse may also qualify for benefits based on their ex-spouse’s record, provided the marriage lasted at least 10 years, they are currently unmarried, and are at least 62 years old. This can be claimed even if the ex-spouse has not yet filed for benefits, provided they are at least 62 and the divorce has been final for at least two years.

These derivative benefits play a vital role in protecting families from financial hardship due to retirement, death, or disability of a primary earner.

The Deemed Filing Rule and Its Exceptions

The “deemed filing” rule significantly impacts how spouses can claim benefits. For anyone born on or after January 2, 1954, if you file for any Social Security retirement or spousal benefit, you are “deemed” to have filed for all benefits for which you are eligible. This means you cannot selectively claim one benefit (e.g., spousal benefits) while allowing your own retirement benefit to grow through Delayed Retirement Credits. You will automatically be paid the higher of the two benefits, but only one is paid out.

There are, however, exceptions:

- Caring for a child: If you are claiming spousal benefits while caring for a child under 16 or disabled, the deemed filing rule does not apply.

- Disability benefits: If you are receiving Social Security disability benefits, the rule generally does not apply.

- Divorced spouses: A divorced spouse may still be able to file for benefits on their ex-spouse’s record without being deemed to have filed for their own, allowing their personal benefit to continue growing.

Understanding deemed filing is critical for married couples (and divorced individuals) to strategize their claiming decisions effectively and avoid inadvertently compromising potential benefits.

Navigating Disability Claims and Work Credits

Social Security Disability Insurance (SSDI) provides income to individuals who are unable to work due to a severe medical condition expected to last at least a year or result in death. Eligibility for SSDI is also tied to your work history, specifically the number of “work credits” you have accumulated. Work credits are earned by paying Social Security taxes on your earnings. In 2024, you earn one credit for every $1,730 in earnings, up to a maximum of four credits per year.

The number of credits needed for disability benefits depends on your age when you become disabled:

- Under age 24: You need 6 credits earned in the 3-year period ending when your disability starts.

- Age 24 to 31: You generally need credits for half the time between age 21 and the time you become disabled.

- Age 31 or older: You generally need 20 credits in the 10-year period ending when your disability starts, and a total of 40 credits.

These work credit requirements are distinct from those for retirement benefits (which generally require 40 credits over your lifetime). SSDI is a crucial component of the Social Security system, offering financial protection when illness or injury prevents an individual from sustaining their livelihood, further highlighting the program’s broad scope beyond just retirement.

Strategic Planning for Social Security and Retirement

Social Security should not be viewed in isolation but as an integral part of your comprehensive retirement plan. Strategic planning can help you maximize your benefits and ensure a more secure financial future.

Reviewing Your Social Security Statement Regularly

The Social Security Administration provides an annual statement detailing your earnings record, estimated benefits at different claiming ages (early, full, and delayed), and potential disability and survivor benefits. This statement is an invaluable tool for retirement planning. You can access your statement online by creating an account at my Social Security. It is critical to review your earnings record regularly to ensure its accuracy. Errors in your reported earnings, even minor ones, can have a significant impact on your future benefits, as your benefits are directly derived from this record. Correcting any discrepancies early on can prevent considerable financial headaches down the line. Beyond accuracy, the statement provides personalized estimates, allowing you to project your future income and assess how Social Security will fit into your broader financial picture.

Integrating Social Security into Your Broader Financial Plan

Social Security, while substantial for many, is generally intended to replace only a portion of your pre-retirement income – on average, about 40% for typical earners. Therefore, it’s crucial to integrate your estimated Social Security benefits with other retirement savings vehicles, such as 401(k)s, IRAs, pensions, and personal investments.

- Gap Analysis: Use your estimated Social Security benefit to determine any potential income gap you’ll need to fill with personal savings.

- Drawing Down Savings: Your Social Security claiming strategy can influence how and when you draw down your other retirement assets. For instance, delaying Social Security until age 70 might mean drawing more heavily from your personal savings in your early retirement years, but then enjoying a larger, inflation-adjusted, and guaranteed income stream later.

- Tax Planning: A portion of Social Security benefits may be taxable depending on your “provisional income.” Integrating this into your overall tax strategy, along with distributions from other retirement accounts, is essential for optimizing your after-tax income.

- Healthcare Costs: Social Security does not cover healthcare costs directly. Planning for Medicare premiums, deductibles, and out-of-pocket expenses is a separate but related component of retirement financial planning.

A holistic view ensures that all pieces of your financial puzzle work together to support your desired lifestyle in retirement.

The Future of Social Security: Understanding Potential Changes

While Social Security has been a bedrock of American retirement for decades, its long-term financial stability is a subject of ongoing debate. Demographic shifts, such as lower birth rates and increased longevity, mean fewer workers are contributing per beneficiary, putting pressure on the system. The Social Security Trustees regularly publish reports projecting that the trust funds will be able to pay 100% of promised benefits for a limited number of years, after which it will only be able to pay a reduced percentage if no legislative changes are made.

Potential future changes could include:

- Adjustments to the Full Retirement Age: A gradual increase in FRA.

- Changes to the Taxable Maximum: Raising the earnings limit subject to Social Security taxes.

- Benefit Formula Modifications: Altering the PIA calculation, potentially adjusting bend points or indexing methods.

- Means-Testing: Introducing an income threshold above which benefits are reduced.

- Changes to Cost-of-Living Adjustments (COLAs): Altering how COLAs are calculated.

While it’s highly unlikely that Social Security will disappear entirely, it’s prudent for individuals to stay informed about potential reforms. Financial planning should factor in the possibility of future adjustments to benefits, emphasizing the importance of diversified retirement savings and not solely relying on Social Security to fund your entire retirement. Understanding the system’s challenges empowers you to advocate for its future and adjust your personal planning accordingly.

The question “how many years is Social Security based on?” unveils a complex yet meticulously designed system. From the “best 35 years” rule that shapes your AIME, to the progressive bend points determining your PIA, and finally to the critical decision of when to claim your benefits, every factor plays a role in your financial well-being during retirement. Social Security is more than just a government program; it’s a testament to collective responsibility, providing essential support for millions. By thoroughly understanding its mechanics, leveraging available tools like your annual statement, and integrating it wisely into your broader financial strategy, you can make informed decisions that pave the way for a more secure and predictable retirement. While the system faces future challenges, its foundational principles remain crucial for countless individuals and families across the nation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.