In the landscape of American retail, few entities command the financial respect and consumer loyalty of Costco Wholesale Corporation. While casual shoppers may frequent the warehouse for bulk groceries and the legendary $1.50 hot dog combo, financial analysts and business strategists look at the company through a different lens: a masterclass in capital allocation and operational efficiency. When asking “how many Costco stores are in the US,” one isn’t just counting buildings; they are measuring the reach of a multi-billion dollar financial engine that has redefined the “low margin, high volume” business model.

As of late 2023 and moving into 2024, Costco operates approximately 600 warehouses across the United States and Puerto Rico. This number represents the backbone of a global empire that consistently ranks among the top retailers in the world. However, the true story lies in the strategic placement of these locations and how each unit contributes to a financial ecosystem that prioritizes long-term stability over short-term spikes.

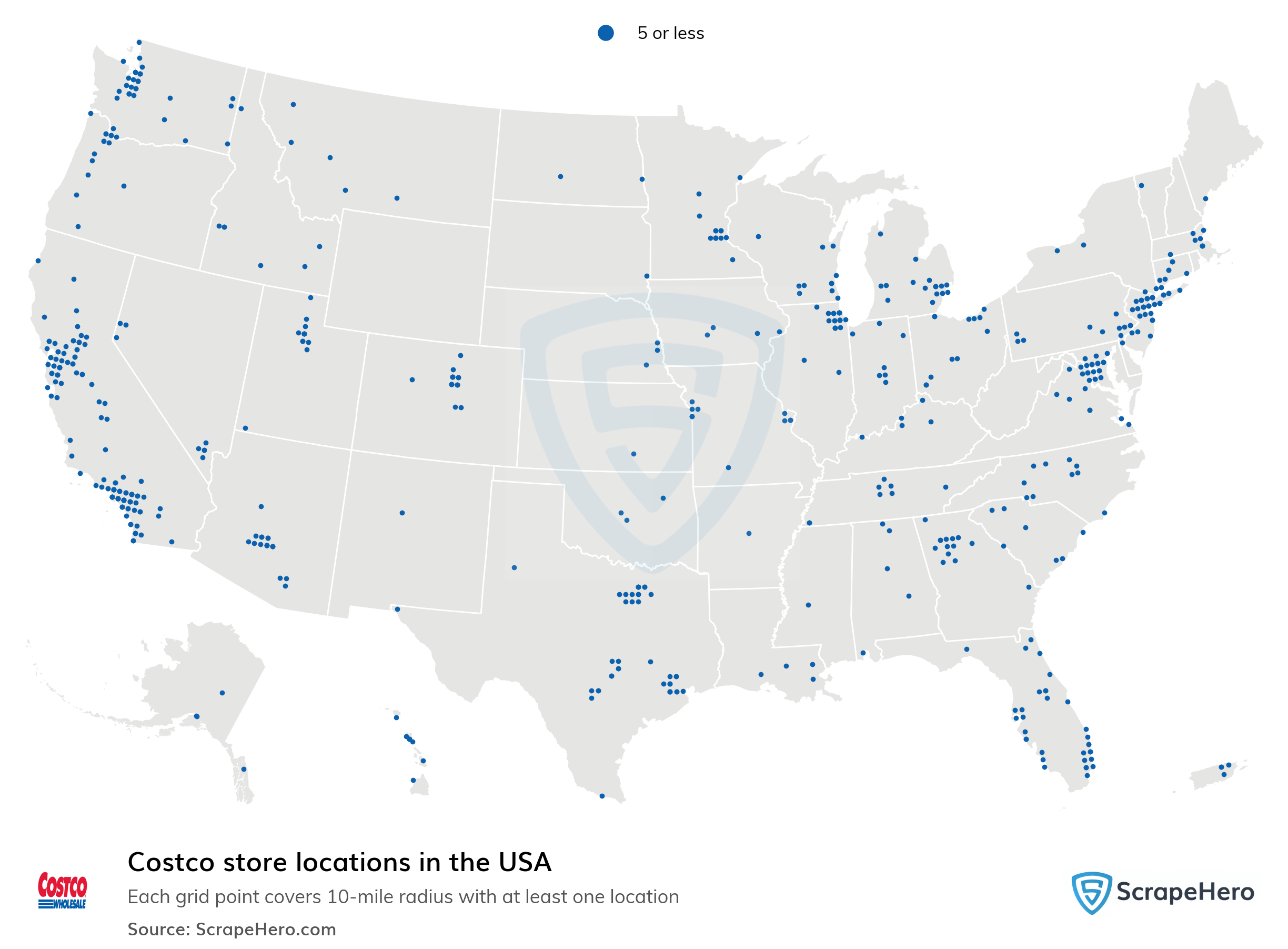

The Quantitative Landscape: Breaking Down Costco’s US Store Count

The sheer number of Costco locations in the United States is a testament to the company’s disciplined approach to growth. Unlike competitors who might oversaturate markets to the point of cannibalizing their own sales, Costco utilizes a rigorous site-selection process that ensures each new warehouse meets specific demographic and income thresholds.

Regional Distribution and Market Saturation

The geographic distribution of Costco stores is heavily weighted toward high-population, high-income regions. California leads the nation by a significant margin, housing over 130 locations—roughly 20% of the company’s total US footprint. Other major hubs include Texas, Washington, and Florida.

From a financial perspective, this concentration is strategic. By clustering stores in regions with higher disposable income, Costco ensures that its membership-based model thrives. The company doesn’t just look for shoppers; it looks for households with the financial capacity to buy in bulk and the storage space to house those purchases. This regional dominance creates a “moat” around the business, making it incredibly difficult for other wholesale clubs or traditional grocers to gain a foothold in these lucrative markets.

The Correlation Between Store Density and Revenue Growth

There is a direct mathematical relationship between the number of Costco stores and the company’s top-line revenue. Each US warehouse generates, on average, over $250 million in annual sales. When you multiply this by a growing fleet of 600+ stores, the result is a massive cash flow that allows the company to reinvest in its infrastructure without taking on excessive debt.

The steady increase in store count—usually adding between 20 to 30 locations globally per year—is a calculated move to maintain a “steady state” of growth. This predictability is a cornerstone of Costco’s appeal to institutional investors. By maintaining a slow but consistent expansion, the company avoids the pitfalls of “hyper-expansion” that have led to the downfall of other retail giants.

The Membership Model: Turning Footprint into Recurring Revenue

To understand the financial power behind the number of Costco stores, one must look past the physical goods on the shelves. Costco is not a traditional retailer in the sense that it profits from the markup on products; rather, it is a subscription service that provides access to goods at near-cost prices.

Membership Fees as a High-Margin Profit Engine

The true genius of the Costco financial model lies in its membership fees. In the United States, an Gold Star membership costs $60 annually, while the Executive membership costs $120. While the number of stores is around 600, the number of cardholders is in the tens of millions.

Financially, these fees are almost pure profit. Because Costco operates on razor-thin margins for its products—capping markups at approximately 14% to 15%, compared to 25% or 30% at traditional supermarkets—the membership revenue accounts for the vast majority of the company’s operating income. This creates a “negative working capital” cycle that is the envy of the financial world. The company receives cash from members upfront, which provides a massive pool of liquidity to fund operations and inventory before a single item is even sold.

Retention Rates and Lifetime Customer Value

The strength of the US store count is reinforced by an staggering membership renewal rate, which consistently hovers around 92-93% in North America. This high retention rate signifies a deep “stickiness” in the consumer’s financial life. Once a household pays the membership fee, they are psychologically and financially incentivized to maximize their “investment” by shopping at Costco as frequently as possible.

From a business finance standpoint, this creates a highly predictable revenue stream. Analysts can project future earnings with a high degree of accuracy because the base of the income—memberships—is stable. This stability allows Costco to maintain a premium valuation in the stock market, as it functions more like a recurring-revenue tech company than a volatile retail business.

Real Estate and Operational Efficiency: The Business Finance Behind the Big Box

Every Costco store in the US is designed with a singular focus: minimizing overhead to maximize value for the member. The “warehouse” is not just a branding term; it is a literal description of the company’s approach to asset management.

Asset Management and the “Warehouse” Philosophy

Costco’s real estate strategy is a masterclass in efficiency. Most locations are “no-frills” environments with concrete floors, exposed rafters, and goods displayed on original shipping pallets. By eliminating the costs associated with elaborate retail displays and expensive interior design, Costco significantly lowers its capital expenditure per square foot.

Furthermore, Costco owns a significant portion of its real estate. In an era where many retailers are burdened by high-interest leases or sale-leaseback agreements that drain cash, Costco’s ownership of its land and buildings provides a massive hedge against inflation and rising real estate costs. This “owned asset” model strengthens the balance sheet and provides the company with tangible collateral, lowering its overall cost of capital.

Supply Chain Optimization as a Cost-Saving Tool

The efficiency of the 600+ US stores is further bolstered by an ultra-lean supply chain. A typical Costco warehouse stocks only about 4,000 Stock Keeping Units (SKUs), whereas a standard Walmart or Target may stock upwards of 100,000.

This limited selection is a deliberate financial strategy. By moving massive volumes of a small number of items, Costco gains incredible bargaining power with suppliers. They can negotiate the lowest possible prices because they represent a significant portion of a supplier’s total distribution. This volume-based pricing is passed directly to the consumer, which in turn reinforces the value of the membership, completing the “virtuous cycle” of the Costco business model.

Costco as an Investment Vehicle: Evaluating Stock Performance (COST)

For those looking at Costco through the lens of personal finance and investing, the store count is a primary indicator of the company’s upward trajectory. The stock (NASDAQ: COST) has historically outperformed the S&P 500, driven by the company’s disciplined management and consistent returns.

Dividend Growth and Shareholder Value

Costco has established itself as a reliable dividend payer, but it is perhaps best known for its “Special Dividends.” Periodically, when the company has accumulated excess cash on its balance sheet—often as a result of successful US expansion and high membership renewals—it returns that capital to shareholders in large, one-time payments.

This practice demonstrates a commitment to shareholder value that is rare in the retail sector. Instead of wasting capital on ill-advised acquisitions or excessive executive bonuses, the company distributes its wealth back to those who have invested in its growth. This makes Costco a favorite for long-term “buy and hold” portfolios focused on wealth accumulation.

Future Outlook: Domestic Expansion vs. International Diversification

While the 600+ stores in the US form the core of the company’s financial strength, the question of “how many more” remains. Analysts believe there is still significant “white space” in the US market, particularly in the Midwest and Northeast, where store density is lower than in the West.

However, the next phase of Costco’s financial growth likely involves taking the lessons learned from the US market and applying them internationally. The success of locations in China, Iceland, and France suggests that the “membership warehouse” model is globally portable. For an investor, the US store count represents a stable foundation, while international expansion represents the “growth kicker” that could drive the stock price for the next two decades.

Conclusion: The Bottom Line on Costco’s Footprint

When we count the number of Costco stores in the US, we are looking at more than just a retail map. We are looking at a highly optimized financial machine that has mastered the art of consumer psychology and corporate finance. With roughly 600 locations serving as the primary touchpoints for a multi-billion dollar membership engine, Costco has created a business model that is remarkably resilient to economic downturns.

For the consumer, the number represents convenience and savings. For the business analyst, it represents a benchmark of operational excellence. And for the investor, it represents a fortress-like balance sheet built on the solid ground of recurring revenue and owned assets. As Costco continues to methodically add to its US store count, its position as a dominant force in the world of finance and retail remains undisputed.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.