Navy Federal Credit Union (NFCU) is the largest natural member credit union in the United States, serving millions of military members, veterans, and their families. For many of these members, Navy Federal’s suite of credit cards—ranging from the CashRewards to the Flagship Rewards—represents a cornerstone of their financial life. However, maintaining financial health requires more than just making purchases; it requires a granular understanding of how billing statements work, how many you should expect, and how to interpret the data they contain.

In this guide, we will dive deep into the mechanics of Navy Federal credit card billing statements, offering professional insights into managing your accounts, optimizing your payment cycles, and leveraging the tools provided by the credit union to build a robust financial future.

The Fundamentals of Navy Federal Billing Cycles and Statements

Every credit card holder at Navy Federal operates on a “billing cycle.” This is the interval between the days when your statements are generated. Understanding the rhythm of these cycles is the first step toward mastering your personal finances.

Defining the Billing Cycle Duration

A standard billing cycle at Navy Federal typically lasts between 28 and 31 days. This cycle does not necessarily align with the first day of the month. Instead, your cycle begins on the day your account was opened or a date assigned by the credit union. During this period, all your transactions, credits, and interest charges are recorded. At the end of these 30-odd days, Navy Federal “closes” the books for that period and generates your billing statement.

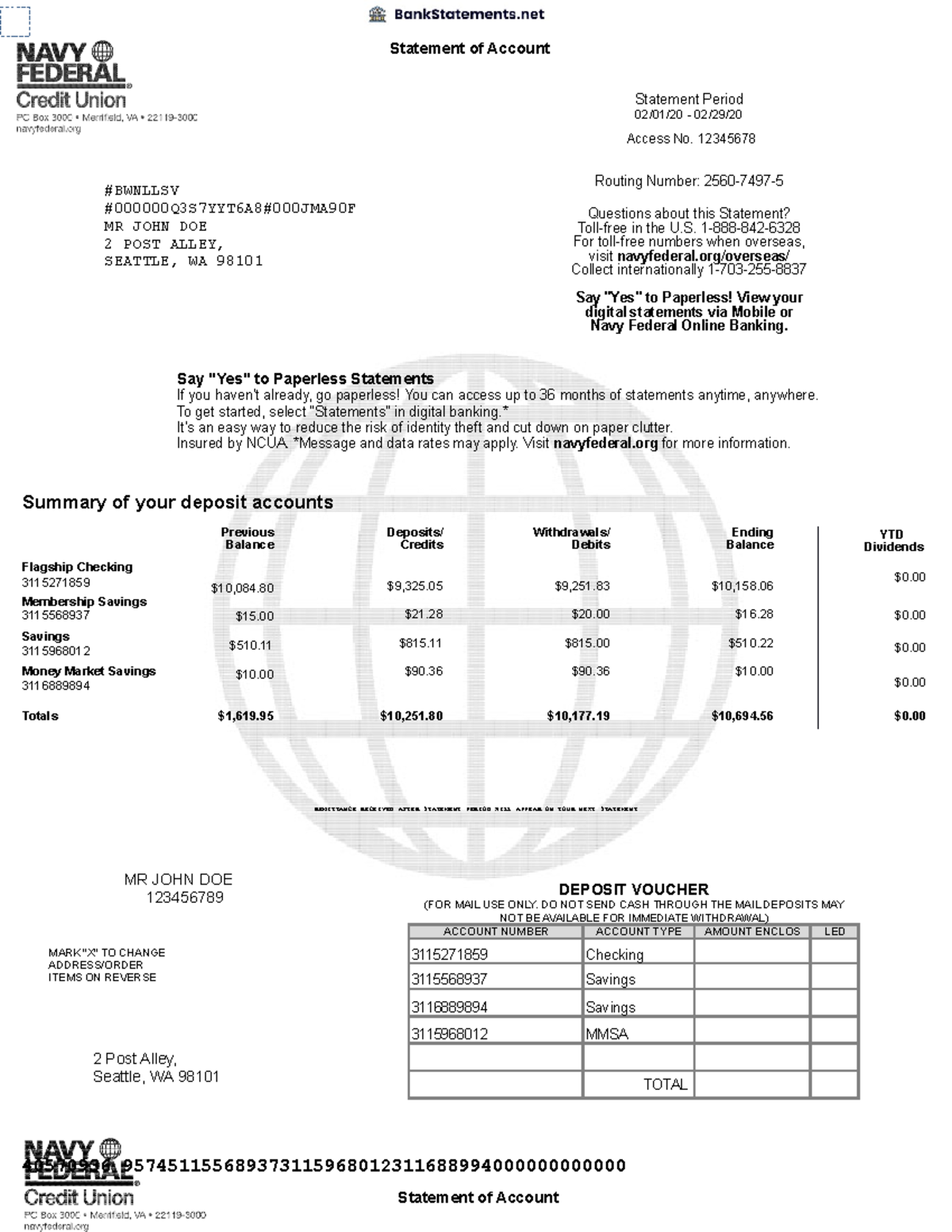

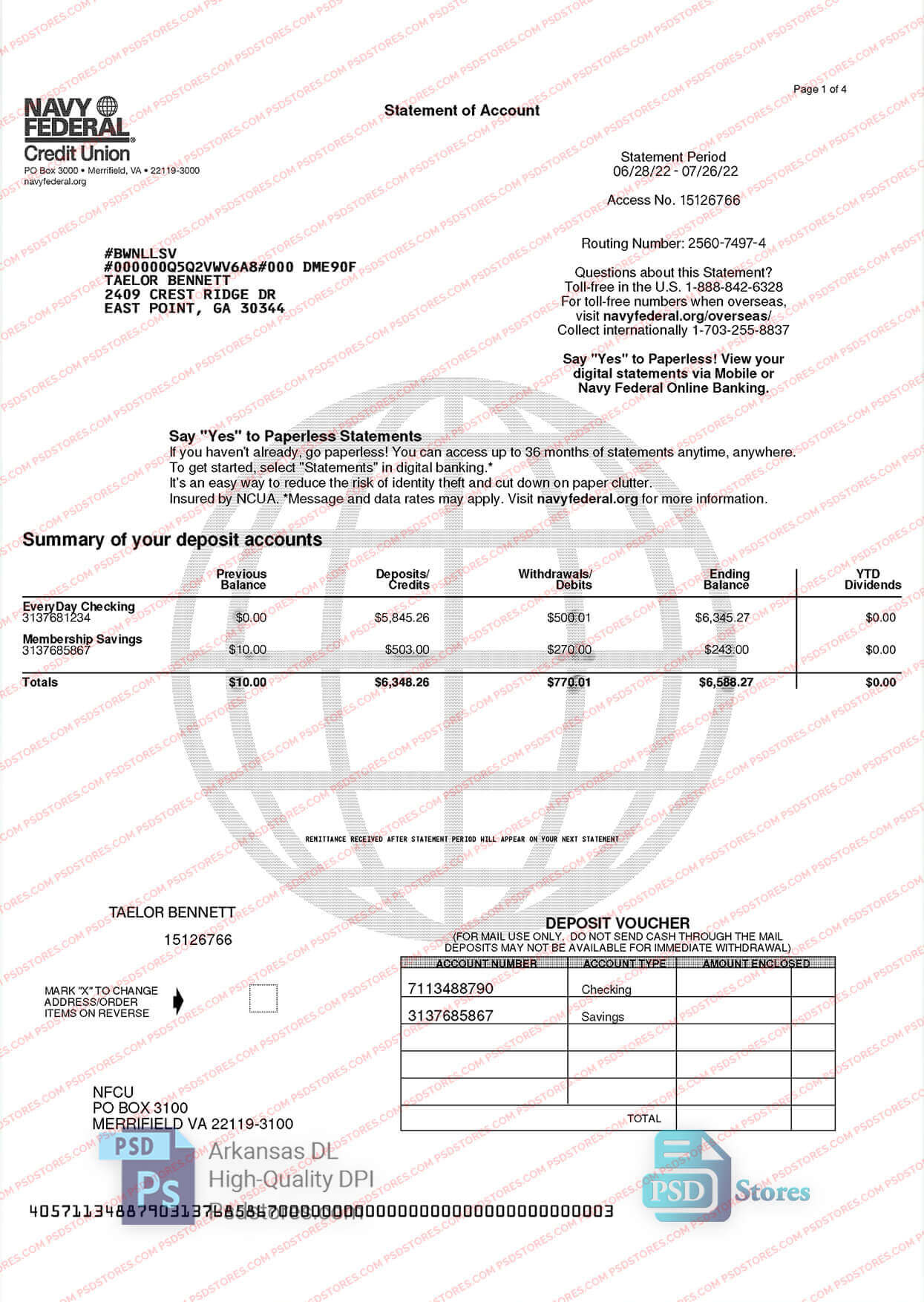

How Many Statements Should You Expect per Year?

A common question for new cardholders is: “How many billing statements will I receive?” For each individual credit card account you hold with Navy Federal, you will receive exactly 12 billing statements per year—one for each monthly cycle.

If you hold multiple cards—for example, a More Rewards American Express® Card and a Platinum Card—you will receive a separate statement for each. This means if you have three different Navy Federal credit cards, you are responsible for managing 36 statements annually. Keeping track of these is vital because each statement carries its own unique due date, minimum payment, and credit limit.

The Importance of the Statement Closing Date vs. Due Date

One of the most critical distinctions in personal finance is the difference between the statement closing date and the payment due date.

- Statement Closing Date: This is the day the billing cycle ends. The balance on your account at this exact moment is what Navy Federal reports to the three major credit bureaus (Equifax, Experian, and TransUnion).

- Payment Due Date: This is typically 21 to 25 days after the closing date. To avoid late fees and maintain a positive payment history, you must pay at least the minimum amount by this date.

Navigating Your Digital and Paper Statements

In the modern era of banking, the way we interact with our financial data has shifted from physical mail to digital interfaces. Navy Federal provides several avenues to access your billing information, ensuring transparency and ease of use.

Accessing Statements via the Navy Federal Mobile App

The Navy Federal mobile app is a powerhouse tool for personal finance management. To find your statements, you simply log in, select the specific credit card account, and navigate to the “Statements” or “Documents” section. The app allows you to view the last several years of statement history in PDF format. This is particularly useful for members who are traveling or stationed overseas and need immediate access to their financial records.

Leveraging Online Banking for Statement History

For those who prefer a desktop experience, the Navy Federal online banking portal offers a more expansive view of your financial history. Here, you can not only view statements but also download transaction data into software like Quicken or Excel. This functionality is essential for members who practice strict budgeting or need to track business expenses on a personal card.

Going Green: The Benefits of Paperless Statements

Navy Federal encourages members to opt for paperless statements. From a financial security perspective, paperless is often superior. Physical mail can be stolen, leading to identity theft. Digital statements are protected by multi-factor authentication. Furthermore, opting for digital delivery often simplifies record-keeping, as you no longer have to manage physical filing cabinets of sensitive financial data.

Managing Multiple Credit Card Accounts and Statements

Many Navy Federal members utilize a “ladder” strategy with their credit cards, using different cards for different spending categories (e.g., one for groceries, one for travel). Managing the influx of statements requires a strategic approach.

Strategy for Staggered Due Dates

If you have multiple Navy Federal statements, you might find that their due dates are scattered throughout the month. This can be stressful for cash flow management. A professional financial tip is to contact Navy Federal and request to move your due dates. By aligning all your credit card statements to close around the same time—perhaps shortly after you receive your mid-month or end-of-month military pay—you can simplify your monthly bill-paying ritual and ensure you never miss a deadline.

Consolidating Your View: The Dashboard Experience

When you log into your Navy Federal account, you are presented with a dashboard. This dashboard provides a high-level summary of all your accounts. For credit cards, it will show the “Current Balance” and the “Statement Balance.”

It is important to understand the difference:

- Statement Balance: The amount you owed when the last billing cycle ended.

- Current Balance: The statement balance plus any new purchases made since the closing date, minus any payments.

To avoid paying interest, you should always aim to pay the “Statement Balance” in full by the due date.

Monitoring for Fraud and Errors Across Multiple Cards

With multiple statements comes the increased responsibility of auditing. Every month, you should reconcile your receipts with your billing statement. Navy Federal has robust fraud protection, but the first line of defense is the member. Look for “zombie subscriptions”—recurring charges for services you no longer use—and any unauthorized transactions. Catching these errors on the statement early allows you to dispute them within the 60-day window typically required by the Fair Credit Billing Act.

Optimizing Your Financial Health Through Statement Analysis

A billing statement is more than a bill; it is a financial diagnostic tool. By analyzing the data within your Navy Federal statements, you can make informed decisions that improve your credit score and long-term wealth.

Tracking Your Spending Categories

Navy Federal often categorizes your spending on your annual or monthly summaries. By looking at these categories, you can identify “lifestyle creep.” If your statements show a consistent increase in “Dining Out” or “Entertainment” while your “Savings” remain stagnant, it may be time to re-evaluate your budget.

Understanding Interest Charges and APR Calculations

If you carry a balance, your statement will include a “Minimum Payment Warning” and an “Interest Charge Calculation” section. These are required by federal law and are incredibly eye-opening. The statement will show you exactly how many years it would take to pay off your balance if you only made the minimum payment, and how much total interest you would pay. Using this information can motivate you to pay more than the minimum to preserve your capital.

Utilizing Statements for Tax Preparation and Budgeting

For members who are self-employed or have deductible expenses, credit card statements are vital during tax season. Navy Federal’s year-end summaries aggregate your spending into a single document, making it significantly easier to identify deductible business expenses, charitable donations, or medical costs.

Frequently Asked Questions Regarding Navy Federal Billing

To wrap up this guide, let’s address some of the practical concerns members often have regarding their statements.

What to Do if a Statement is Missing?

If a billing cycle ends and you do not see a statement generated, it is usually because there was no activity on the card and a zero balance during that period. However, if you know you used the card and the statement is missing, you should contact Navy Federal immediately. Technical glitches are rare but possible, and “not receiving a bill” is not a legal excuse for missing a payment.

How Long Does Navy Federal Keep Statement Archives?

Typically, Navy Federal provides digital access to at least the last 36 to 72 months of statements. If you need records older than seven years—perhaps for a complex IRS audit or legal matter—you may need to request archived copies for a small fee. It is a best practice to download your December statement every year and save it to a secure cloud drive to ensure you have a permanent record.

The Impact of Statement Balances on Your Credit Score

Finally, remember that the “Statement Balance” is what determines your credit utilization ratio. If you have a $10,000 limit and your statement closes with a $9,000 balance, your utilization is 90%, which can hurt your credit score—even if you pay it off in full a few days later. To optimize your score, many financial experts recommend paying your balance down before the statement closing date, so the statement reflects a lower utilization (ideally under 10%).

By treating your Navy Federal billing statements as a roadmap rather than just a monthly obligation, you can take full control of your financial journey, ensuring that every dollar spent is a step toward greater financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.