The question “how many banks in America?” might seem straightforward, but its answer is anything but static. It’s a dynamic figure that reflects the constant evolution of the U.S. financial system, influenced by economic cycles, technological advancements, regulatory shifts, and consumer behavior. More than just a simple tally, understanding this number and the underlying trends provides crucial insights into the health, structure, and future direction of personal finance, business lending, and the broader economy. For individuals managing their money, entrepreneurs seeking capital, or investors monitoring market trends, grasping the diverse landscape of American banking is paramount.

The Evolving Count: A Dynamic Financial Ecosystem

At any given moment, the precise number of banks in America is a moving target. The U.S. financial system is famously diverse and decentralized, a stark contrast to many other developed nations with a smaller number of dominant banking institutions. This vast network includes a mix of large national banks, regional powerhouses, community-focused institutions, and member-owned credit unions, each playing a vital role in facilitating economic activity.

Decoding the “Bank” Definition: What Counts?

Before diving into figures, it’s essential to define what constitutes a “bank” for counting purposes. Generally, when discussing “banks,” we primarily refer to commercial banks and savings institutions (like savings banks and savings and loan associations) that are federally or state-chartered and accept deposits insured by the Federal Deposit Insurance Corporation (FDIC). This definition excludes investment banks that don’t take deposits, foreign bank branches, and non-bank financial institutions like shadow banks or FinTech companies, even though these entities also perform banking-like functions. Credit unions, while functionally similar and often serving the same consumer needs, are typically counted separately due to their cooperative, member-owned structure and different regulatory oversight (National Credit Union Administration, NCUA).

The Latest Figures: A Snapshot of the Banking Sector

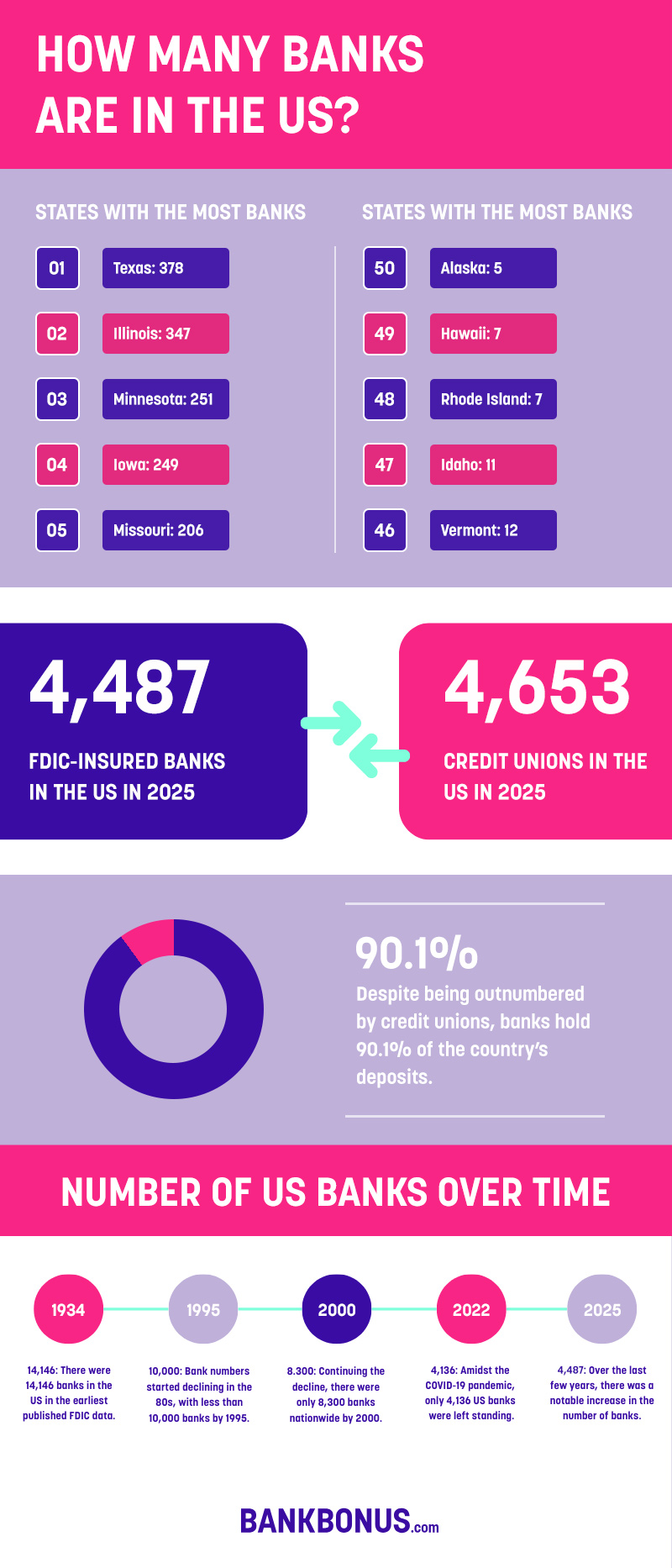

As of recent reporting periods (e.g., Q4 2023 or Q1 2024, depending on the latest available data from the FDIC), the number of FDIC-insured commercial banks and savings institutions in the United States typically hovers around 4,600 to 4,700. This figure represents a significant decline from historical highs, as the industry has experienced decades of consolidation. For instance, in 1985, there were over 14,000 FDIC-insured institutions. This reduction, however, does not necessarily mean a reduction in banking services; rather, it reflects a shift towards fewer, larger entities and more efficient operations.

When considering credit unions, the number adds significantly to the institutional count. The NCUA typically reports around 4,600 to 4,700 federally insured credit unions. Therefore, if one considers all deposit-taking institutions, including both banks and credit unions, the total count often approaches or slightly exceeds 9,000 unique institutions. This combined figure paints a more complete picture of the retail financial services landscape accessible to the average American.

Key Regulatory Bodies: FDIC, OCC, and NCUA

Understanding the regulatory framework is crucial to comprehending the structure and stability of the U.S. banking system.

- Federal Deposit Insurance Corporation (FDIC): The FDIC insures deposits up to $250,000 per depositor, per insured bank, for each account ownership category. This insurance is a cornerstone of public trust in the banking system. The FDIC also examines and supervises state-chartered banks that are not members of the Federal Reserve System.

- Office of the Comptroller of the Currency (OCC): The OCC charters, regulates, and supervises all national banks and federal savings associations. It ensures that these institutions operate in a safe and sound manner, provide fair access to financial services, and comply with applicable laws and regulations.

- National Credit Union Administration (NCUA): The NCUA serves a similar role for credit unions as the FDIC does for banks, insuring deposits and supervising federally insured credit unions.

These bodies, along with the Federal Reserve System (which supervises state-chartered banks that are members of the Federal Reserve System and all bank holding companies), work in concert to maintain a stable and robust financial infrastructure.

Beyond the Numbers: Understanding Bank Types and Their Roles

The raw count of financial institutions doesn’t fully capture the diversity of banking services available. The U.S. system is characterized by different types of banks, each with a distinct focus and serving specific segments of the population and economy.

Commercial Banks: The Backbone of American Finance

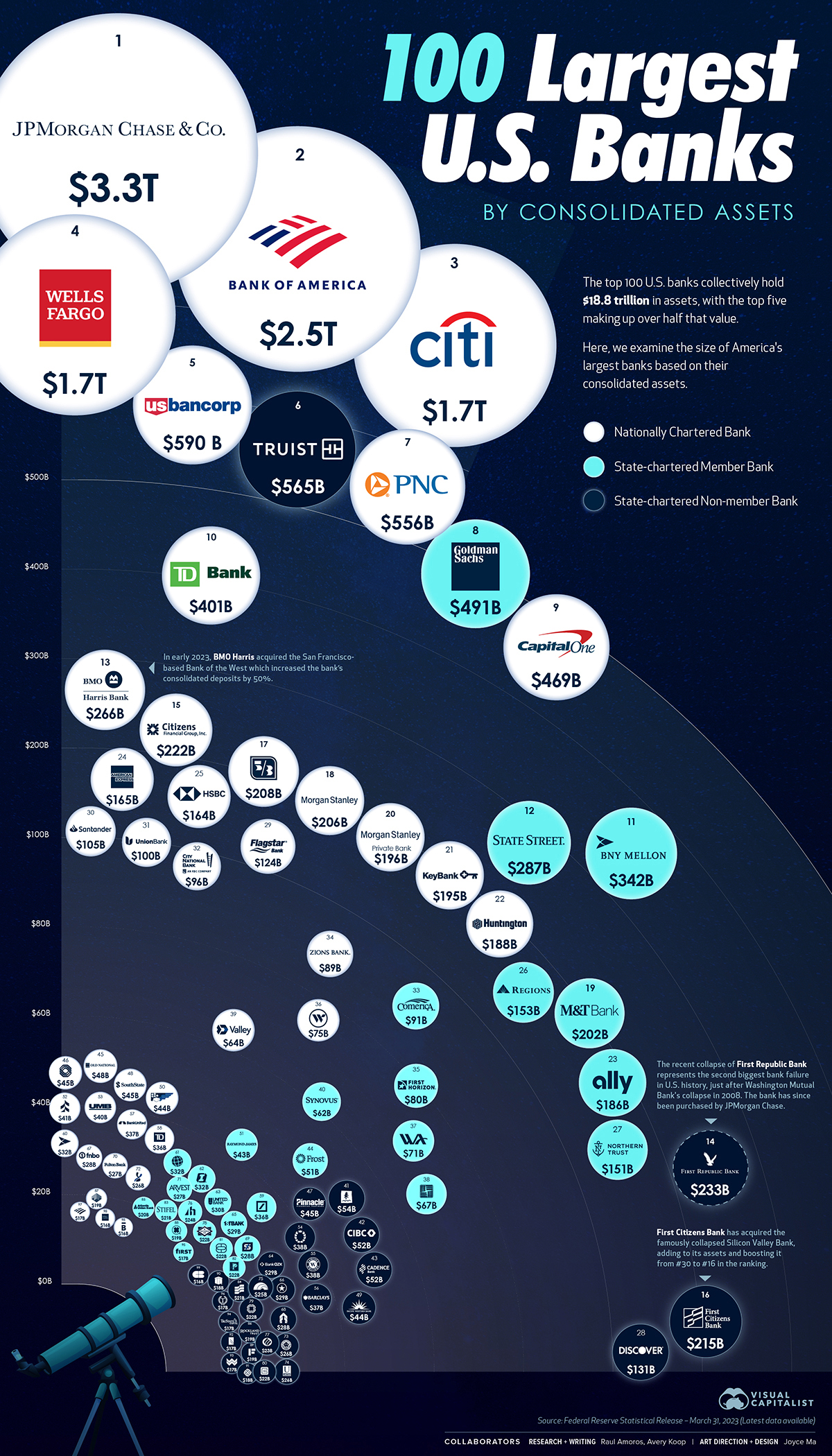

Commercial banks are the most common and recognizable type of banking institution. They offer a broad range of services to individuals, businesses, and government entities, including deposit accounts (checking, savings, CDs), loans (personal, auto, mortgage, business), credit cards, and treasury management services. They vary in size from global giants like JPMorgan Chase and Bank of America, which have a national and international footprint, to regional banks serving multiple states, and smaller community banks. These banks are typically for-profit entities, owned by shareholders.

Community Banks: Local Roots, Tailored Services

Community banks, often state-chartered, are generally smaller institutions that focus on serving local communities and businesses. They pride themselves on relationship-based banking, offering personalized services and making lending decisions based on local knowledge. While their physical footprint is smaller, they are crucial for providing financial access in rural areas and supporting local economic development. Their flexibility and understanding of local market dynamics can be a significant advantage for small businesses and individuals who prefer a more personal touch.

Credit Unions: Member-Owned Alternatives

Credit unions are non-profit financial cooperatives owned by their members. Instead of generating profits for shareholders, they aim to return profits to members in the form of lower loan rates, higher savings rates, and fewer fees. Membership is typically restricted to individuals who share a common bond (e.g., employees of a specific company, residents of a particular geographic area, or members of an association). Credit unions offer many of the same services as commercial banks but operate under a different philosophy, often emphasizing financial education and community involvement.

Investment Banks and Digital-Only Banks: Specialized and Modern Players

While not typically included in the “FDIC-insured bank” count, these entities are vital components of the broader financial ecosystem.

- Investment Banks: These institutions primarily deal with corporate finance, mergers and acquisitions, underwriting securities, and trading for institutional clients. They do not typically accept retail deposits.

- Digital-Only Banks (Neobanks): These are financial technology (FinTech) companies that operate entirely online, without physical branches. Many are not technically banks themselves but partner with existing FDIC-insured banks to offer deposit accounts, while providing their own user interfaces, budgeting tools, and other innovative services. They appeal to tech-savvy consumers seeking convenience, lower fees, and modern digital experiences.

Forces Shaping the Banking Landscape: Consolidation and Innovation

The trajectory of the banking sector in the U.S. has been largely defined by two powerful forces: relentless consolidation and rapid technological innovation. These trends are not only reducing the raw number of institutions but also fundamentally altering how banking services are delivered and accessed.

Mergers and Acquisitions: The Trend Towards Fewer, Larger Institutions

The steady decline in the number of banks from over 14,000 in the mid-1980s to fewer than 5,000 today is primarily due to mergers and acquisitions (M&A). Several factors drive this consolidation:

- Economies of Scale: Larger banks can spread fixed costs (like technology, compliance, and marketing) over a larger asset base, leading to greater efficiency and profitability.

- Increased Regulatory Burden: Post-financial crisis regulations (like Dodd-Frank) have increased compliance costs, making it harder for smaller institutions to compete without significant investment.

- Technological Demands: Investing in advanced digital platforms, cybersecurity, and data analytics is expensive, pushing smaller banks to merge to gain the necessary capital and expertise.

- Market Share and Diversification: Acquisitions allow banks to expand their geographic reach, acquire new customer segments, and diversify their product offerings.

While consolidation can lead to greater stability for the system as a whole and potentially more sophisticated services, it also raises concerns about reduced competition, potential lack of choice for consumers, and the “too big to fail” problem.

The Rise of Digital Banking and FinTech

The digital revolution has profoundly impacted banking. Consumers increasingly expect seamless online and mobile banking experiences, driving traditional banks to invest heavily in technology and giving rise to new digital-first players.

- Convenience: Online and mobile banking offer 24/7 access to accounts, bill pay, transfers, and loan applications, reducing the need for physical branches.

- Innovation: FinTech companies are unbundling traditional banking services, offering specialized solutions for payments, lending, budgeting, and investing, often with superior user experiences.

- Cost Efficiency: Digital channels are generally less expensive to operate than brick-and-mortar branches, allowing some institutions to offer lower fees or better rates.

This shift has prompted both traditional banks to digitalize and a new wave of challengers (neobanks and FinTechs) to emerge, changing the competitive dynamics of the industry.

Regulatory Changes and Their Impact on Bank Numbers

Regulatory frameworks are constantly evolving, often in response to economic crises or technological shifts.

- Deregulation/Re-regulation: Periods of deregulation (e.g., Glass-Steagall repeal) can spur consolidation, while periods of re-regulation (e.g., Dodd-Frank Act post-2008) can increase compliance costs, again favoring larger institutions or leading to smaller banks being acquired.

- Chartering Policies: The ease or difficulty of obtaining a new bank charter from the OCC or state regulators also influences the overall count. While new charters are granted, the pace has been slow compared to the rate of mergers.

These regulatory environments play a critical role in shaping the number and structure of financial institutions, ensuring stability while also influencing market entry and exit.

Why the Number Matters: Implications for Consumers and the Economy

The exact count of banks might seem like an abstract statistic, but its implications for individuals, businesses, and the overall economy are tangible and significant.

Competition and Consumer Choice

A healthy number of diverse financial institutions fosters competition. More competition typically translates into:

- Better Rates: Banks vie for deposits and loan customers, often leading to more attractive interest rates on savings and lower rates on loans.

- Lower Fees: Competitive pressure can force banks to reduce or eliminate various account fees.

- Improved Services: Institutions are incentivized to innovate and offer better customer service, more advanced digital tools, and a wider range of products tailored to different needs.

Conversely, excessive consolidation can lead to fewer choices, potentially higher fees, and less innovation, especially in niche markets or underserved communities.

Access to Capital and Economic Growth

Banks are crucial intermediaries in the economy, channeling savings into investments and loans. A robust and diverse banking system ensures that:

- Businesses have access to capital: Small and large businesses rely on banks for working capital, expansion loans, and lines of credit, which are vital for job creation and economic growth. Community banks, in particular, are often pillars of small business lending in their local markets.

- Individuals can fund major life events: Mortgages, auto loans, and student loans provided by banks enable individuals to purchase homes, vehicles, and education, contributing to personal wealth building and consumer spending.

A lack of banking options, especially in rural or low-income areas, can create “banking deserts,” hindering local economic development and perpetuating financial exclusion.

Financial Stability and Systemic Risk

While a greater number of banks might seem to imply less risk, the crucial factor is the quality and diversity of institutions. A system with many small, well-managed banks can be resilient, as the failure of one or two won’t cascade. However, a system dominated by a few “too big to fail” institutions carries systemic risk, where the failure of one could trigger a broader financial crisis. Regulators constantly balance the benefits of scale and efficiency against the risks of concentration and interconnectedness. The lessons from the 2008 financial crisis continue to inform policy debates around bank size and complexity.

Navigating Your Banking Choices in a Diverse Market

Given the dynamic and diverse nature of the American banking landscape, making informed choices about where to bank is more important than ever.

Identifying Your Financial Needs

Before choosing a bank or credit union, assess your personal financial needs and preferences:

- Transaction Volume: Do you frequently use ATMs or prefer digital transactions?

- Lending Needs: Are you planning to take out a mortgage, car loan, or small business loan soon?

- Savings Goals: Are you looking for high-yield savings accounts or investment products?

- Access Preferences: Do you value in-person branch service, or are you comfortable with an entirely digital experience?

- Values: Do you prefer to bank with institutions focused on local communities or those that align with specific social or environmental values (e.g., community development financial institutions)?

Weighing the Pros and Cons of Different Bank Types

- Large Commercial Banks: Pros include extensive branch networks, advanced digital tools, a wide range of products, and often competitive rates on certain products. Cons can include less personalized service, potentially higher fees, and a less direct connection to local communities.

- Community Banks: Pros include personalized service, local decision-making, relationship-based banking, and strong community ties. Cons might include fewer branches, less advanced digital offerings compared to large banks, and potentially less competitive rates on some products.

- Credit Unions: Pros include member-centric focus, often lower fees and better rates, and a strong community ethos. Cons can include membership eligibility requirements and sometimes a smaller branch network or less sophisticated technology.

- Digital-Only Banks: Pros include convenience, often lower fees, innovative budgeting tools, and excellent mobile experiences. Cons can include a lack of physical branches for cash deposits/withdrawals, less personal customer service, and reliance on technology.

The Future of Banking: Personalization and Digital Access

The future of banking in America will undoubtedly continue to be shaped by technology and consumer demands for convenience and personalization. While the number of traditional banks may continue to slowly decline due to consolidation, the access to banking services will likely expand through digital channels and innovative FinTech solutions. AI and data analytics will enable banks to offer more tailored products and advice, while cybersecurity will remain a paramount concern. For consumers and businesses, understanding this ever-changing landscape will be key to making strategic financial decisions and leveraging the best tools available for their specific needs. The question of “how many banks” serves as a starting point to explore a complex, vital, and continuously evolving sector that underpins the American economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.