The financial landscape of the United States is vast and intricate, underpinning the nation’s economic activity from individual savings to corporate financing. A fundamental question often arises: how many banks operate within this dynamic ecosystem? The answer, while seemingly straightforward, is complex, influenced by evolving definitions, regulatory classifications, and continuous market consolidation. Understanding the sheer number, variety, and distribution of these institutions offers critical insights into financial access, competition, and the overall health of the U.S. economy.

The Evolving Landscape of U.S. Banking

The concept of a “bank” itself has broadened considerably since the early days of state-chartered institutions. Today, the term encompasses a diverse array of financial entities, each playing a distinct role in serving consumers and businesses. To accurately assess the number of banks in the U.S., it’s crucial to first define what constitutes a banking institution within this modern context.

Defining a “Bank”: What Counts?

When people ask “how many banks,” they are typically referring to depository institutions that accept deposits and make loans. However, even within this broad definition, there are important distinctions:

- Commercial Banks: These are the most common type, offering a wide range of services to individuals, businesses, and government entities. They are typically insured by the Federal Deposit Insurance Corporation (FDIC) and can be nationally or state-chartered.

- Savings Institutions (Savings Banks and Thrifts): Historically focused on mortgages and consumer savings, these institutions have largely converged with commercial banks in terms of offerings and are also FDIC-insured. The line between a savings bank and a commercial bank has blurred significantly over the decades.

- Credit Unions: Member-owned financial cooperatives that provide similar services to banks but operate on a not-for-profit basis. They are insured by the National Credit Union Administration (NCUA). While technically distinct from banks due to their ownership structure and mission, they serve as crucial depository institutions for millions of Americans.

- Non-Bank Financial Companies (Fintechs, Shadow Banks): This category includes a growing number of entities that offer banking-like services (lending, payments, investment management) but are not chartered as traditional banks and may not accept insured deposits. While significant players in the financial system, they are generally not included in the traditional count of “banks.”

For the purpose of answering “how many banks,” the focus is usually on FDIC-insured commercial banks and savings institutions, along with NCUA-insured credit unions, as these represent the core regulated depository institutions.

Historical Trends: Consolidation and New Entrants

The U.S. banking industry has undergone profound transformations over the past century, particularly marked by significant consolidation. In the mid-1980s, there were over 14,000 FDIC-insured commercial banks and savings institutions. This number has steadily declined due to mergers, acquisitions, and bank failures, driven by deregulation, technological advancements, and the pursuit of economies of scale.

Despite this consolidation, the market remains dynamic. While fewer in number, the remaining institutions are often larger and more geographically diverse. Simultaneously, new charters, though less frequent than in the past, continue to emerge, often with specialized business models or digital-first approaches. This constant flux means the number is never static but rather a snapshot in time.

The Current Snapshot: Numbers and Nuances

As of recent data (early 2023/2024), the landscape of U.S. depository institutions provides a clearer picture of the current numbers. It’s important to remember that these figures are dynamic, changing daily due to mergers, new charters, and closures.

Commercial Banks and Savings Institutions (FDIC-Insured)

The primary data source for these institutions is the Federal Deposit Insurance Corporation (FDIC). According to their reports, the number of FDIC-insured commercial banks and savings institutions has stabilized somewhat in recent years after decades of decline, but the long-term trend of consolidation persists.

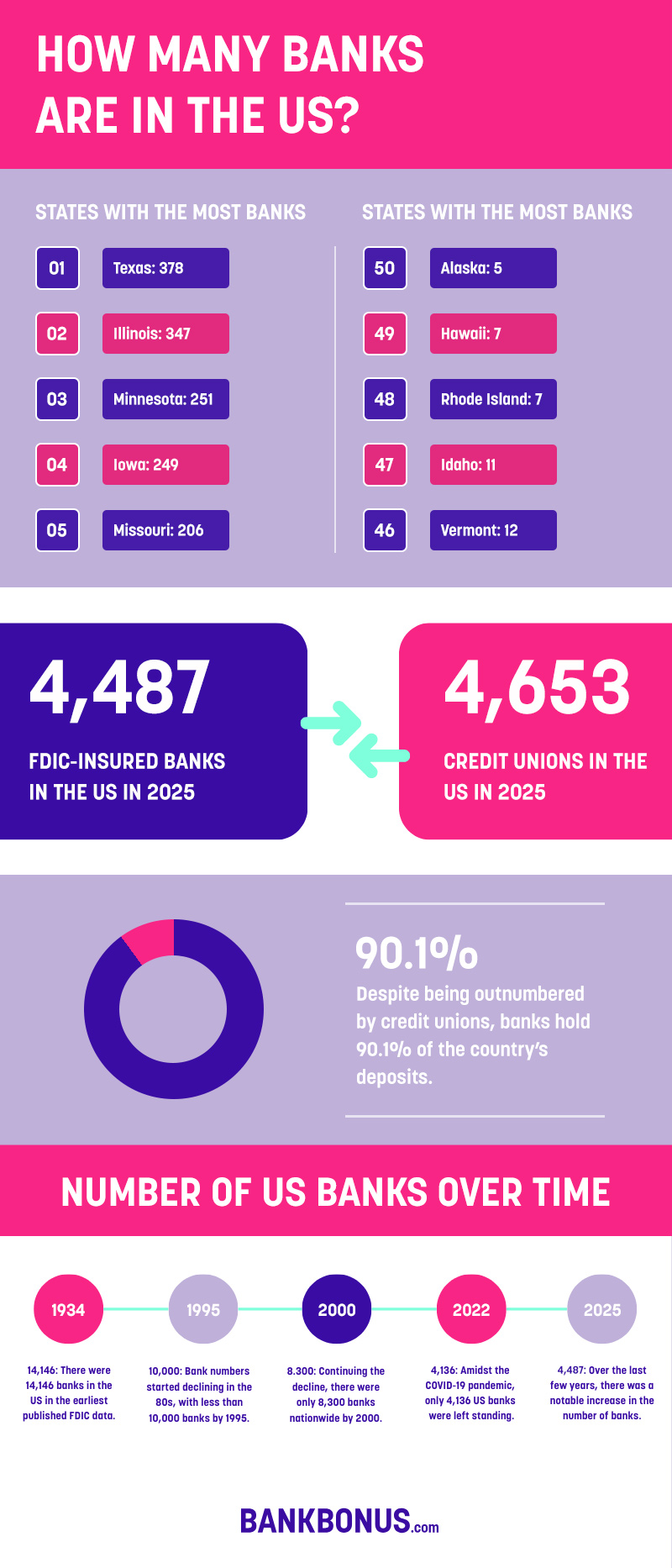

As of the latest available statistics (e.g., Q3 2023 or Q4 2023 for general reference), the number of FDIC-insured institutions typically hovers around 4,600 to 4,700. This figure includes both national and state-chartered banks, as well as a smaller number of savings institutions that are also FDIC-insured. This is a dramatic reduction from the peak in the 1980s but still represents a robust and diverse banking sector.

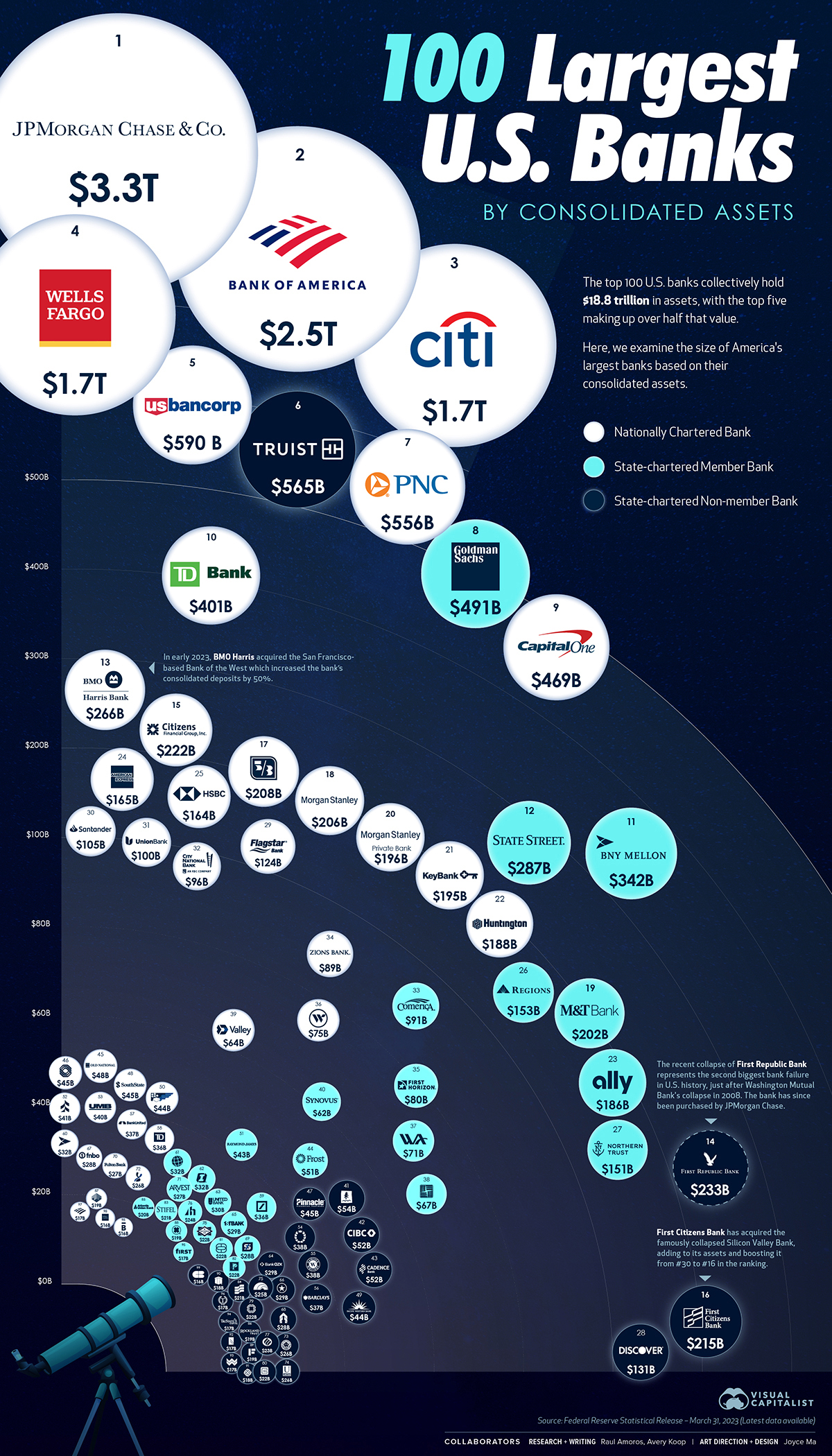

These institutions range from global giants like JPMorgan Chase and Bank of America, with trillions in assets and operations across the country and internationally, to thousands of small community banks serving specific local markets.

The Role of Credit Unions (NCUA-Insured)

Credit unions are another vital component of the U.S. financial system, providing banking services to their members. They are regulated and insured by the National Credit Union Administration (NCUA). Similar to banks, credit unions have also experienced a trend of consolidation, though often at a slower pace.

As of recent NCUA data (e.g., early 2023/2024), the number of federally insured credit unions is typically in the range of 4,500 to 4,700. This means that when combined with FDIC-insured institutions, the total number of traditional, regulated depository institutions in the U.S. is approximately 9,000 to 9,400.

Credit unions are distinct in their not-for-profit model and member ownership, often fostering strong community ties and a focus on member welfare rather than shareholder profits. They cater to a broad spectrum of consumers and small businesses, often filling niches that larger commercial banks might overlook.

The Shadow Banking System and Fintech’s Impact

While not typically counted in the “how many banks” tally, it’s crucial to acknowledge the growing influence of non-bank financial companies and fintechs. These entities offer services like online lending, payment processing, investment platforms, and even digital checking accounts, often partnering with traditional banks or operating under different regulatory frameworks. They expand access to financial services and inject significant competition, fundamentally altering the competitive landscape even if they don’t add to the count of chartered banks.

Why the Number Matters: Economic Impact and Financial Stability

The total number and distribution of banking institutions are not mere statistics; they have profound implications for economic health, consumer welfare, and financial stability. A healthy banking sector, characterized by an appropriate balance of large, medium, and small institutions, is essential for a thriving economy.

Competition and Consumer Choice

A diverse banking sector with a significant number of players fosters competition. This competition benefits consumers and businesses through:

- Better Rates and Fees: Banks compete for deposits and loans, leading to more favorable interest rates on savings and borrowing, and lower service fees.

- Innovative Products and Services: Competition drives institutions to develop new and improved financial products, from advanced online banking platforms to specialized loan offerings.

- Improved Customer Service: To retain and attract customers, banks strive to offer superior service and personalized attention.

Conversely, a highly concentrated banking sector with too few players could lead to reduced choice, higher costs, and less innovation.

Access to Capital for Businesses

Banks are critical intermediaries for channeling capital from savers to borrowers. A robust network of banks ensures that businesses, particularly small and medium-sized enterprises (SMEs), have access to the credit they need to grow, invest, and create jobs. Community banks, in particular, often specialize in relationship-based lending to local businesses, playing a disproportionately large role in local economic development despite their smaller asset size. A decline in the number of these institutions can sometimes lead to credit gaps in certain communities or for specific business types.

Systemic Risk and Regulation

The number and interconnectedness of banks also bear on financial stability. A system with many smaller, independent banks might be perceived as less prone to systemic risk—the risk that the failure of one institution could trigger a cascade of failures across the entire financial system. However, consolidation can also lead to stronger, more diversified institutions that are better equipped to withstand economic shocks. Regulators, primarily the FDIC, Federal Reserve, and OCC (Office of the Comptroller of the Currency), constantly monitor the health of these institutions, ensuring adequate capital, liquidity, and risk management practices to safeguard the financial system regardless of the number of players.

Key Drivers of Change in the Banking Sector

The number of banks in the U.S. is not static; it’s a dynamic figure constantly influenced by a confluence of economic, technological, and regulatory factors. Understanding these drivers is crucial for grasping the trajectory of the banking industry.

Mergers and Acquisitions: The Consolidation Trend

The most significant factor influencing the decline in the number of banks has been a persistent wave of mergers and acquisitions (M&A). Banks acquire smaller institutions to expand market share, achieve economies of scale, reduce overhead, and diversify their services or geographic reach. Regulatory changes, such as the lifting of interstate banking restrictions, further fueled this trend, allowing larger banks to operate across state lines and acquire local competitors. While this leads to fewer individual charters, it often results in stronger, more resilient institutions.

Regulatory Environment and Compliance Costs

The regulatory burden on banks has increased significantly, particularly since the 2008 financial crisis with the passage of the Dodd-Frank Act. Compliance with complex rules regarding capital requirements, consumer protection, anti-money laundering, and data privacy requires substantial investment in technology, personnel, and expertise. For smaller community banks, these compliance costs can be disproportionately high, making it challenging to compete and sometimes prompting them to sell to larger entities that can better absorb these expenses. This regulatory pressure can act as a barrier to entry for new banks and a catalyst for consolidation among existing ones.

Technological Disruption and Digital Banking

The rapid pace of technological innovation has profoundly impacted the banking sector. Digital banking platforms, mobile apps, and artificial intelligence are changing how customers interact with their money and how banks operate. Investing in cutting-edge technology is essential to remain competitive, but it requires significant capital outlays. This pressure favors larger banks with deeper pockets or nimble fintechs built on modern tech stacks. Existing traditional banks that fail to adapt risk losing customers to more digitally advanced competitors, either other traditional banks or non-bank fintech providers.

Economic Cycles and Market Forces

Economic downturns can place immense stress on banks, leading to increased loan defaults and reduced profitability. During such periods, weaker institutions may fail or be forced into mergers, contributing to a decline in the overall number. Conversely, periods of strong economic growth can foster an environment where new banks emerge, capitalizing on unmet market needs or new business models. Interest rate environments, inflation, and unemployment rates all play a role in the profitability and stability of banks, influencing their survival and growth prospects.

Looking Ahead: The Future of Banking in the U.S.

The U.S. banking sector is continuously evolving, shaped by an intricate dance between tradition and innovation. While the number of distinct banking charters has decreased significantly over decades, the diversity and robustness of financial services remain paramount.

The Rise of Niche and Community Banks

Despite the overarching trend of consolidation, there is a persistent demand for localized and specialized financial services. This has led to the emergence of “de novo” banks (newly chartered institutions), often with a focus on specific communities, underserved demographics, or niche industries. Many of these new entrants leverage technology to offer a more personalized and efficient service model, differentiating themselves from the largest national banks. Community banks, in particular, are finding renewed relevance by emphasizing relationship-based banking and deep local market knowledge.

Digital-First Institutions and Challenger Banks

The future will undoubtedly see a continued expansion of digital-first banks, often referred to as “challenger banks” or “neobanks.” While many operate by partnering with existing chartered banks (meaning they don’t add to the official count of charters), some are successfully obtaining their own bank charters. These institutions typically offer streamlined, mobile-centric experiences, lower fees, and innovative features, appealing especially to tech-savvy consumers and those underserved by traditional banking models. Their growth forces traditional banks to accelerate their digital transformations, contributing to a more technologically advanced banking ecosystem.

The Enduring Role of Traditional Banks

Despite the rise of digital competitors and the ongoing consolidation, traditional commercial banks and credit unions will remain the bedrock of the U.S. financial system. Their comprehensive range of services, extensive branch networks (even if diminishing), trusted brands, and deep regulatory experience provide a sense of security and accessibility for millions of Americans and businesses. The future will likely see a hybrid model, where traditional banks integrate more advanced technology and digital service offerings while maintaining their foundational roles in capital allocation, risk management, and consumer protection. The exact number of institutions may continue to fluctuate, but the core functions of banking will endure, adapting to meet the financial needs of a changing economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.