The question “how many banks are there in the U.S.?” seems simple enough to answer with a single number. Yet, delving into this question reveals a dynamic, complex, and crucial aspect of the American financial landscape. The exact figure is not static; it fluctuates quarterly, reflects decades of economic evolution, and encompasses a diverse range of institutions far beyond the traditional image of a brick-and-mortar branch. Understanding this number, and the trends behind it, offers profound insights into the health of the U.S. economy, the competitive environment for financial services, and the choices available to consumers and businesses alike.

At its core, the U.S. banking system is designed for stability and robust financial intermediation, ensuring the flow of capital and facilitating countless transactions daily. While the sheer number of distinct chartered banks has significantly decreased over the past few decades due to various economic and regulatory forces, the system remains incredibly diverse and innovative. From global megabanks to hyper-local community banks, and the burgeoning sector of credit unions and online-only institutions, the ecosystem serves a nation of over 330 million people and a multi-trillion-dollar economy. This exploration will move beyond a mere tally, providing a professional, insightful, and engaging look at the forces shaping the U.S. banking sector and what it means for everyone.

The Dynamic Landscape of U.S. Banking: More Than Just Numbers

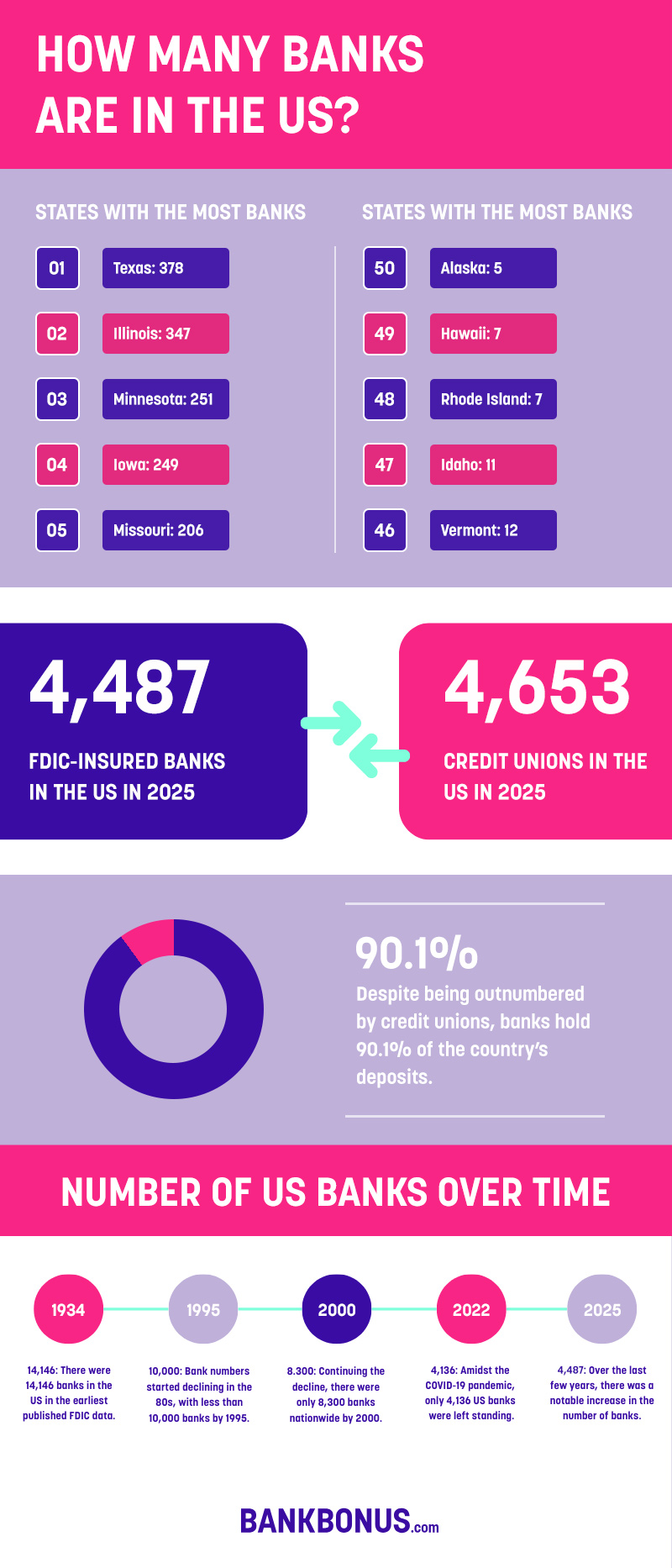

The immediate answer to “how many banks in the U.S.?” typically hovers around 4,000 to 4,500 FDIC-insured commercial banks and savings institutions at any given time, as reported by the Federal Deposit Insurance Corporation (FDIC). However, this number is a snapshot of a constantly evolving system and doesn’t tell the whole story. The U.S. banking sector is not a static entity but a living organism, adapting to technological advancements, regulatory changes, market demands, and global economic shifts. The significance of this number extends far beyond simple statistics; it directly impacts financial stability, consumer choice, business lending, and the overall competitiveness of the U economy.

The trajectory of the number of U.S. banks has been one of significant consolidation over the last 40 years. In the mid-1980s, the U.S. boasted over 14,000 banks. This dramatic reduction is a testament to sweeping changes in regulations, the pursuit of economies of scale, technological disruption, and periods of economic stress. While fewer in number, the remaining institutions often operate with greater scale, efficiency, and a broader array of services. This consolidation has led to a banking environment where larger institutions hold a significant portion of assets, yet a vibrant network of smaller, community-focused banks continues to play a vital role in local economies. Understanding this duality is key to grasping the true nature of U.S. banking today.

The Official Tally: FDIC-Insured Institutions

The most authoritative source for the number of U.S. banks is the Federal Deposit Insurance Corporation (FDIC). The FDIC insures deposits in U.S. banks and savings associations, guaranteeing up to $250,000 per depositor, per insured bank, for each account ownership category. This insurance is a cornerstone of public confidence in the banking system. The FDIC publishes quarterly data on the number of insured institutions, total assets, and other key financial metrics. As of the most recent data available (e.g., Q3 2023 or Q4 2023 reports), the figure typically floats in the range of 4,100 to 4,500. It’s important to note that this number specifically refers to commercial banks and savings institutions that are FDIC-insured, excluding credit unions, which have their own regulatory body and insurance fund. The number is constantly updated due to mergers, acquisitions, failures, and the rare creation of new banks.

A Historical Perspective: Decades of Consolidation

To truly appreciate the current number of banks, one must look at the historical context. The U.S. banking industry has undergone profound transformation. In 1985, there were approximately 14,400 FDIC-insured commercial banks in the U.S. The decline from that peak to today’s figures represents a sustained period of consolidation driven by several factors. Deregulation, particularly the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994, facilitated interstate banking and spurred a wave of mergers and acquisitions. Economic crises, such as the Savings and Loan crisis of the late 1980s and the 2008 financial crisis, also led to numerous bank failures and subsequent consolidation. Furthermore, the pursuit of economies of scale, the increasing cost of regulatory compliance, and the need for significant investments in technology have made it challenging for smaller institutions to compete, often leading them to merge with larger entities. While consolidation reduces the sheer number of banks, it often results in larger, more diversified institutions that can offer a broader range of services and potentially greater stability.

Expanding the Definition: Types of Financial Institutions

When we ask “how many banks,” our mental image often defaults to a commercial bank. However, the U.S. financial landscape is much richer and more diverse, comprising various types of institutions that serve different purposes and operate under distinct regulatory frameworks. Understanding these distinctions is crucial for a comprehensive grasp of the financial ecosystem and for making informed decisions about where to place your money or seek financial services. Beyond commercial banks, credit unions, online-only banks, and neo-banks have emerged as significant players, each contributing to the competitive dynamics and offering unique value propositions.

These different types of institutions cater to a wide spectrum of needs, from basic checking and savings accounts to complex commercial lending and investment services. The rise of digital platforms has further blurred some traditional lines, creating new avenues for financial services delivery and prompting consumers to consider factors beyond just physical proximity when choosing a financial partner. This expanded view highlights the true breadth of options available within the U.S. financial system, emphasizing that “banking” today is far more multifaceted than it once was.

Commercial Banks and Savings Institutions

These are the traditional institutions most people recognize as “banks.” Commercial banks are typically chartered by either state or federal governments (the Office of the Comptroller of the Currency, OCC, for national banks). Their primary functions include accepting deposits, making loans (consumer, commercial, mortgage), providing checking and savings accounts, and offering various other financial services like credit cards, wealth management, and treasury services. Savings institutions, historically focused on mortgage lending and savings deposits, have largely evolved to offer similar services to commercial banks. Both are critical pillars of the financial system, providing liquidity, facilitating transactions, and extending credit that fuels economic activity. They operate under a robust regulatory framework designed to ensure their stability and protect depositors.

The Rise of Credit Unions

Credit unions represent a distinct and increasingly important segment of the U.S. financial services industry. Unlike banks, which are typically for-profit entities owned by shareholders, credit unions are not-for-profit cooperative organizations owned by their members. Their primary mission is to serve their members, often translating to lower fees, better interest rates on deposits, and more competitive loan rates compared to traditional banks. Credit unions are regulated by the National Credit Union Administration (NCUA), which also insures deposits up to $250,000 per member, per account ownership category, through the National Credit Union Share Insurance Fund (NCUSIF). The number of credit unions has also seen consolidation, but their market share and asset base have grown significantly, making them a formidable alternative for consumers seeking a member-centric banking experience.

Emerging Players: Online Banks and Neobanks

The digital revolution has given rise to new categories of financial service providers. Online banks are fully chartered and FDIC-insured institutions that operate entirely without physical branches. They leverage technology to offer competitive rates and often lower fees due to reduced overhead costs. Examples include Ally Bank or Discover Bank. Neobanks, on the other hand, are typically financial technology (fintech) companies that offer banking-like services through mobile apps and digital platforms, often partnering with a traditional, FDIC-insured bank to hold deposits. While they provide an innovative user experience and advanced digital tools, they do not hold their own banking charters. Companies like Chime or Revolut fall into this category. Both online banks and neobanks are disrupting traditional banking models, driving innovation, and appealing to a tech-savvy customer base that values convenience, speed, and digital-first solutions. Their increasing popularity reflects a broader shift in consumer preferences towards digital financial management.

The Economic Impact and Regulatory Framework of U.S. Banks

The presence and characteristics of U.S. banks are not merely statistical points but fundamental determinants of the nation’s economic health and stability. These institutions are the lifeblood of commerce, facilitating everything from daily consumer transactions to large-scale infrastructure projects. Their collective actions and the framework within which they operate significantly influence economic growth, employment, and financial market integrity. The question of “how many banks” is thus inextricably linked to discussions about competition, innovation, and the effectiveness of financial regulation in balancing growth with stability.

A robust and well-regulated banking sector is essential for a thriving modern economy. It ensures that capital is efficiently allocated, risks are managed appropriately, and consumers and businesses have access to the financial tools they need to prosper. The U.S. system, with its mix of large national institutions and smaller community-focused entities, alongside the growth of credit unions and digital innovators, represents a complex but generally resilient structure designed to serve diverse needs across a vast and varied geography. Understanding the roles these institutions play and the oversight they receive provides deeper insight into their profound economic impact.

Facilitating Economic Growth

Banks are crucial intermediaries in the economy. They collect deposits from savers and lend these funds to borrowers, facilitating investment in businesses, real estate, and consumer goods. This process, known as financial intermediation, is vital for economic growth. By providing capital, banks enable companies to expand, innovate, and create jobs. They also offer payment systems (checking, credit cards, wire transfers) that are indispensable for commercial transactions, ensuring the smooth flow of goods and services. Beyond lending, banks provide essential services like treasury management for corporations, foreign exchange, and investment banking, all of which support complex economic activities and global trade. Without a functioning banking system, economic activity would grind to a halt, underscoring their critical role in the prosperity and stability of the nation.

Competition, Innovation, and Consumer Choice

The number and types of financial institutions directly influence competition and innovation within the banking sector. While consolidation has reduced the absolute number of banks, the rise of credit unions, online banks, and neobanks has introduced new forms of competition. This competitive pressure encourages banks to innovate, offering better products, services, and technologies to attract and retain customers. Consumers benefit from this environment through lower fees, higher interest rates on savings, more convenient digital tools, and a wider array of specialized financial products tailored to specific needs. For instance, the demand for mobile banking and user-friendly apps has been significantly driven by this competition. The existence of a diverse range of institutions ensures that both individuals and businesses have choices, allowing them to select a financial partner that best aligns with their values, service preferences, and financial goals, whether that’s a relationship-focused community bank or a technologically advanced online platform.

Regulatory Oversight and Financial Stability

The U.S. banking system operates under a multi-layered regulatory framework designed to ensure its safety and soundness, protect consumers, and prevent systemic risks. Key federal regulators include the Federal Reserve (which oversees bank holding companies and state-chartered member banks), the Office of the Comptroller of the Currency (OCC, for national banks), the Federal Deposit Insurance Corporation (FDIC, for deposit insurance and oversight of insured institutions), and the Consumer Financial Protection Bureau (CFPB, for consumer protection). Credit unions are regulated by the National Credit Union Administration (NCUA). This robust oversight aims to maintain financial stability by setting capital requirements, conducting examinations, enforcing compliance with consumer protection laws, and intervening when institutions face distress. The balance between allowing market forces to drive efficiency and imposing regulations to mitigate risks is a constant challenge, but it is critical for maintaining public trust and the overall health of the financial system.

Navigating Your Banking Choices: What Consumers Need to Know

Given the dynamic nature and diverse landscape of the U.S. banking system, understanding how many banks there are, and what types exist, ultimately empowers consumers to make informed choices. The “right” financial institution isn’t a one-size-fits-all answer; it depends on individual needs, preferences, and financial goals. Whether you prioritize low fees, high interest rates, personalized customer service, extensive branch networks, or cutting-edge digital tools, the varied ecosystem ensures that options are available. This segment provides practical guidance for navigating the choices and considers the future trajectory of the banking sector, highlighting trends that will continue to shape how we manage our money.

The decision of where to bank is a significant one, impacting daily financial management, long-term savings, and access to credit. By being aware of the different players, their strengths, and their limitations, consumers can proactively seek out institutions that best serve their financial well-being. Furthermore, staying attuned to the evolving landscape, especially the shift towards digital banking and the potential for continued consolidation, allows individuals to anticipate changes and adapt their financial strategies accordingly.

Choosing the Right Institution for Your Needs

Selecting a financial institution should be a deliberate process. Consider the following factors:

- Fees and Rates: Compare monthly maintenance fees, ATM fees, overdraft fees, and foreign transaction fees. Look at interest rates offered on savings accounts, money market accounts, and CDs, as well as loan rates for mortgages, auto loans, and personal loans.

- Customer Service: Do you prefer in-person interactions, or are you comfortable with phone and online support? Evaluate the responsiveness and availability of customer service channels.

- Branch Access vs. Digital Tools: If you value physical branches for transactions or personalized advice, a traditional bank or credit union with a strong local presence might be best. If you primarily bank online and use mobile apps, an online-only bank or neobank could offer superior digital experiences and competitive rates.

- Product Offerings: Does the institution offer all the services you need, such as checking, savings, credit cards, loans, investment services, and wealth management? Some institutions specialize in certain areas.

- Insurance: Always ensure your deposits are insured. For banks, this is FDIC insurance; for credit unions, it’s NCUA insurance, both up to $250,000 per depositor, per ownership category.

Careful consideration of these elements will lead to a choice that aligns with your lifestyle and financial aspirations.

The Future of Banking: Digital Transformation and Consolidation

The U.S. banking sector is constantly evolving, with significant trends pointing towards continued digital transformation and potential further consolidation. We can expect an acceleration of:

- Digital-First Experiences: Banks will continue to invest heavily in mobile banking apps, online platforms, and innovative digital tools, making banking more convenient and accessible. Artificial intelligence and machine learning will play increasingly larger roles in customer service, fraud detection, and personalized financial advice.

- Open Banking and APIs: The integration of financial services through APIs (Application Programming Interfaces) will allow for more seamless connections between different financial apps and services, offering consumers greater control over their financial data and more integrated financial management.

- Targeted Offerings: As technology allows for more granular data analysis, institutions will likely offer highly personalized products and services, catering to specific demographic groups or financial needs.

- Continued Consolidation: While the pace might slow, the pressures of regulatory compliance, technology investment, and competitive intensity suggest that some level of consolidation among traditional banks may continue. However, this will be balanced by the emergence of new fintech players and niche banking services.

These trends signify a future where banking is even more integrated into daily life, driven by data, and delivered through sophisticated digital channels, offering both challenges and unprecedented opportunities for consumers to manage their money effectively.

In conclusion, the question “how many banks are there in the U.S.?” unlocks a fascinating narrative of an industry in constant flux. While the number of traditional chartered banks has consolidated significantly over the decades, the broader financial services landscape has diversified immensely. Today, U.S. consumers and businesses benefit from a resilient, competitive, and innovative system comprising thousands of FDIC-insured banks, a robust network of NCUA-insured credit unions, and a rapidly expanding cohort of online banks and neobanks. This diverse ecosystem, underpinned by robust regulatory oversight, continues to be a cornerstone of the nation’s economic strength, offering a wealth of choices for every financial need and preference.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.