Social Security is a cornerstone of financial security for millions of Americans, providing a vital safety net in retirement, for those with disabilities, and for survivors. Understanding how your Social Security benefit is calculated is crucial for effective financial planning. It’s not simply a matter of multiplying your years of work by a fixed percentage. Instead, the Social Security Administration (SSA) employs a complex, yet transparent, formula designed to reflect your lifetime earnings and ensure fairness across generations. This article will demystify the process, breaking down the key components that determine your future benefit.

The Foundation: Your Lifetime Earnings Record

The most fundamental element in calculating your Social Security benefit is your earnings history. The SSA tracks your earnings each year up to a certain limit, which is subject to an annual cost-of-living adjustment. This means that not all of your income is subject to Social Security taxes, and consequently, not all of it will factor into your benefit calculation.

Tracking Your Earnings

From the moment you start working and paying Social Security taxes, the SSA creates and maintains a record of your earnings. This record is updated annually, typically by the following year. It’s essential to review your earnings record periodically to ensure accuracy. You can do this by creating an account on the Social Security Administration’s website (ssa.gov) and accessing your “Social Security Statement.” This statement provides a detailed history of your reported earnings and an estimate of your future retirement benefits at different ages.

The Average Indexed Monthly Earnings (AIME)

The SSA doesn’t use your raw earnings directly. Instead, it first “indexes” your earnings. Indexing adjusts your past earnings to reflect changes in general wage levels in the economy over time. This process ensures that earnings from earlier in your career are brought up to a more comparable value with your more recent earnings. For example, $10,000 earned in 1980 would be adjusted to a significantly higher figure today to reflect the increase in average wages since then. This indexing is critical because it prevents your benefit calculation from unfairly penalizing earnings from decades ago.

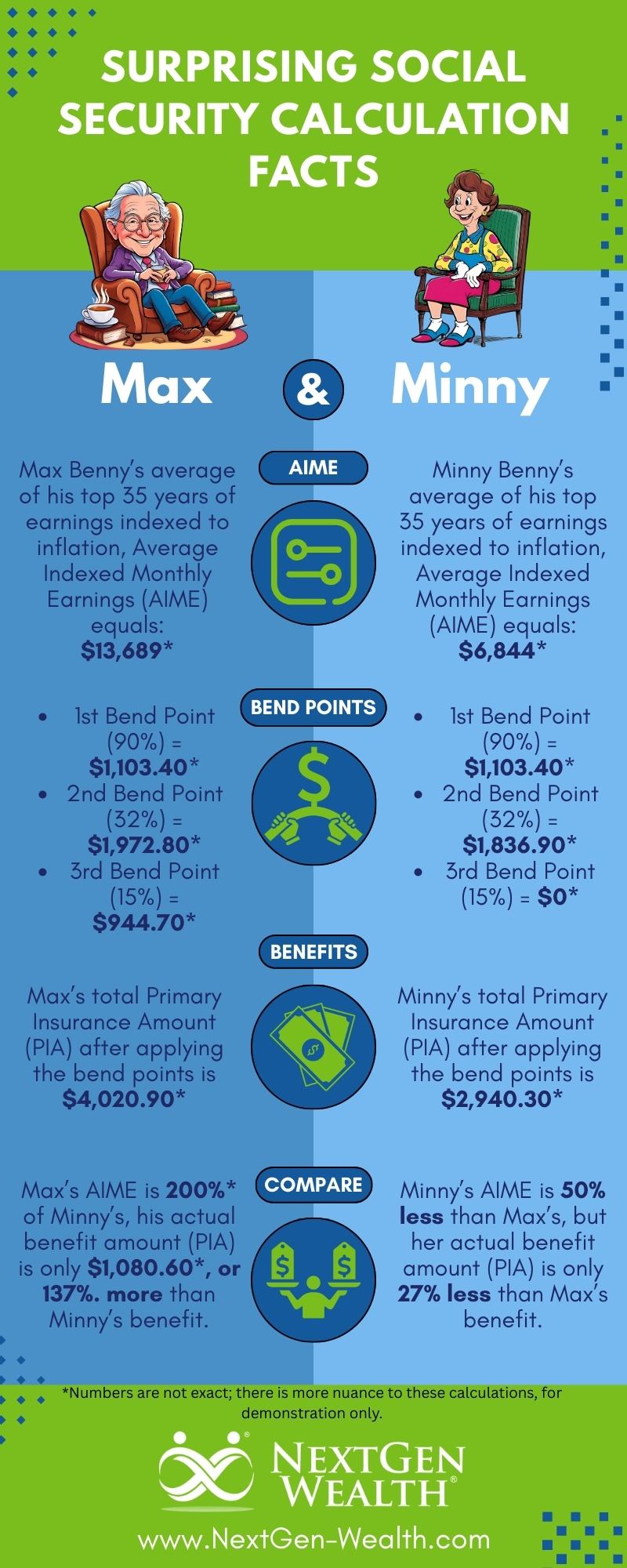

After indexing, the SSA identifies your highest 35 years of earnings. If you have fewer than 35 years of earnings, years with zero earnings will be included, which will lower your average. These 35 years of indexed earnings are then summed and divided by 420 (the number of months in 35 years) to arrive at your Average Indexed Monthly Earnings, or AIME. Your AIME represents your average monthly earnings over your working life, adjusted for inflation and wage growth.

The Calculation: Bringing AIME to Your Benefit

Once your AIME is established, the SSA applies a progressive formula to convert this average into your actual retirement benefit. This formula uses “bend points” that are adjusted annually. These bend points are designed to provide a higher replacement rate of your pre-retirement earnings for lower-income workers and a lower replacement rate for higher-income workers.

Understanding the Benefit Formula

The Social Security benefit formula has three “bend points.” The first bend point applies to the initial portion of your AIME, the second bend point applies to the next segment, and the third bend point applies to the remainder. The SSA uses specific percentages (which change slightly each year) to calculate the primary insurance amount (PIA), which is the benefit you would receive if you claim Social Security at your full retirement age.

For example, let’s consider a simplified, hypothetical scenario. Suppose the current bend points and percentages result in a formula where the SSA calculates 90% of the first portion of your AIME, 32% of the middle portion, and 15% of the amount above the third bend point. The sum of these calculated amounts equals your PIA. This means that a larger portion of a lower AIME is replaced by Social Security than a larger portion of a higher AIME. This progressive nature is a key feature of the Social Security system, aimed at providing a more substantial safety net for those who earned less throughout their careers.

The Impact of Claiming Age

Your PIA is the benefit you are entitled to at your “full retirement age.” However, you have the flexibility to claim Social Security benefits as early as age 62 or as late as age 70. Your choice of claiming age significantly impacts your monthly benefit amount.

Early Retirement: Reduced Benefits

If you choose to claim Social Security retirement benefits before your full retirement age (which varies based on your birth year, ranging from 66 to 67), your monthly benefit will be permanently reduced. For each month you claim before your full retirement age, your benefit is reduced by a fraction of a percent. This reduction is substantial. For instance, claiming at age 62 when your full retirement age is 67 means you will receive approximately 30% less per month for the rest of your life compared to claiming at your full retirement age.

Delayed Retirement: Increased Benefits

Conversely, if you postpone claiming Social Security benefits beyond your full retirement age, you will earn delayed retirement credits. These credits increase your monthly benefit by a certain percentage for each month you delay, up to age 70. For those who reach their full retirement age and continue working, delaying can lead to a significantly higher monthly payout. The SSA caps these increases at age 70, so there is no financial advantage to waiting longer to claim.

Additional Factors Influencing Your Benefit

While your earnings record and claiming age are the primary drivers of your Social Security benefit, several other factors can influence the amount you receive.

Spousal and Survivor Benefits

Social Security isn’t solely about individual earnings. The system also provides benefits for spouses and survivors.

Spousal Benefits

If you are married, your spouse may be eligible for a spousal benefit based on your earnings record, even if they never worked themselves or earned less than you. A spouse can receive up to 50% of the primary worker’s benefit if they claim at their full retirement age. However, if they claim spousal benefits before their full retirement age, those benefits will be reduced, similar to early retirement benefits.

Survivor Benefits

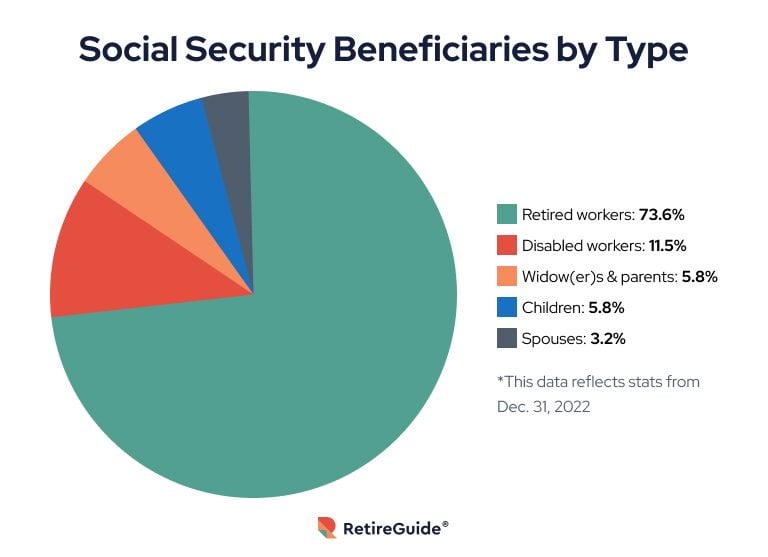

In the event of a worker’s death, their surviving spouse, children, and in some cases, dependent parents may be eligible for survivor benefits. The amount of the survivor benefit depends on the deceased worker’s earnings record and the age and relationship of the survivor. For example, a widow or widower claiming survivor benefits at their full retirement age can receive 100% of the deceased worker’s benefit. Younger widows or widowers may receive a reduced benefit.

Disability Benefits

Social Security also provides disability benefits to individuals who are unable to work due to a medical condition expected to last at least one year or result in death. The calculation for disability benefits is similar to retirement benefits, using your AIME. However, the criteria for eligibility are strictly medical, requiring a documented inability to perform substantial gainful activity.

Government Pension Offset (GPO) and Windfall Elimination Provision (WEP)

These provisions can affect individuals who also receive a pension from work that was not covered by Social Security (e.g., some federal, state, or local government jobs). The GPO and WEP are designed to prevent “double-dipping” and can reduce your Social Security benefit. Understanding if these provisions apply to you is important for accurate benefit estimation.

Planning for Your Social Security Future

The Social Security Administration’s calculation method, while intricate, is designed to be fair and sustainable. By understanding the core principles – your lifetime earnings, the indexing process, the progressive benefit formula, and the impact of your claiming age – you can make informed decisions about your retirement and financial future.

Regularly Reviewing Your Earnings Record

As mentioned, it is crucial to periodically check your Social Security earnings record. Errors can occur, and the sooner you identify and correct them, the better. The SSA provides clear instructions on its website for how to report discrepancies.

Using Online Tools and Resources

The Social Security Administration’s website (ssa.gov) is an invaluable resource. It offers a wealth of information, calculators, and the ability to create a personalized account to view your earnings history and benefit estimates. Online retirement planning tools from financial institutions can also help you integrate your expected Social Security benefits into a broader retirement savings strategy.

Consulting a Financial Advisor

For personalized guidance, especially if your financial situation is complex or you have questions about the GPO or WEP, consulting with a qualified financial advisor can be highly beneficial. They can help you understand how your Social Security benefits fit into your overall financial plan and optimize your claiming strategy.

By taking the time to understand “how Social Security is figured,” you empower yourself to make sound financial decisions that can lead to a more secure and comfortable retirement. It’s an investment in your future that pays dividends throughout your life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.