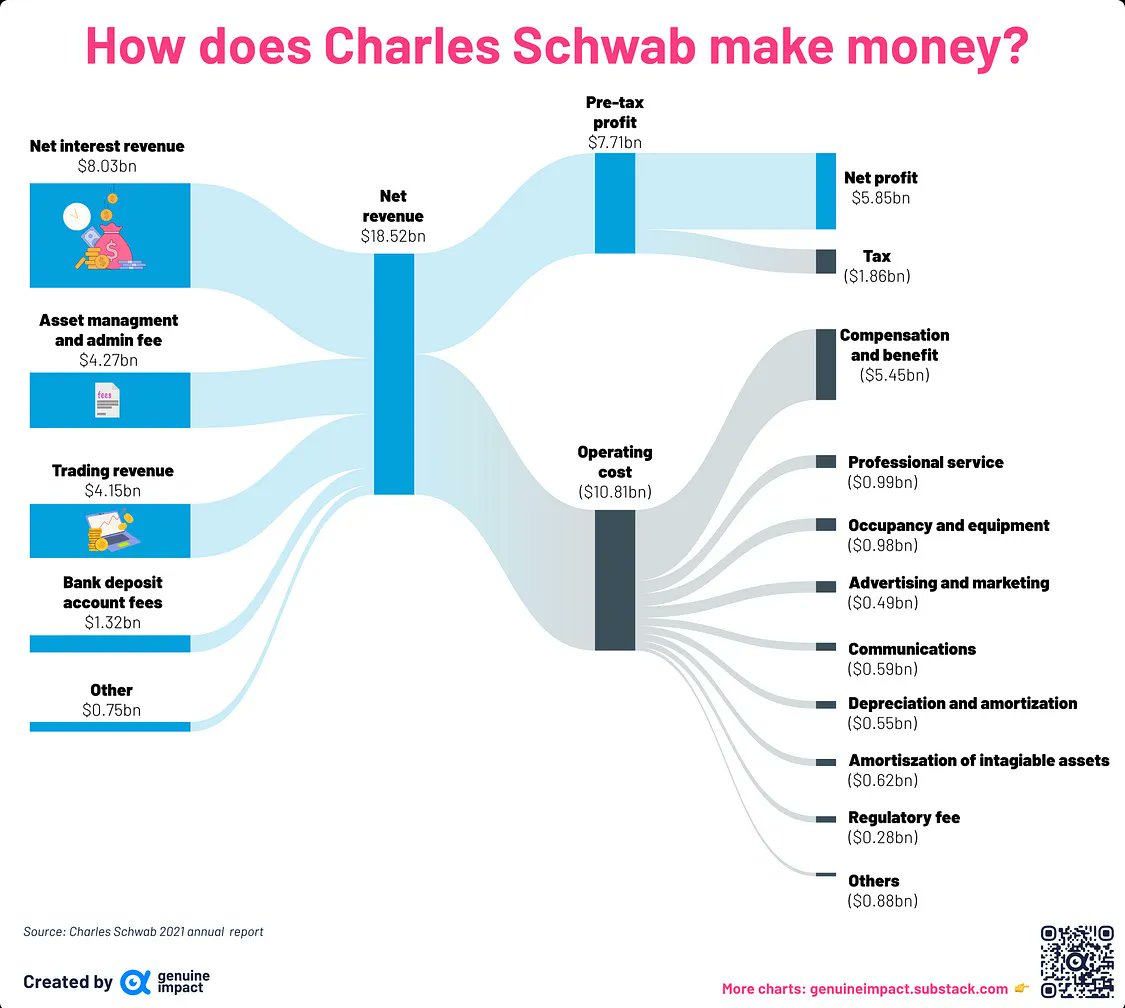

Charles Schwab, a name synonymous with investing and personal finance, stands as a titan in the brokerage industry. Founded in 1971 on principles of accessibility and transparency, it has grown from a discount broker to a comprehensive financial services powerhouse, managing trillions in client assets. For many, Schwab is where they open a brokerage account, plan for retirement, or seek financial advice. But beneath the veneer of low-cost investing and client-centric services, lies a sophisticated and diversified business model that generates substantial revenue. Understanding how Charles Schwab makes money isn’t just an exercise in financial curiosity; it offers insights into the intricacies of the modern financial services industry, particularly in an era of commission-free trading.

Schwab’s revenue generation is not reliant on a single stream but a complex interplay of interest income, asset management fees, trading-related revenues, and various ancillary services. This multi-faceted approach has allowed the company to not only adapt to significant industry shifts, such as the elimination of trading commissions, but also to thrive and expand its market share. This article will delve into the primary mechanisms through which Charles Schwab generates its impressive profits, shedding light on the strategies that underpin its financial success.

The Foundation of Profit: Net Interest Revenue

At the core of Charles Schwab’s profitability lies its vast client asset base, much of which is held in cash awaiting investment or simply as part of their liquid holdings. This cash, though seemingly idle, is a powerful engine for Schwab’s earnings through net interest revenue. This is arguably the most significant component of their income, often accounting for more than half of their total net revenue.

Cash Sweep Programs

When clients deposit funds into their Schwab brokerage accounts, a portion of these uninvested cash balances is automatically “swept” into interest-bearing deposit accounts, often held at Schwab Bank or other affiliated banking entities. While clients may earn a modest interest rate on these balances, Schwab strategically invests these aggregated funds into a portfolio of interest-earning assets, such as U.S. Treasury securities, mortgage-backed securities, and corporate debt. The difference between the interest Schwab earns on these investments and the interest it pays out to clients (if any) or the funding cost is its net interest margin. Given the sheer scale of client assets, even a small margin on trillions of dollars translates into billions in revenue. This mechanism benefits Schwab significantly, especially during periods of rising interest rates, as their investment returns tend to increase faster than the rates they pay out to clients.

Lending Activities

Beyond simply investing client cash, Schwab also leverages its balance sheet to engage in various lending activities that generate interest income. The most common forms include margin loans and securities-based lending. Margin loans allow clients to borrow money from Schwab, using their existing securities as collateral, to purchase additional securities or for other personal liquidity needs. Schwab charges interest on these loans, which typically floats with market rates, offering a lucrative revenue stream.

Securities-based lending (SBL) is another crucial component, providing clients with flexible credit lines secured by eligible securities held in their brokerage accounts. These loans are often used for significant personal expenses, real estate, or business ventures, offering a lower-cost alternative to traditional loans in many cases. The interest earned from these lending products, coupled with responsible risk management, contributes substantially to Schwab’s net interest revenue. The ability to lend funds directly to clients against their assets further strengthens Schwab’s position as a comprehensive financial partner, retaining client assets within its ecosystem.

Balance Sheet Management

Charles Schwab also actively manages its own corporate balance sheet to optimize net interest income. This involves strategic deployment of its capital, including retained earnings and debt, into various interest-earning assets. The treasury management team carefully monitors interest rate environments, market liquidity, and credit risk to ensure the company’s investments generate strong returns while maintaining financial stability. This sophisticated approach to asset-liability management (ALM) ensures that Schwab is not just a passive recipient of interest from client cash but an active participant in maximizing its overall interest-generating capacity. The expertise in managing a multi-billion dollar balance sheet is a critical, albeit often unseen, element of its consistent profitability.

Commission-Free Trading and its Hidden Value

The advent of commission-free trading in 2019 was a seismic shift in the brokerage industry, pioneered by firms like Schwab. While this move delighted individual investors, it prompted many to wonder how these companies could possibly continue to generate revenue. The answer lies in a blend of direct and indirect revenue streams associated with trading activity, ensuring that “free” trading is not truly without cost for the broker.

Payment for Order Flow (PFOF)

One of the most significant, and often debated, revenue streams in the commission-free era is Payment for Order Flow (PFOF). When a client places an order to buy or sell a stock through Schwab, instead of routing it directly to an exchange, Schwab (like many other brokers) routes it to a market maker. These market makers pay Schwab a small fee for the privilege of executing these trades. The market makers profit from the “bid-ask spread”—the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept. By aggregating millions of small retail orders, market makers can profit consistently, and they share a portion of that profit with the broker who provides the order flow. While PFOF has been scrutinized for potential conflicts of interest, regulators require brokers to ensure clients receive “best execution,” meaning their orders are filled at the best available price. For Schwab, PFOF represents a substantial revenue source that effectively replaces the commissions once charged.

Securities Lending

Beyond margin loans, Charles Schwab also generates revenue by lending out fully paid securities held in client accounts to other institutions, primarily short sellers. Short sellers borrow shares to sell them, hoping to buy them back later at a lower price to profit from a decline. Schwab facilitates this process by lending out client securities (typically with prior client authorization or through specific account types) and charges a fee or a portion of the interest earned on the cash collateral received from the borrower. This practice, known as securities lending, can be highly profitable, especially for in-demand or “hard-to-borrow” stocks. While clients’ assets are protected and the process is typically low-risk for the brokerage, it provides another layer of recurring revenue from the vast pool of assets under Schwab’s custody.

Mutual Fund & ETF Revenue Sharing

While individual stock and ETF trading might be commission-free, Schwab also offers a wide array of mutual funds and exchange-traded funds (ETFs) from various asset managers. For many of these funds, Schwab receives revenue sharing fees. These are payments from mutual fund and ETF providers to Schwab for marketing their products, providing distribution services, or simply making them available on Schwab’s platform. These fees can be based on a percentage of the assets invested in those funds by Schwab clients. Similarly, Schwab’s own proprietary mutual funds and ETFs generate management fees directly for the company. This “shelf space” or distribution fee model is common in the investment industry and provides a steady, asset-based revenue stream that grows as client investments in these products increase.

Advisory and Asset Management Fees

As Charles Schwab evolved beyond a discount broker, it significantly expanded its advisory and wealth management services. These services, which involve actively managing client portfolios or providing personalized financial guidance, generate substantial revenue through asset-based fees. This category represents a growing and increasingly important part of Schwab’s business model, aligning its success with the growth of its clients’ wealth.

Schwab Intelligent Portfolios (Robo-Advisory)

Schwab was an early adopter and innovator in the robo-advisory space with its Schwab Intelligent Portfolios. This service provides automated, algorithm-driven portfolio management based on a client’s risk tolerance and financial goals. While the core service for many clients is offered without an advisory fee (Schwab earns revenue from the underlying ETFs and cash held in the portfolios), Schwab also offers a premium version, Intelligent Portfolios Premium, which includes unlimited access to a human financial planner for a flat monthly advisory fee. This hybrid model allows Schwab to cater to a broad spectrum of investors, from those seeking a hands-off, low-cost solution to those desiring personalized guidance, all while generating revenue directly or indirectly.

Human-Advised Services

For clients with more complex financial needs or larger asset bases, Schwab offers traditional, human-led financial planning and wealth management services through its network of financial advisors. These services often include comprehensive financial planning, investment management, estate planning, and tax strategy. Clients typically pay an advisory fee, calculated as a percentage of the assets under management (AUM). These fees are recurring and scale directly with the value of the client’s portfolio, making them a stable and high-margin revenue source. The personalized nature of these services builds deep client relationships, fostering retention and attracting new, high-net-worth individuals.

Proprietary Funds & Third-Party Platforms

Schwab not only offers advisory services but also manages its own suite of mutual funds and ETFs. These proprietary funds generate management fees directly for the company from the assets invested in them. Furthermore, Schwab’s platform serves as a hub for thousands of third-party mutual funds and ETFs. While Schwab clients can access these funds, Schwab often enters into agreements with the fund providers to receive administrative or shareholder servicing fees. This allows Schwab to earn revenue without directly managing the assets, effectively acting as a distribution channel and custodian for a vast universe of investment products. The breadth of its offerings ensures that no matter where clients choose to invest, Schwab is likely to derive some form of revenue.

Ancillary Services and Diversification

Beyond the core brokerage and advisory functions, Charles Schwab has diversified its offerings to provide a holistic suite of financial services, generating additional revenue streams and deepening client relationships. These ancillary services further integrate clients into the Schwab ecosystem, making it a one-stop shop for their financial needs.

Banking Services

Through Schwab Bank, a wholly-owned subsidiary, Charles Schwab offers a range of traditional banking services, including checking accounts, savings accounts, and mortgages. While these services provide convenience to brokerage clients, they also contribute to Schwab’s overall profitability. Checking accounts with competitive features often attract and retain clients, while deposits provide additional funding for Schwab’s lending activities, further enhancing net interest revenue. Mortgage lending, while a smaller part of its overall business, also generates interest income and origination fees. This integration of banking and brokerage services creates a sticky client relationship, as funds can easily flow between accounts.

Retirement Plan Services

Charles Schwab is a significant player in the retirement plan market, offering administration and record-keeping services for employer-sponsored retirement plans, such as 401(k)s. Companies pay Schwab fees for managing these plans, which can include administrative fees, asset-based fees on the plan’s investments, and fees for participant education and support. This segment provides a stable, recurring revenue stream from corporate clients and their employees, often leading to individual brokerage relationships as employees gain familiarity with Schwab’s platform. The vast number of participants and the long-term nature of retirement savings make this a valuable and consistent revenue source.

Corporate & Executive Services

Schwab also caters to the specialized needs of businesses and corporate executives. This includes services like stock plan administration for companies (managing employee stock options and restricted stock units), corporate cash management, and executive services for high-net-worth individuals within those corporations. These services are typically fee-based, either as a flat fee or a percentage of assets/transactions. Providing these specialized, high-value services not only generates direct revenue but also positions Schwab as a trusted partner for corporations, potentially leading to further business and wealth management opportunities with their executives and employees.

Conclusion

Charles Schwab’s journey from a discount broker to a financial behemoth is a testament to its adaptive and diversified business model. In an environment where traditional trading commissions have all but vanished, Schwab has masterfully shifted and expanded its revenue streams. Its primary drivers of profitability include significant net interest revenue generated from client cash balances and lending activities, nuanced income from “commission-free” trading through mechanisms like Payment for Order Flow and securities lending, and robust asset management and advisory fees from both automated and human-led services. Complementing these core pillars are a range of ancillary banking, retirement, and corporate services that further cement its financial footprint.

By strategically leveraging its massive client asset base, offering a broad spectrum of financial products and services, and continuously innovating its approach to value creation, Charles Schwab has built a resilient and highly profitable enterprise. Its success demonstrates that in the complex world of finance, profitability is less about a single income stream and more about a sophisticated, interconnected ecosystem designed to serve clients comprehensively while maximizing shareholder value. Understanding these multifaceted revenue sources provides a clearer picture of not just how Schwab makes money, but also the underlying economics driving a significant portion of the modern financial services industry.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.