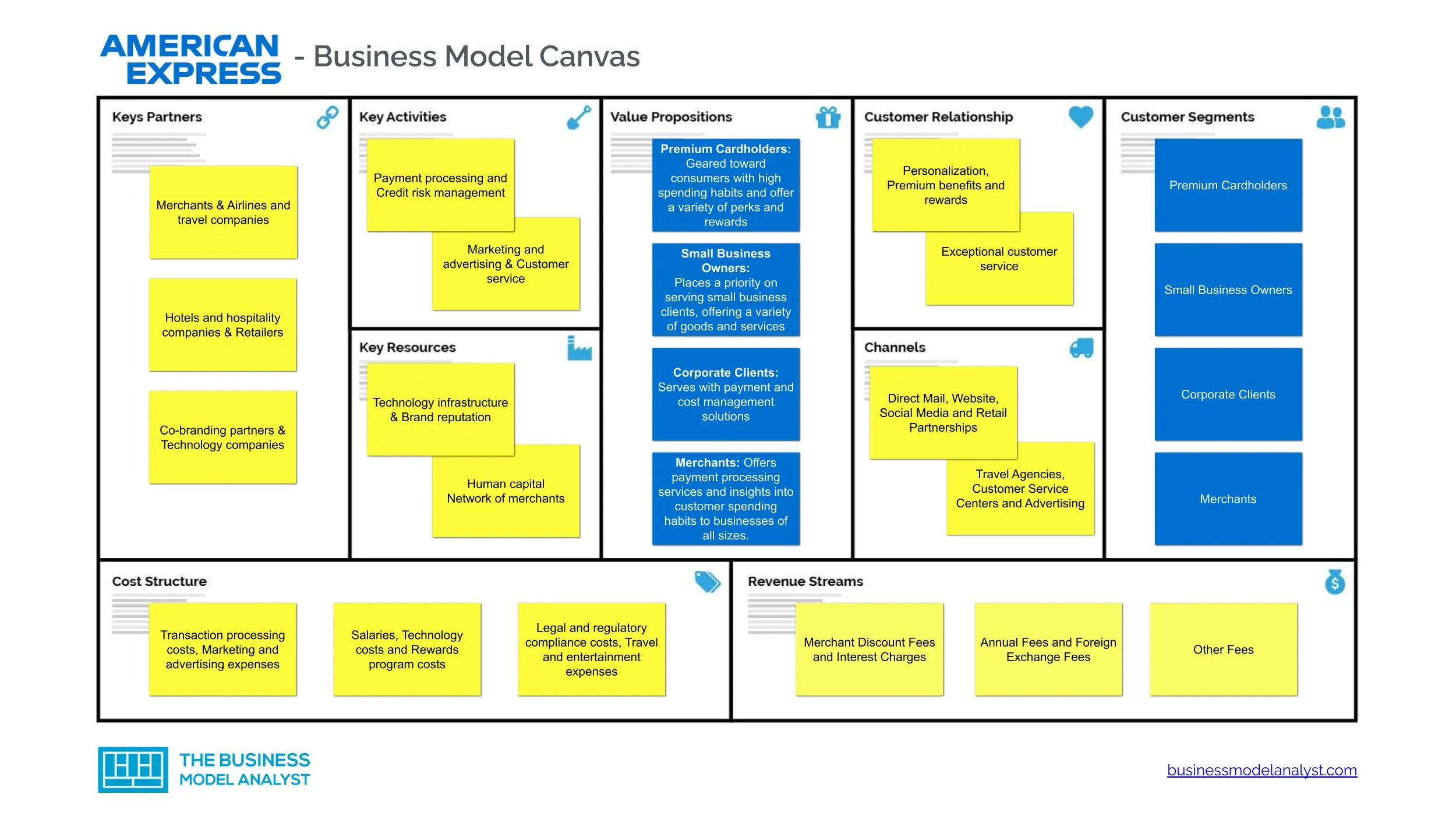

American Express, often recognized by its distinctive Centurion logo, stands as a titan in the global financial services industry. Unlike many of its peers, Amex operates a unique business model that integrates aspects of both a credit card issuer and a payment network. This dual role grants it a distinct position, offering a premium experience to its cardholders while simultaneously forging direct relationships with the merchants who accept its cards. Understanding “how Amex works” means delving into its intricate revenue streams, its value proposition for diverse stakeholders, and the strategic advantages derived from its tightly integrated ecosystem. This article will explore the financial mechanics, operational structure, and key differentiators that define American Express within the competitive landscape of personal and business finance.

The Hybrid Model: Issuer and Payment Network Combined

At the core of American Express’s operational philosophy is its hybrid, or “closed-loop,” business model. This fundamental structure sets it apart from other major payment players and is critical to understanding its financial prowess and strategic decisions.

Distinguishing Amex from Visa/Mastercard

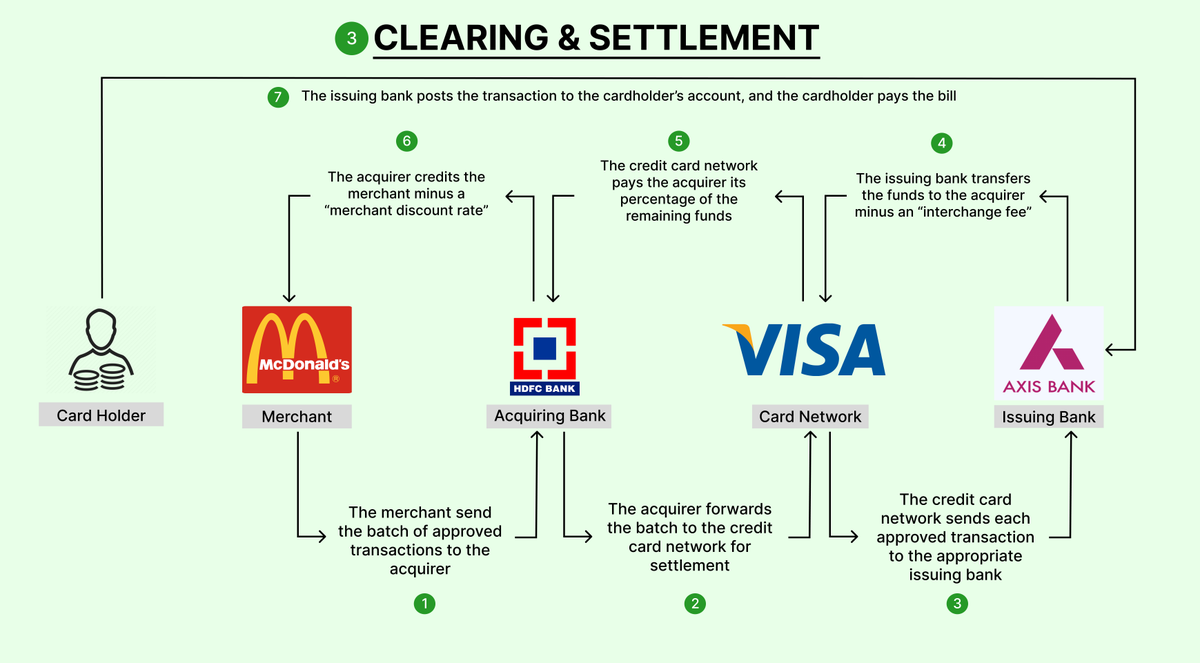

To truly grasp Amex’s unique position, it’s essential to compare it with the more common models represented by Visa and Mastercard. Visa and Mastercard are primarily technology companies and payment networks. They do not issue credit cards themselves; rather, they provide the infrastructure for banks and financial institutions (the issuers) to offer co-branded cards. When you use a Visa or Mastercard, there are typically four parties involved: the cardholder, the merchant, the acquiring bank (which processes transactions for the merchant), and the issuing bank (which issued the card to the cardholder). Visa and Mastercard facilitate the communication and settlement between these banks, earning a small fee for each transaction.

American Express, conversely, acts as both the issuer and the network for most of its proprietary cards. This means that when you use an Amex card, American Express itself is typically the entity that issued you the card and is also the network processing the transaction.

The Closed-Loop System

This integrated approach is often referred to as a “closed-loop” system. In this model, American Express has direct relationships with both the cardholder and the merchant. This direct connection offers several strategic advantages. For cardholders, it allows Amex to gather comprehensive data on spending habits, which in turn informs its sophisticated reward programs, personalized offers, and robust customer service. This direct relationship also enables Amex to maintain a high degree of control over the customer experience from end-to-end. For merchants, Amex also directly manages the acceptance process, facilitating a more streamlined relationship. The closed-loop system is foundational to Amex’s ability to offer a premium product and service, tailor its offerings, and manage its financial risks and rewards more effectively. It creates a powerful ecosystem where Amex can leverage insights from both sides of the transaction to optimize its business and enhance value for its premium clientele.

Revenue Streams: How Amex Generates Income

American Express’s financial stability and profitability are derived from a diverse array of revenue streams, each strategically managed to capitalize on its unique business model and premium market positioning.

Discount Fees (Merchant Fees)

The largest portion of Amex’s revenue typically comes from what are known as “discount fees” or “merchant fees.” These are fees charged to merchants for accepting American Express cards. When a customer uses an Amex card at a store, Amex charges the merchant a percentage of the transaction value. These fees are generally higher than those charged by Visa or Mastercard networks, a fact that has historically been a point of contention for some merchants. The justification for these higher fees from Amex’s perspective is the perceived value of accessing their affluent cardmember base, who are known for higher average spending. Factors influencing these fees include the merchant’s industry, transaction volume, and the type of Amex card being used. This direct merchant relationship, enabled by the closed-loop system, allows Amex to capture a significant portion of the transaction value.

Cardholder Fees and Interest Income

Another significant revenue stream comes directly from cardholders. This includes:

- Annual Fees: A substantial portion of Amex’s revenue comes from annual fees, particularly for its premium charge and credit cards (e.g., Gold, Platinum, Centurion). These fees grant cardholders access to exclusive benefits, rewards programs, and services that differentiate Amex cards from standard offerings.

- Late Payment and Other Fees: Like other financial institutions, Amex charges fees for late payments, returned checks, over-limit transactions, and foreign transaction fees when cards are used internationally.

- Net Interest Income: For its credit card products (which allow cardholders to carry a balance month-to-month), Amex earns interest on outstanding balances. Net interest income is the difference between the interest earned on these outstanding balances and the interest paid by Amex on its own funding sources (such as deposits or borrowed funds). This is a critical component for its traditional credit card offerings, distinct from its “Pay In Full” charge cards.

Other Services

Beyond transaction and interest-based revenues, Amex diversifies its income through various other services. This includes revenue generated from its Global Commercial Services segment, which offers corporate payment solutions, expense management tools, and business financing for small and large enterprises. Its Global Merchant and Network Services also offer consulting and loyalty solutions for merchants. Furthermore, Amex has a travel division that provides booking services and travel-related products, contributing to a broader ecosystem of financial and lifestyle services that cater to its target demographic. This multifaceted approach to revenue generation underpins Amex’s robust financial model.

The Value Proposition for Cardholders and Merchants

American Express meticulously crafts a unique value proposition for both its cardholders and the merchants who accept its cards, carefully balancing the costs and benefits for each stakeholder within its closed-loop system.

For Cardholders: Premium Services and Rewards

Amex primarily targets affluent consumers and businesses, positioning its cards as tools for a premium lifestyle and sophisticated financial management. For cardholders, the value proposition centers around:

- Exceptional Rewards and Benefits: Amex cards are renowned for their lucrative rewards programs, including high points multipliers on specific spending categories (e.g., travel, dining, groceries), transferrable points to airline and hotel loyalty programs, and significant sign-up bonuses.

- Travel-Centric Perks: Many premium Amex cards offer unparalleled travel benefits, such as airport lounge access (Centurion, Priority Pass, Delta Sky Club), hotel elite status, travel credits, concierge services, and comprehensive travel insurance.

- Enhanced Customer Service: Amex prides itself on delivering superior customer service, offering personalized assistance, dedicated account managers for top-tier cardholders, and efficient dispute resolution.

- Purchase Protection and Security: Cardholders benefit from various protections, including extended warranties, purchase protection against damage or theft, and robust fraud prevention measures, providing peace of mind for their expenditures. These features collectively contribute to a perception of exclusivity and superior value that justifies the often higher annual fees.

For Merchants: Access to Affluent Customers

While merchants typically pay higher discount fees to accept Amex compared to other networks, many choose to do so because of the distinct advantages it offers:

- High-Spending Customer Base: Amex cardholders are generally recognized as having higher disposable incomes and higher average transaction values. Merchants accepting Amex gain access to this desirable customer segment, potentially leading to increased sales volumes and higher revenue per customer.

- Loyalty and Repeat Business: Amex cardholders often exhibit strong loyalty to their cards and, by extension, to merchants who accept them. This can translate into repeat business and stronger customer relationships for participating businesses.

- Marketing Opportunities: Amex sometimes partners with merchants for targeted promotions and offers, driving cardholders directly to those businesses. Its brand association can also lend a perception of quality and exclusivity to merchants.

- Business Intelligence: Through its direct relationships, Amex can offer merchants valuable insights into cardholder spending patterns, helping them tailor their strategies. For many businesses, particularly those in high-end retail, hospitality, and travel, the benefits of attracting and serving the affluent Amex customer base often outweigh the higher processing costs, making Amex acceptance a strategic decision rather than a mere operational necessity.

Product Offerings: Beyond the Green Card

American Express’s portfolio extends far beyond a single card, encompassing a sophisticated range of products designed to meet diverse financial needs, from individual consumers to large corporations. Understanding these distinctions is key to comprehending Amex’s market penetration and strategy.

Charge Cards vs. Credit Cards

One of the most defining characteristics of Amex’s product line is the clear distinction between its charge cards and credit cards.

- Charge Cards: Traditionally, Amex built its reputation on charge cards (e.g., Green, Gold, Platinum). The fundamental principle of a charge card is that the full balance must be paid off by the statement due date each month. There is no pre-set spending limit, but this does not mean unlimited spending; rather, the limit is dynamic and adapts based on spending patterns, payment history, and financial capacity. Charge cards do not accrue interest, as carrying a balance is not permitted. They are often associated with premium benefits and rewards, catering to individuals and businesses who prefer to manage their finances by paying in full.

- Credit Cards: In addition to charge cards, Amex also offers traditional credit cards (e.g., Blue Cash Everyday, EveryDay Preferred, co-branded airline/hotel cards). These cards allow cardholders to revolve a balance month-to-month, subject to a pre-set credit limit. Like standard credit cards, they charge interest on the outstanding balance if it’s not paid in full by the due date. This segment of the product line allows Amex to compete more broadly in the credit market and generate significant net interest income.

Personal and Business Cards

Amex strategically segments its card offerings for both individual consumers and businesses, providing tailored solutions for each.

- Personal Cards: These range from entry-level credit cards with cash-back rewards to high-tier premium charge cards like the Platinum Card and the ultra-exclusive, invite-only Centurion Card (Black Card). Each tier offers progressively richer benefits, higher annual fees, and more exclusive access to travel, dining, and lifestyle perks.

- Business Cards: American Express is a strong player in the small business and corporate segments. Business cards (e.g., Business Green Rewards Card, Business Gold Card, Business Platinum Card) are designed to help entrepreneurs and companies manage expenses, track spending, and earn rewards tailored to business operations. These often include features like employee cards, detailed expense reporting, and access to business-specific benefits and financing options.

Lending and Business Solutions

Beyond its card products, American Express provides a suite of broader financial services. This includes various lending solutions for small and medium-sized businesses, such as working capital loans and lines of credit, enabling businesses to manage cash flow and invest in growth. Amex also offers payment processing services for merchants, further solidifying its presence across the entire financial transaction ecosystem. These diverse product offerings demonstrate Amex’s commitment to being a comprehensive financial partner for a wide array of clients.

Risks and Challenges in the Financial Landscape

Despite its established position and unique business model, American Express operates within a dynamic and often challenging financial landscape. Several factors continuously pose risks and necessitate strategic adaptation to maintain its competitive edge and profitability.

Regulatory Scrutiny

The financial services industry is heavily regulated, and American Express, with its dual role as an issuer and network, is subject to intense regulatory scrutiny. Key areas of concern often include:

- Interchange Fees: Regulators globally frequently examine interchange fees (a component of the merchant discount rate) due to concerns about their impact on merchant costs and consumer prices. While Amex’s model is distinct, broad regulatory actions affecting merchant fees can indirectly or directly impact its revenue structure.

- Consumer Protection: Laws related to credit card terms, interest rates, disclosure requirements, and consumer data privacy are continually evolving. Non-compliance or new restrictive regulations could impact Amex’s ability to market products, assess fees, or manage customer relationships.

- Anti-Trust Issues: Amex has faced anti-trust lawsuits concerning its “non-discrimination” clauses, which prevent merchants from steering customers to use lower-cost cards. Although Amex largely prevailed in a significant Supreme Court case, such legal challenges consume resources and highlight ongoing regulatory attention to competition in the payments industry.

Competition from Fintech and Other Networks

The payments landscape is rapidly transforming, driven by technological innovation and the rise of new players.

- Fintech Disruptors: Startups and technology companies (Fintechs) are constantly introducing new payment methods, digital wallets, peer-to-peer payment systems, and alternative lending platforms. These innovations can bypass traditional card networks or offer lower-cost solutions, putting pressure on Amex’s market share and pricing power.

- Traditional Competitors: Visa, Mastercard, and Discover continue to expand their networks and enhance their product offerings. While their models differ, they are direct competitors for both merchant acceptance and cardholder acquisition, especially in the credit card space.

- Global Expansion of Local Networks: In many countries, local payment networks and government-backed initiatives (e.g., UPI in India, Pix in Brazil) are gaining traction, potentially limiting the global reach and dominance of international players like Amex.

Economic Downturns

As a financial institution heavily reliant on consumer spending and credit, American Express is inherently sensitive to macroeconomic fluctuations.

- Reduced Spending: During economic recessions or downturns, consumers and businesses tend to reduce discretionary spending, directly impacting Amex’s transaction volumes and the discount fees it collects.

- Increased Delinquencies: A weakening economy can lead to higher unemployment and financial distress, resulting in increased delinquencies and defaults on credit card balances. This necessitates higher provisions for credit losses, directly impacting profitability.

- Reduced Demand for Premium Products: In tougher economic times, the demand for premium cards with high annual fees and extensive travel benefits may wane as consumers prioritize essential spending over luxury perks. Amex’s focus on affluent customers makes it somewhat resilient but not immune to significant economic shifts. Managing these risks requires continuous innovation, strategic partnerships, prudent financial management, and a keen eye on global economic trends.

Conclusion

American Express operates with a distinctive and powerful business model, carving out a niche as both a credit card issuer and a payment network. This “closed-loop” system allows it to maintain direct relationships with cardholders and merchants alike, fostering a premium ecosystem that prioritizes exceptional service, robust rewards, and exclusive access for its affluent clientele. Amex’s diverse revenue streams, primarily derived from merchant discount fees, cardholder annual fees, and interest income, underscore its financial sophistication.

Despite facing continuous challenges from regulatory scrutiny, fierce competition from evolving fintech solutions, and the inherent volatility of economic cycles, Amex has consistently adapted. Its strategic focus on a high-spending customer base, coupled with a comprehensive suite of personal and business financial products, positions it as a resilient force in the global financial landscape. Ultimately, “how Amex works” is a testament to its enduring ability to deliver perceived value to its users while commanding a significant and profitable share of the world’s financial transactions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.