In the realm of finance, numbers are the language of progress. Whether you are a retail investor tracking the growth of a portfolio, a small business owner calculating profit margins, or an individual trying to optimize a household budget, the ability to work out a percentage of a figure is a fundamental skill. While basic arithmetic might seem elementary, the application of percentages in complex financial scenarios requires a deeper understanding of mathematical relationships.

Mastering these calculations allows you to move beyond surface-level data. It empowers you to interpret market trends, evaluate the true cost of debt, and identify the most lucrative investment opportunities. This guide explores the essential methodologies for calculating percentages within the “Money” niche, providing the professional insights needed to manage capital with precision.

1. The Fundamentals of Financial Percentages

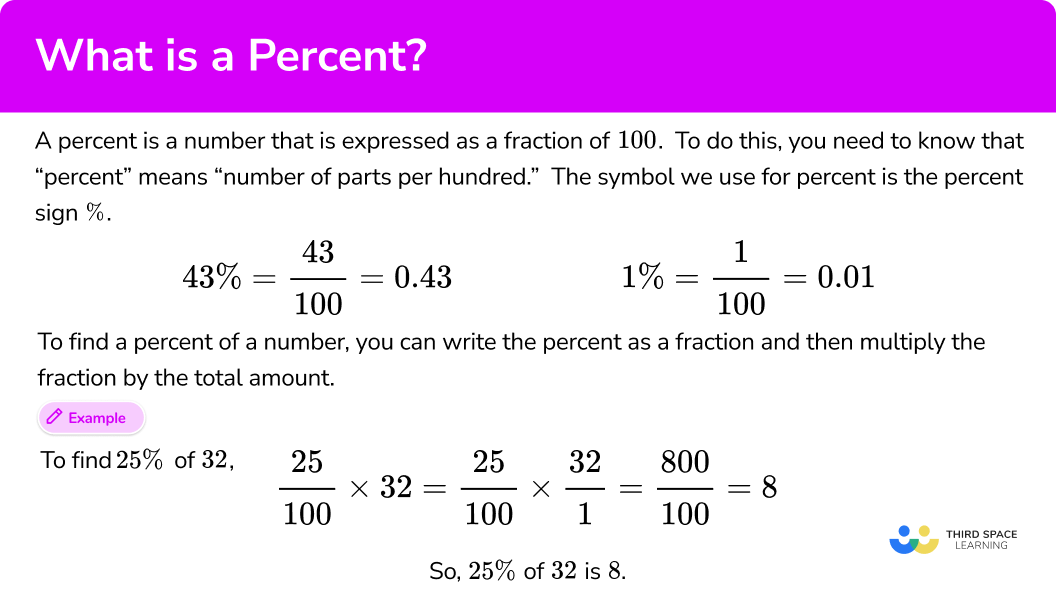

At its core, a percentage is a way of expressing a number as a fraction of 100. In finance, this “part-to-whole” relationship is the foundation for almost every metric we use to measure success. To work out a percentage of a figure, you are essentially determining the relative weight of a specific value within a larger context.

Understanding the “Part over Whole” Concept

The most basic formula to find what percentage one number is of another is:

(Part / Whole) × 100 = Percentage.

For example, if you earned $500 in dividends from a total portfolio value of $10,000, you would divide 500 by 10,000 to get 0.05. Multiplying by 100 gives you 5%. In financial terms, this represents your dividend yield for that specific period. Understanding this ratio is vital for comparing different assets regardless of their absolute dollar value.

The Core Formula for Daily Financial Math

Conversely, you often need to find the specific dollar amount of a known percentage (e.g., “What is 15% of my $4,000 monthly income?”). The formula is:

(Percentage / 100) × Total Figure = Amount.

In this scenario, (15 / 100) is 0.15. Multiplying 0.15 by 4,000 results in $600. This calculation is the bread and butter of personal finance, used for everything from setting aside tax provisions to determining how much to tip at a business lunch.

2. Percentages in Personal Wealth Management

In personal finance, percentages are more than just math; they are a roadmap for wealth accumulation. Relying solely on absolute figures can be misleading because they don’t account for the scale of your initial capital or the passage of time.

Calculating Annualized Returns on Investments (ROI)

The most critical percentage in an investor’s life is the Return on Investment (ROI). This figure tells you how efficiently your capital is working for you. The formula for ROI is:

[(Current Value – Original Cost) / Original Cost] × 100.

If you purchased a stock for $2,000 and its value rose to $2,500, your gain is $500. Dividing $500 by the original $2,000 gives you 0.25, or a 25% ROI. However, seasoned investors also look at “Annualized ROI” to compare a stock held for six months against a bond held for two years. This allows for a “level playing field” analysis of different financial vehicles.

Managing Your Budget with the 50/30/20 Rule

Financial advisors often recommend the 50/30/20 rule as a benchmark for fiscal health. This strategy uses percentages to allocate after-tax income:

- 50% to Needs: Housing, utilities, and groceries.

- 30% to Wants: Dining out, hobbies, and travel.

- 20% to Financial Goals: Debt repayment, emergency funds, and retirement investments.

By working out these percentages against your monthly “take-home” figure, you can quickly identify if your lifestyle is out of sync with your long-term wealth goals. If your “Needs” are consuming 70% of your figure, you know immediately that you are “house poor” or over-leveraged.

Understanding Compounding Interest Rates

Interest rates are percentages that work either for you (savings) or against you (debt). The power of compounding means that a percentage is applied to a figure that is constantly growing. To calculate the future value of an investment with compound interest, the formula is:

A = P(1 + r/n)^(nt)

Where P is the principal, r is the annual interest rate (as a decimal), n is the number of times interest compounds per year, and t is the time in years. Even a small 1% difference in a percentage rate can result in tens of thousands of dollars in difference over a 30-year mortgage or retirement plan.

3. Business Finance and Profitability Metrics

For the entrepreneur or corporate executive, percentages are the ultimate diagnostic tool. They reveal the “health” of a business in ways that a standard balance sheet cannot.

Calculating Gross and Net Profit Margins

A business might generate $1 million in revenue, but if its expenses are $990,000, it is not a healthy enterprise. This is why we calculate margins.

- Gross Profit Margin: [(Revenue – Cost of Goods Sold) / Revenue] × 100. This shows how efficiently a company produces its core products.

- Net Profit Margin: (Net Income / Revenue) × 100. This is the “bottom line” percentage, showing what remains after all taxes, interest, and operating expenses are paid.

High-growth tech companies often have high gross margins but low net margins as they reinvest capital. In contrast, established service firms aim for a steady net margin percentage to ensure dividend payments to shareholders.

Tax Calculations and VAT Adjustments

In many jurisdictions, businesses must calculate Value Added Tax (VAT) or Sales Tax. If a product costs $100 and the tax rate is 20%, the calculation is straightforward ($100 × 0.20 = $20). However, “working backward” is a common business need. If a total receipt is $120 and includes a 20% tax, how do you find the original figure?

You divide the total by (1 + the tax rate).

$120 / 1.20 = $100.

Mastering the “reverse percentage” is essential for accurate bookkeeping and ensuring that tax obligations are not overpaid or under-calculated.

Determining Discount Rates and Markups

Retailers frequently use percentages to drive sales. A “20% discount” is a reduction in the sales price, whereas a “20% markup” is an increase over the cost price. It is a common financial error to confuse the two. A 25% markup on a $100 item results in a $125 price tag. However, a 25% discount on that $125 item brings the price down to $93.75, not back to $100. Understanding these percentage fluctuations is vital for maintaining inventory profitability.

4. Common Pitfalls and Advanced Financial Scenarios

Calculating a percentage of a figure seems simple until you encounter variable data or shifting baselines. In professional finance, the context of the calculation is as important as the math itself.

Percent Increase vs. Percent Decrease

One of the most deceptive aspects of financial math is the asymmetry between gains and losses. If a $10,000 investment drops by 50%, it is worth $5,000. To get back to its original $10,000 value, it must increase by 100%, not 50%.

The formula for percentage change is:

[(New Value – Old Value) / Old Value] × 100.

In the recovery phase, the “Old Value” is now the lower $5,000, making the required percentage of growth much higher. This is why capital preservation is the first rule of professional investing.

Understanding “Basis Points” in Interest Rate Fluctuations

In the world of banking and bonds, percentages are often too “large” a unit for precision. Instead, professionals use Basis Points (BPS). One basis point is equal to 1/100th of 1 percent (0.01%).

If the Federal Reserve raises interest rates from 4.25% to 4.50%, they have raised rates by 25 basis points. While a 0.25% change sounds negligible to a layperson, on a $100 million corporate loan, those 25 basis points represent a $250,000 increase in annual interest expenses.

5. Leveraging Digital Tools for Financial Accuracy

While manual calculations are necessary for quick checks, modern financial management relies on automation to eliminate human error.

Using Spreadsheet Formulas

In Excel or Google Sheets, working out a percentage of a figure is simplified through cell references. To find the percentage of a total, you would use =A1/B1 and then format the cell as a “Percentage.” For more complex financial modeling, functions like IRR (Internal Rate of Return) or PMT (Payment) use percentage inputs to project long-term financial outcomes.

Professional Financial Calculators and Apps

For real estate and investment banking, dedicated financial calculators (like the HP 12C) are industry standards. These devices have built-in logic for “Time Value of Money,” allowing users to input a percentage (the interest rate) and a figure (the principal) to solve for future wealth or debt amortization schedules.

Ultimately, whether you are using a high-powered software suite or a simple pen and paper, the ability to work out a percentage of a figure is the gateway to financial literacy. It allows you to see past the raw numbers and understand the underlying health, growth, and risks of any financial endeavor. By mastering these formulas and understanding their application in wealth management and business, you position yourself to make smarter, more informed, and more profitable decisions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.