In the sophisticated world of modern finance, we often find ourselves leaning heavily on complex algorithms, high-frequency trading bots, and automated accounting software. However, the bedrock of sound financial decision-making remains rooted in fundamental arithmetic. Among these foundational skills, the ability to subtract fractions is surprisingly critical. Whether you are calculating the “spread” between interest rates, determining the remaining equity in a real estate partnership, or adjusting a portfolio’s asset allocation, mastering fractional subtraction is a prerequisite for financial literacy.

While most individuals learn the mechanics of fractions in primary school, the practical application in a professional or investment context requires a deeper level of precision and a “Money” mindset. This guide explores the “how-to” of subtracting fractions while framing it within the essential context of personal and business finance.

The Mathematics of Money: Why Fractions Matter in Finance

Before diving into the mechanics, one must understand why fractions—and the ability to manipulate them—remain relevant in an era dominated by decimals. In the financial markets, fractions represent the “pieces of the whole” that define ownership, debt, and cost.

Decimal vs. Fractional Representation in Markets

While the U.S. stock market moved to “decimalization” in 2001, many areas of finance still rely on fractional logic. Bond yields, interest rate “basis points,” and fractional share ownership in fintech apps like Robinhood or Schwab require an understanding of how parts of a whole interact. Subtracting fractions allows an investor to understand the net difference between two yields or the reduction in a stake of a private equity venture. When you see a “quarter-point” drop in the Federal Reserve’s interest rate, you are dealing with the subtraction of $1/4$ from a whole or another fraction.

The Role of Basic Arithmetic in Financial Literacy

Financial literacy is not just about knowing where to invest; it is about the precision of the calculation. A mistake in subtracting a fractional fee from a projected return can lead to significant discrepancies over a 30-year investment horizon. If an expense ratio is $3/4%$ and you are comparing it to a fund with a $1/2%$ ratio, the ability to quickly subtract those fractions ($3/4 – 1/2 = 1/4$) allows for immediate clarity in cost-benefit analysis.

Step-by-Step Guide: How to Subtract Fractions in Financial Calculations

To subtract fractions effectively in a business or personal finance setting, one must follow a disciplined process to ensure accuracy. This is particularly important when dealing with “mixed numbers,” which often appear in real estate (e.g., $5 frac{1}{2}$ acres) or debt terms.

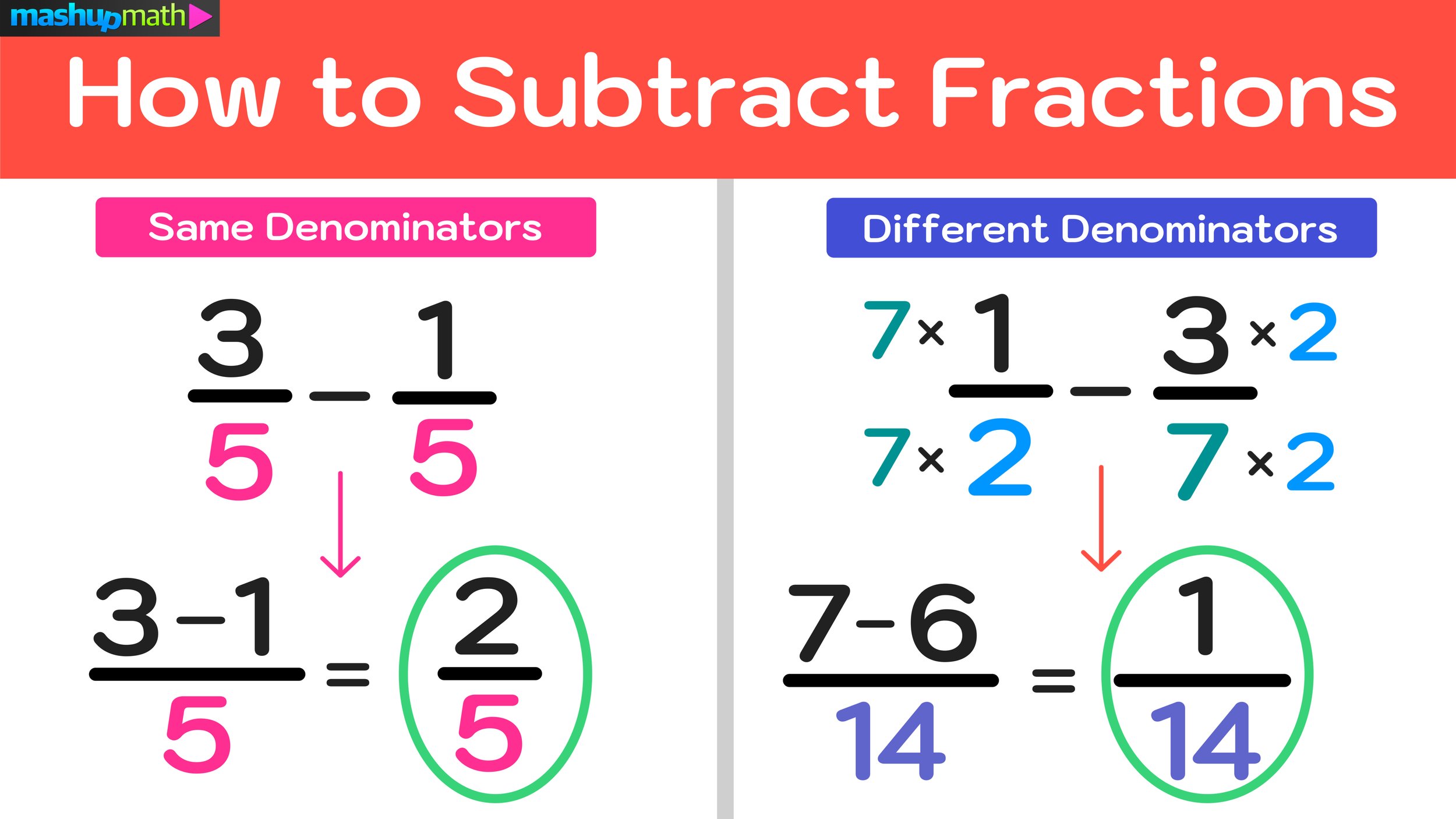

Finding the Lowest Common Denominator (LCD)

The most frequent hurdle in subtracting fractions is dealing with unequal denominators (the bottom number). In finance, denominators often represent different units of time or different “pools” of capital.

To subtract $1/4$ from $7/8$ (perhaps representing a reduction in a dividend yield), you must first find a common denominator. In this case, $8$ is the common denominator. You convert $1/4$ into $2/8$.

The calculation then becomes:

$7/8 – 2/8 = 5/8$.

In a financial context, the LCD ensures that you are “comparing apples to apples.” You cannot subtract a quarterly expense from an annual return without first finding a common denominator of time.

Handling Mixed Numbers in Business Accounting

Mixed numbers consist of a whole number and a fraction (e.g., $10 frac{1}{4}$ percent). When subtracting these—for instance, if a business owner owns $10 frac{1}{4}%$ of a company and sells $2 frac{1}{2}%$—the process requires two steps:

- Convert to Improper Fractions: $10 frac{1}{4}$ becomes $41/4$. $2 frac{1}{2}$ becomes $5/2$ (or $10/4$).

- Subtract: $41/4 – 10/4 = 31/4$.

- Convert Back: $31/4 = 7 frac{3}{4}%$.

This level of precision prevents the “rounding errors” that frequently plague amateur investors who rely solely on rough decimal approximations.

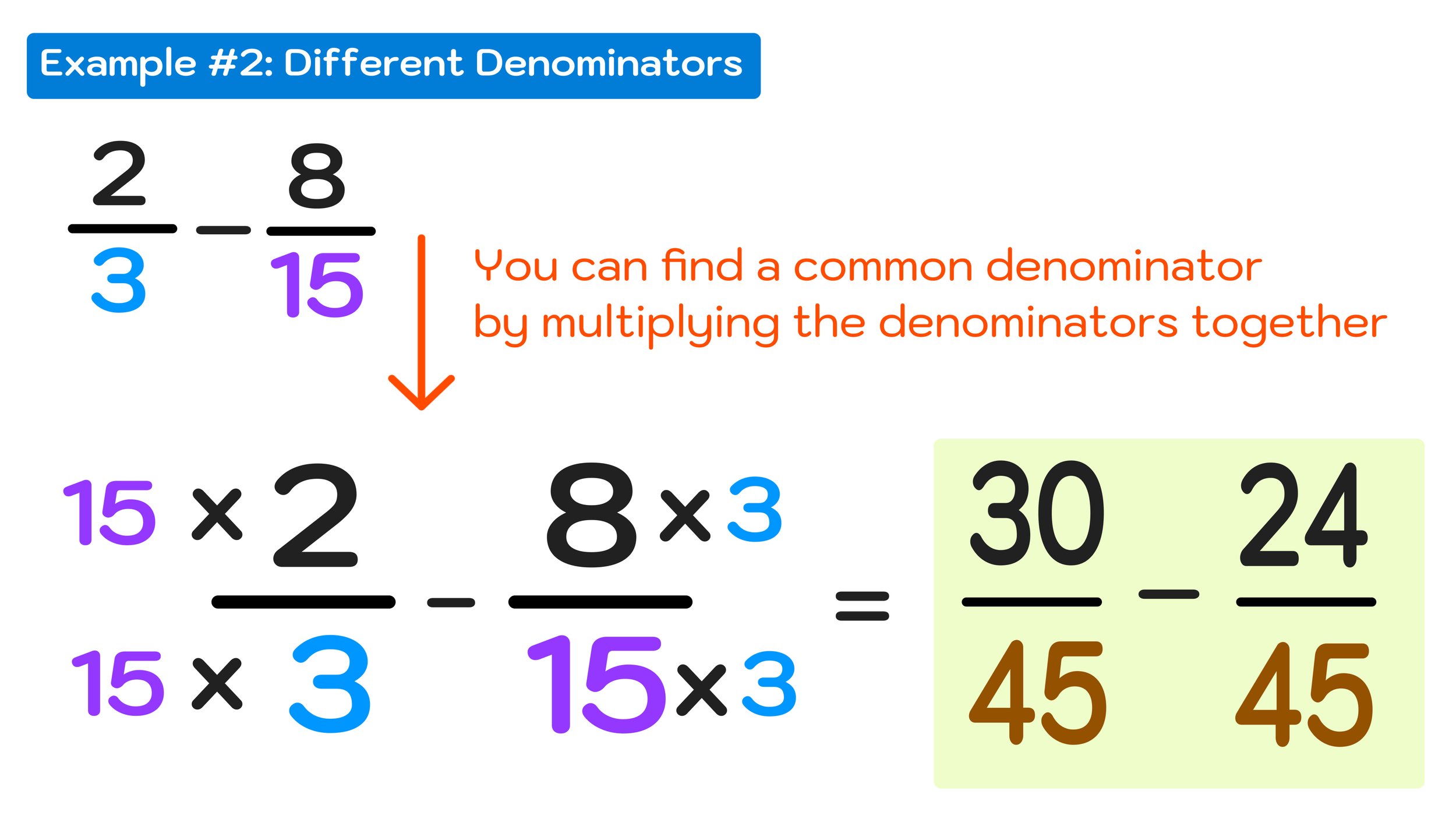

Subtracting Fractions with Unequal Denominators

When denominators are not easily compatible, such as subtracting $1/3$ of a portfolio (allocated to high-risk assets) from a total remaining liquid balance of $4/5$, you must multiply the denominators to find a common ground.

$3 times 5 = 15$.

Convert $4/5$ to $12/15$ and $1/3$ to $5/15$.

The result: $7/15$.

This represents the remaining fractional portion of the portfolio. Understanding this allows an investor to see that slightly less than half of their assets remain liquid.

Real-World Applications: From Dividends to Debt

The theory of subtraction becomes much more engaging when applied to wealth-building scenarios. In money management, “subtraction” is often synonymous with “cost” or “dilution.”

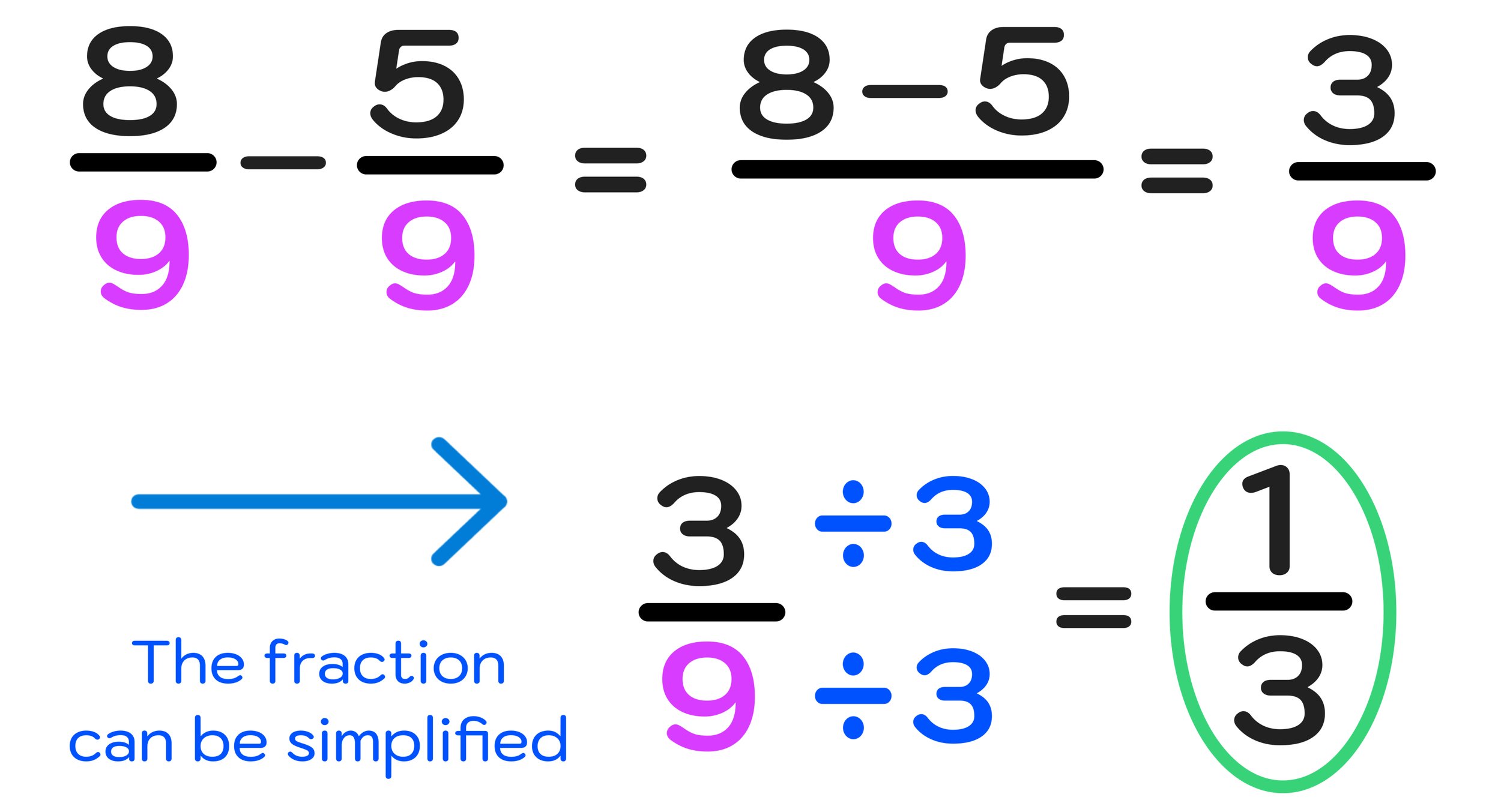

Calculating Net Gains After Fractional Fees

Every investment comes with a cost. If you are promised a $5/8%$ return on a short-term note but must pay a $1/16%$ brokerage fee, your net return is determined by subtraction.

$5/8 – 1/16 = 10/16 – 1/16 = 9/16%$.

While these numbers seem small, on a principal of $1,000,000, the difference between $10/16$ and $9/16$ is substantial. Professional wealth managers perform these subtractions to ensure that the “net” is always the focus, rather than the “gross.”

Prorating Expenses and Rental Agreements

In real estate and property management, fractions are used to prorate rent. If a tenant moves out $1/3$ of the way through a month, and they have already paid for $3/4$ of the month due to a prior credit, the landlord must subtract the fractions to find the appropriate refund or charge.

Mastering the subtraction of these time-based fractions ensures that the business maintains its cash flow integrity and remains legally compliant with lease agreements.

Advanced Financial Logic: The “Subtraction” Mindset in Portfolio Optimization

In high-level wealth management, subtraction is more than just an arithmetic operation; it is a strategic philosophy. Effective portfolio management often involves “subtracting” underperforming assets or “fractionalizing” holdings to mitigate risk.

Reducing Risk by Subtracting Volatile Assets

Imagine a portfolio as a single “unit.” If $2/5$ of that unit is tied up in volatile crypto-assets and $1/4$ is in emerging markets, an investor might decide to reduce their exposure to volatility by “subtracting” a fraction of those holdings.

By subtracting $1/10$ from the crypto-holding ($2/5 – 1/10 = 4/10 – 1/10 = 3/10$), the investor has strategically rebalanced their wealth. This fractional adjustment is the essence of “trimming a position,” a common term in professional trading.

The Impact of Small Fractional Reductions on Long-Term Growth

The most powerful concept in finance is compounding. Conversely, the most destructive force is “negative compounding” caused by fractional fees. Subtracting a seemingly tiny fraction from your annual growth rate—say, $1/4%$ for an advisor fee and $1/8%$ for fund expenses—totaling $3/8%$, can result in hundreds of thousands of dollars lost over a lifetime.

By understanding how to subtract these fractions, an investor can visualize the “drag” on their wealth and seek out lower-cost fractional alternatives, such as index funds with expense ratios near zero.

Digital Tools and Modern Solutions for Fractional Math

While mental math is a valuable skill for any business leader or investor, the modern financial landscape provides tools to ensure that these subtractions are error-free.

Using Excel and Financial Calculators for Precision

Software like Microsoft Excel allows users to format cells specifically as “Fractions.” When building a budget or an investment tracker, using the fraction format (e.g., # ?/?) ensures that the software handles the LCD and subtraction internally while displaying the result in a way that is intuitive for the user.

For example, if you enter =1/2 - 1/8 in a fraction-formatted cell, Excel will return 3/8. This is particularly useful for traders who still think in terms of “ticks” or “points,” which are inherently fractional.

The Evolution of Fractional Investing Apps

We are currently in a “Fractional Revolution.” Apps now allow users to buy $1/1000$ of a share of Berkshire Hathaway or $1/10$ of a piece of fine art. As these assets are bought and sold, the underlying technology is constantly performing fractional subtraction to update user balances. Understanding the math behind these apps allows the consumer to be a participant in the market rather than just a spectator. It demystifies the process, allowing for a clearer understanding of how “fractional ownership” actually works when it comes time to liquidate or “subtract” those assets from a digital wallet.

Conclusion: The Value of Fractional Accuracy

How do you subtract fractions? You find a common denominator, adjust the numerators, and perform the subtraction. But in the world of Money, the answer is much deeper. You subtract fractions to find the truth behind the numbers—to see the real profit after fees, the real equity after debt, and the real growth after inflation.

By mastering this fundamental arithmetic, you equip yourself with the tools necessary for sophisticated wealth management. Financial success is rarely the result of one giant leap; it is the result of thousands of small, precise calculations. Whether you are a business owner, a retail investor, or someone simply looking to master their personal budget, remember that the “fractions” of your financial life add up—or subtract down—to your ultimate net worth. Professionalism in finance starts with the precision of your math.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.