For over a decade, Bitcoin was primarily viewed through a singular lens: a speculative investment or a digital version of gold. The prevailing sentiment was to “HODL”—to hold onto the asset indefinitely in hopes of massive price appreciation. However, as the ecosystem matures and institutional adoption stabilizes, the conversation is shifting toward the practical utility of digital currency.

The question is no longer just “What is Bitcoin worth?” but rather “How do you spend Bitcoin?” Transitioning from a passive investor to an active user of the network requires a shift in financial mindset. Spending Bitcoin involves navigating a unique landscape of liquidity, transaction costs, and tax implications. This guide explores the financial mechanics of using Bitcoin as a medium of exchange and how it integrates into a modern personal finance strategy.

The Evolution of Bitcoin from Store of Value to Medium of Exchange

In the early days of cryptocurrency, using Bitcoin for a purchase was a novelty—most famously illustrated by the purchase of two pizzas for 10,000 BTC in 2010. Today, the landscape is vastly different. Bitcoin has evolved into a sophisticated financial instrument that offers a borderless, permissionless way to transfer value.

Understanding the Practical Utility of Crypto

From a financial perspective, the utility of Bitcoin lies in its ability to bypass traditional banking intermediaries. For individuals in the “Money” niche, this means lower cross-border fees and the ability to settle large transactions without the multi-day delays associated with SWIFT transfers. As more merchants integrate crypto-payment processors, Bitcoin is moving away from being a frozen asset and toward being a liquid currency that can be used for everything from a cup of coffee to a luxury real estate purchase.

The Shift in Consumer Behavior

We are witnessing a psychological shift in how crypto-holders view their portfolios. Modern financial planning now often includes a “crypto-to-fiat” strategy. Instead of selling large chunks of Bitcoin for cash and triggering massive tax events, many users are opting for “micro-spending”—using small amounts of their holdings for daily expenses. This behavior reflects a growing confidence in the long-term stability of the network and a desire for financial sovereignty.

Navigating the Practical Ways to Spend Your Bitcoin

Spending Bitcoin is not as simple as swiping a traditional credit card, but it is becoming increasingly streamlined. There are three primary avenues through which an individual can convert their digital holdings into goods and services.

Direct Peer-to-Peer Transactions

The most “purist” way to spend Bitcoin is through direct peer-to-peer (P2P) transfers. This involves sending BTC directly from your wallet to a merchant’s wallet via a QR code. While this was once reserved for tech-savvy enthusiasts, many small businesses and independent contractors now accept direct Bitcoin payments to avoid the 3% processing fees charged by credit card companies. From a personal finance standpoint, this is the most cost-effective method, as it eliminates the middleman.

Utilizing Crypto Debit Cards

For those who want the convenience of traditional banking with the power of crypto, Bitcoin debit cards (offered by companies like Coinbase, BitPay, and Crypto.com) are the primary tool. These cards are linked to your crypto account and automatically convert your Bitcoin into the local fiat currency (like USD or EUR) at the moment of sale. This allows you to spend your Bitcoin anywhere that accepts Visa or Mastercard. While convenient, it is important to monitor the conversion fees and “spreads” that these providers charge, as they can eat into your purchasing power.

Buying Gift Cards with Digital Assets

A popular “middle-ground” for spending Bitcoin is the use of gift card platforms like Bitrefill or Fold. These services allow you to buy gift cards for major retailers—Amazon, Uber, Airbnb, and Starbucks—using Bitcoin. This method is often preferred for financial privacy and ease of use, as it avoids the need for a merchant to directly support crypto payments. Often, these platforms offer “sats-back” (cashback in the form of Bitcoin), which serves as a financial incentive for the user.

Major Sectors and Retailers Accepting Bitcoin Today

The merchant map for Bitcoin is expanding rapidly. While we are not yet at a point where every corner store accepts digital currency, major sectors have embraced the technology, providing significant outlets for those looking to spend their digital wealth.

Luxury Goods and High-End Assets

The high-end market was an early adopter of Bitcoin. Real estate agencies in markets like Dubai and Miami frequently list properties in BTC. Similarly, luxury watch dealers and exotic car dealerships have found that crypto-wealthy individuals are eager to diversify their digital holdings into hard assets. For the high-net-worth individual, spending Bitcoin on a tangible asset is often a strategic move to rebalance a portfolio that has become too heavily weighted in volatile digital currencies.

Travel and Global Tourism

Travel is perhaps the most logical use case for a borderless currency. Platforms like Travala.com allow users to book millions of hotels and flights using Bitcoin. This eliminates the need for currency exchange and the associated bank fees when traveling internationally. For the frequent flyer, maintaining a “travel fund” in Bitcoin can be a hedge against the devaluation of local fiat currencies in specific regions.

Everyday Retail and E-commerce

E-commerce giants and tech-forward companies are leading the charge in daily retail. Microsoft allows users to top up their accounts with Bitcoin, and Overstock.com was a pioneer in accepting crypto for home goods. Even in the physical world, the integration of the Lightning Network—a layer-2 solution for Bitcoin—is making it possible for fast-food chains and local boutiques to accept near-instant, low-fee Bitcoin payments.

The Financial Implications of Spending Digital Assets

Before you begin spending your Bitcoin, it is crucial to understand the fiscal responsibilities involved. Unlike spending cash, spending Bitcoin is considered a “taxable event” in many jurisdictions, including the United States (under IRS guidelines).

Tax Consequences and Capital Gains

In the eyes of many tax authorities, Bitcoin is treated as property, not currency. This means that every time you spend Bitcoin, you are technically “selling” that asset. If the value of the Bitcoin increased from the time you acquired it to the time you spent it, you owe capital gains tax on the difference. Keeping meticulous financial records is essential. Many users now employ crypto-tax software to track the “cost basis” of their spending to ensure they remain compliant with the law.

Transaction Fees and Network Costs

Every Bitcoin transaction requires a fee paid to miners to process the data on the blockchain. During times of high network congestion, these fees can spike, making a $5 coffee purchase cost $15 in fees. To manage your money wisely, it is important to understand when to use the main blockchain (for large purchases) and when to use the Lightning Network (for small, daily transactions). The Lightning Network reduces fees to a fraction of a cent, making micro-transactions financially viable.

Opportunity Cost vs. Purchasing Power

One of the biggest financial hurdles to spending Bitcoin is the “opportunity cost.” Because Bitcoin has a fixed supply and the potential for high appreciation, spending it today might mean missing out on significant gains tomorrow. A common financial strategy to mitigate this is the “Spend and Replace” method: whenever you spend $100 worth of Bitcoin, you immediately buy $100 worth of Bitcoin with fiat currency. This allows you to support the circular economy of crypto without reducing your overall investment position.

Essential Tools for Managing Your Bitcoin Spending

To transition into using Bitcoin as a functional part of your financial life, you need the right digital infrastructure. Efficiency and security are the two pillars of a crypto-spending strategy.

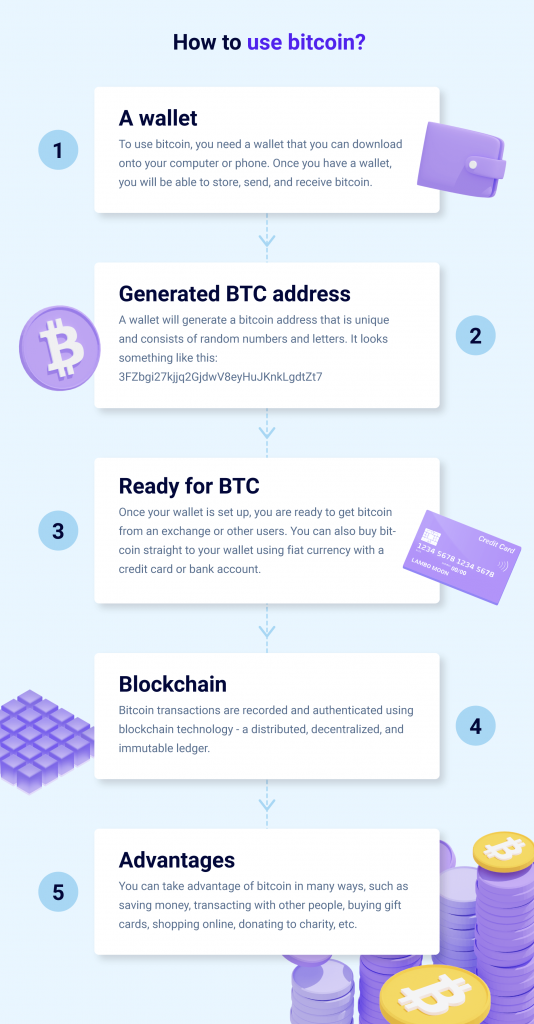

Selecting the Right Wallet for Daily Use

Not all wallets are created equal. For spending, you likely need a “Hot Wallet” (a mobile app wallet) rather than a “Cold Wallet” (hardware storage). Mobile wallets like Muun, BlueWallet, or Phoenix are designed for quick transactions and often support the Lightning Network. These wallets should be treated like your physical wallet—keep only as much “spending money” in them as you need, while keeping your main savings in a more secure, offline hardware device.

Security Best Practices for Liquid Assets

When you start spending Bitcoin, you interact with more third-party interfaces, which increases your surface area for potential security risks. Always ensure you are using reputable payment processors and avoid clicking on unsolicited links claiming to accept Bitcoin. From a financial security standpoint, never share your private keys or seed phrases with a merchant. A legitimate Bitcoin transaction only requires the recipient’s public address or a generated QR code.

By integrating these tools and strategies, Bitcoin ceases to be a dormant asset on a ledger and becomes a dynamic tool for financial freedom. Whether you are seeking to avoid bank fees, diversify into luxury assets, or simply participate in the future of finance, knowing how to spend Bitcoin effectively is an essential skill for the modern era.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.