Discovering that you owe the Internal Revenue Service (IRS) more than you can afford to pay is a significant source of financial stress for millions of Americans. Whether it stems from an unexpected windfall, a mistake in withholding, or the complexities of self-employment income, tax debt can feel like an insurmountable obstacle. However, the IRS is often more flexible than taxpayers realize. Their primary goal is to collect the revenue owed, and they have established several “Installment Agreements” or payment plans to facilitate this.

In the world of personal finance, managing tax debt is about more than just clearing a balance; it is about protecting your credit, avoiding levies, and maintaining your long-term financial health. This guide provides an in-depth look at how to navigate the IRS payment plan system, the strategic financial decisions involved, and the steps required to regain control of your balance sheet.

Understanding Your Options: The Different Types of IRS Installment Agreements

Before clicking “apply,” it is vital to understand that not all payment plans are created equal. The IRS offers different structures based on how much you owe and how quickly you can pay it back. Choosing the right one can save you hundreds of dollars in setup fees and interest.

Short-Term Payment Plans

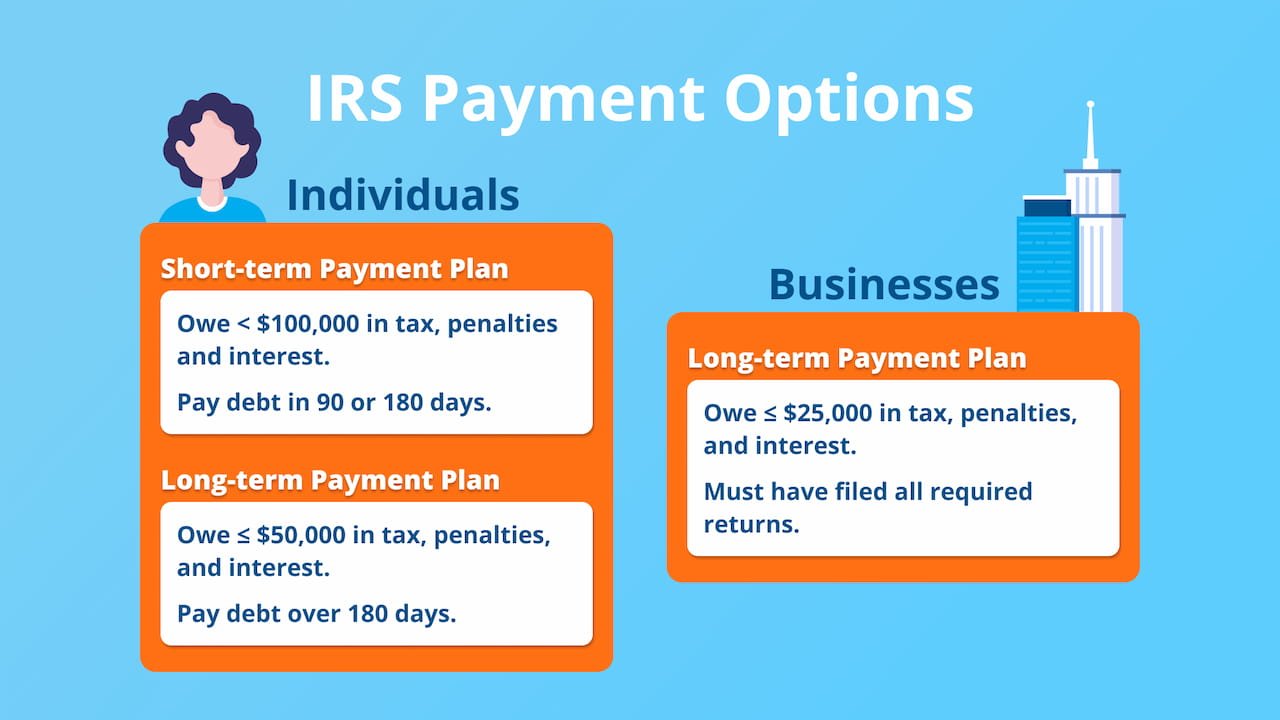

A short-term payment plan is designed for individuals who can pay their tax liability in full within 180 days (6 months). This is often the most cost-effective route because the IRS does not charge a setup fee for this arrangement. While interest and late-payment penalties still accrue until the balance is zero, the absence of an administrative fee makes it an ideal choice for those expecting a bonus, a real estate closing, or a significant commission in the near future.

Long-Term Installment Agreements

If you require more than 180 days to settle your debt, you will need a long-term installment agreement. These plans allow for monthly payments over a period of up to 72 months (6 years). Unlike the short-term option, long-term plans involve a setup fee, which varies depending on how you choose to pay.

Direct Debit vs. Non-Direct Debit

The method of payment significantly impacts your costs. A Direct Debit Installment Agreement (DDIA) is the IRS’s preferred method, where payments are automatically withdrawn from your bank account. Because this reduces the risk of default, the IRS offers a lower setup fee for DDIAs. Non-direct debit options—where you pay via check, money order, or the Electronic Federal Tax Payment System (EFTPS) manually—carry higher setup fees and a higher risk of accidentally missing a payment.

Eligibility Requirements and Necessary Documentation

To enter into a payment plan, you must meet specific criteria. The IRS views a payment plan as a good-faith agreement, and they expect certain standards of financial compliance in return.

The Requirement of Tax Compliance

The most critical prerequisite for any IRS payment plan is that you must be “compliant” with your tax filings. This means every required tax return for previous years must be filed. You cannot set up a payment plan for a debt if you have outstanding returns that haven’t been submitted. If you are behind on filing, your first step is to get your paperwork in order, even if you cannot pay the balance due on those returns.

Financial Thresholds for Individuals and Businesses

For individuals, the process is streamlined if the total amount owed (including tax, penalties, and interest) is $50,000 or less. In these cases, you can typically apply online without providing a detailed financial statement. If you owe more than $50,000, the IRS may require you to fill out Form 433-F (Collection Information Statement), which provides an exhaustive look at your assets, monthly income, and living expenses to determine your ability to pay.

For small businesses, the threshold for a streamlined “In-Business Trust Fund Express” installment agreement is generally $25,000 or less. Business owners must ensure they are current on all payroll tax deposits to remain eligible.

Necessary Information for Application

When you are ready to apply, ensure you have the following information at hand:

- Your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Your filing status and the address from your most recently filed return.

- The total amount you owe.

- Your bank account and routing numbers (if opting for direct debit).

- A clear understanding of your monthly budget to propose a sustainable payment amount.

Step-by-Step Guide to Applying for a Payment Plan

The IRS has modernized its systems, making it possible for most taxpayers to resolve their debt without ever speaking to an agent. However, for complex cases, traditional methods remain available.

Using the Online Payment Agreement (OPA) Tool

The most efficient way to set up a plan is through the IRS.gov website. The Online Payment Agreement (OPA) tool is available to individuals who owe combined income tax, penalties, and interest of $50,000 or less.

- Log in: You will need to create or log in to your IRS Online Account using identity verification services like ID.me.

- Select the Plan: Based on your balance, the system will offer short-term or long-term options.

- Determine Your Payment: You can choose your monthly payment amount and the day of the month the payment is due.

- Confirm: Once submitted, you usually receive immediate notification of whether your plan has been approved.

Applying via Form 9465

If you prefer not to use the online portal, or if you do not meet the criteria for the OPA, you can file Form 9465, Installment Agreement Request. This form can be mailed to the IRS along with your tax return or sent separately if you have already filed. While this method is slower, it allows you to explain specific financial hardships that the online tool might not account for.

Phone and In-Person Options

For those with significant debt (over $50,000) or complex business structures, a phone interview with an IRS representative or a visit to a Taxpayer Assistance Center may be required. In these scenarios, be prepared to negotiate. The IRS representative will look at your “allowable living expenses” to decide how much of your discretionary income should be diverted to your tax debt.

Managing Your Plan: Costs, Compliance, and Revisions

Setting up the plan is only the first half of the battle. Maintaining the agreement is essential to avoid “default,” which can lead to wage garnishments and bank levies.

Understanding the Cost of Borrowing from the IRS

It is a common misconception that a payment plan stops interest. In reality, the IRS interest rate—which is adjusted quarterly—continues to accrue on the unpaid balance. Additionally, the “failure-to-pay” penalty continues to apply, though it is usually reduced from 0.5% per month to 0.25% per month while an installment agreement is in effect. From a financial perspective, if you have access to a personal loan or a home equity line of credit with a lower interest rate, it may be mathematically wiser to pay off the IRS in full and owe a private lender instead.

The “Stay Current” Rule

The most important rule of an IRS installment agreement is that you must remain compliant with future tax obligations. If you set up a plan for 2023 taxes but then owe a balance for 2024 taxes that you don’t pay, your existing agreement will go into default. To protect your plan, you must ensure your future withholdings or estimated tax payments are sufficient to cover your liabilities moving forward.

Modifying Your Agreement

Financial circumstances change. If you lose your job or face an emergency expense, you can request a modification to your payment plan. You can do this through the OPA tool or by calling the IRS. There is typically a small fee for modifying an existing agreement, but it is much cheaper than the penalties associated with a default.

Strategic Financial Planning: Avoiding Future Tax Debt

Successfully setting up a payment plan is a “reactive” financial move. To achieve true financial wellness, you must transition to a “proactive” strategy to ensure you never find yourself in this position again.

Adjusting Your Withholding (Form W-4)

For W-2 employees, the most common reason for tax debt is an outdated Form W-4. If you have had a change in marital status, a new child, or a secondary income stream, use the IRS Tax Withholding Estimator tool to determine if you need to increase the amount taken out of your paycheck.

Managing Self-Employment and Side Hustles

The “gig economy” has led to a surge in tax debt because many independent contractors forget to set aside money for taxes. A best practice in personal finance is to divert 25% to 30% of every freelance check into a high-yield savings account designated specifically for “Tax Reserves.” Paying quarterly estimated taxes (Form 1040-ES) is not just a suggestion; it is a requirement that prevents an overwhelming bill in April.

When to Seek Professional Help

While a streamlined installment agreement is DIY-friendly, certain situations warrant professional intervention. If you owe more than $100,000, if the IRS has already issued a Notice of Federal Tax Lien, or if you believe you qualify for an “Offer in Compromise” (settling for less than you owe), you should consult a Certified Public Accountant (CPA) or an Enrolled Agent (EA). These professionals can represent you before the IRS and ensure your rights are protected.

By viewing an IRS payment plan as a tool rather than a punishment, you can manage your tax debt with professional precision. It is a structured path toward financial redemption, allowing you to settle your obligations while maintaining the liquidity needed for your daily life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.