The landscape of personal finance has undergone a radical transformation over the last decade. The days of carrying bulky wallets filled with paper currency or waiting three to five business days for a bank wire to clear are rapidly fading into obsolescence. In their place, a suite of sophisticated financial tools has emerged, with Cash App—developed by Block, Inc.—standing at the forefront of the mobile payment revolution. Whether you are splitting a dinner bill, paying a freelance contractor, or sending a gift to a family member, understanding how to navigate this ecosystem is essential for modern financial literacy.

This guide explores the intricacies of sending money via Cash App, framing it not just as a technical maneuver, but as a strategic component of your personal financial toolkit.

The Evolution of Modern Finance: Understanding the Role of Cash App

Before diving into the mechanics of a transaction, it is vital to understand the position Cash App holds within the financial sector. It is more than a simple peer-to-peer (P2P) platform; it has evolved into a hybrid of a checking account, an investment platform, and a digital wallet.

Bridging the Gap Between Traditional Banking and Digital Wallets

For many years, the “unbanked” or “underbanked” population faced significant hurdles in accessing digital financial services. Cash App addressed this by providing a low-barrier entry point to the financial system. Unlike traditional banks that may require high minimum balances or extensive credit checks, Cash App allows users to establish a financial presence with just a smartphone. By providing a routing and account number to its users, it bridges the gap between the rigid structures of legacy banking and the fluidity of digital-first finance.

Why Cash App Has Become a Staple in Personal Finance

The platform’s ubiquity stems from its speed and social integration. In the context of personal finance, “velocity of money” refers to how quickly capital can move through an economy. Cash App increases this velocity for the individual. By allowing for near-instantaneous movement of funds, it enables better cash flow management for small business owners and individuals alike. Its simplicity removes the friction often associated with financial transactions, making it an indispensable tool for daily liquidity.

Step-by-Step Logistics: How to Send and Receive Funds Safely

Navigating the interface of a financial app requires precision. One wrong digit can lead to a complicated recovery process. Understanding the core mechanics ensures that your capital reaches its intended destination without unnecessary stress.

Initiating Your First Transfer: The Core Mechanics

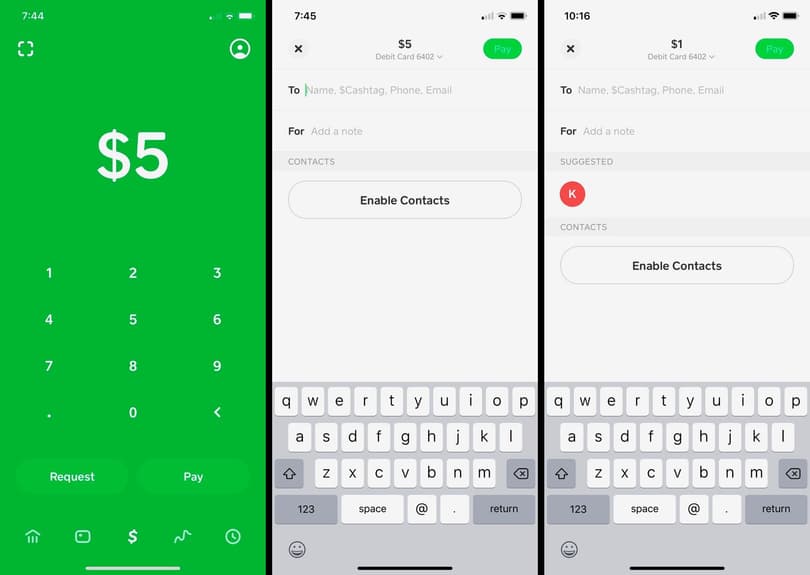

To send money, the process is designed to be intuitive. Upon opening the app, you are greeted with a numerical keypad. You enter the desired amount—for instance, $50.00—and tap the “Pay” button. At this stage, the app will prompt you to identify the recipient. You can select a contact from your phone’s synced list or manually enter their unique identifier.

Crucially, you must also select the source of the funds. Cash App allows you to draw from your existing Cash App balance, a linked debit card, or a linked bank account. From a financial planning perspective, using your existing balance is often the most efficient method, as it avoids additional steps in the reconciliation of your primary bank statements.

Understanding $Cashtags, Phone Numbers, and QR Codes

Identification is the most critical step in the transaction process. Cash App utilizes the “$Cashtag”—a unique username that acts as a financial address. When sending money, it is a “best practice” to double-check the recipient’s $Cashtag against their profile photo or verified name.

For face-to-face transactions, the app offers a QR code feature. This is the gold standard for accuracy; by scanning a friend’s code directly from their screen, you eliminate the risk of typographical errors. In the world of personal finance, eliminating human error is the first step toward securing your wealth.

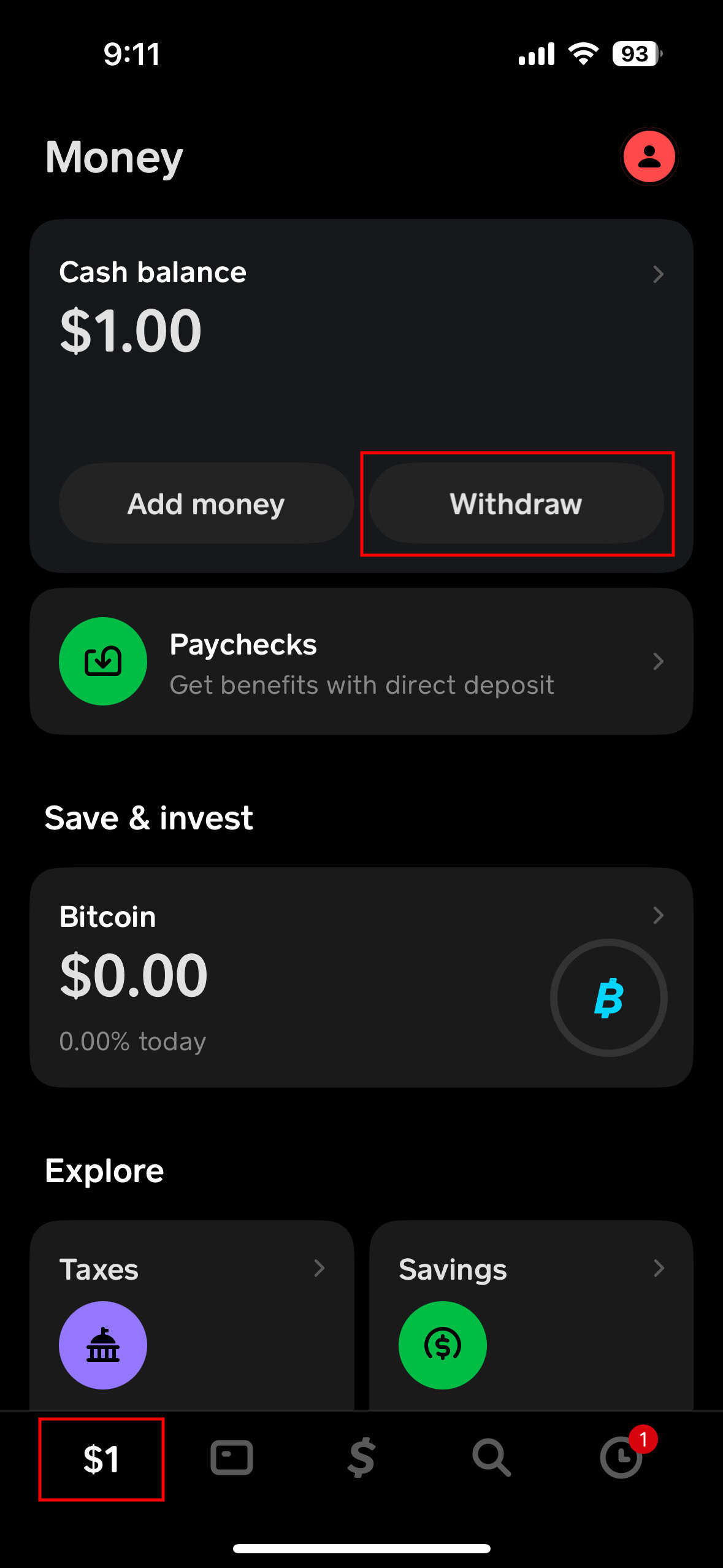

Navigating Instant Transfers vs. Standard Deposits

When you receive money, you face a strategic choice: Instant Transfer or Standard Deposit. This is where a savvy user must weigh the value of time against the cost of fees.

- Standard Deposits are free but typically take one to three business days to arrive in your linked bank account.

- Instant Transfers carry a small percentage fee (usually between 1.5% and 1.75%) but move the money to your debit card immediately.

From a financial management standpoint, unless you are facing a liquidity crisis, opting for the Standard Deposit is the more disciplined choice, as it preserves your total capital by avoiding unnecessary service charges.

Fees, Limits, and Optimization Strategies

To use any financial tool effectively, one must understand its constraints and costs. Cash App is transparent about its fee structure, but users must be proactive in managing their account limits to ensure the tool scales with their financial needs.

Decoding the Cost of Convenience: Transaction Fees

While peer-to-peer transfers from a linked bank account or debit card are generally free, there are specific scenarios where fees apply. For instance, sending money via a linked credit card incurs a 3% fee. In the context of personal finance, using a credit card for P2P transfers is generally discouraged because it essentially functions as a cash advance, which can also trigger high interest rates from your card issuer.

Furthermore, if you are using Cash App for business purposes, you should switch to a “Business Account.” While this provides more robust reporting for tax purposes, it also involves a transaction fee on incoming payments. Budgeting for these fees is essential for any freelancer or side-hustler utilizing the platform.

Managing Your Transaction Limits for Larger Financial Needs

New users often encounter “sending limits,” typically capped at $250 within a 7-day period and a receiving limit of $1,000 within a 30-day period. To optimize the app for more significant financial movements—such as paying rent or purchasing high-value items—you must complete the verification process. This involves providing your full legal name, date of birth, and the last four digits of your Social Security Number. Once verified, these limits are significantly increased, allowing the app to serve as a more robust primary financial vehicle.

Utilizing Cash App for Side Hustles and Business Transactions

For entrepreneurs, Cash App offers a “Business” profile setting. This is a powerful feature for those managing side illegal income or small service-based businesses. It allows you to accept payments without the recipient needing your private phone number or email, maintaining a professional boundary. Additionally, the platform provides basic tax documentation (like the 1099-K form when thresholds are met), which is vital for maintaining compliance with the IRS and ensuring your business finances are handled with professional rigor.

Security and Financial Safeguards in the Digital Age

As with any tool that touches your money, security is the paramount concern. Digital finance requires a proactive approach to safety to protect your hard-earned assets from the rising tide of cyber-fraud.

Implementing Advanced Security Protocols

Cash App provides several internal layers of protection. The “Security Lock” feature is perhaps the most important; it requires a PIN or biometric authentication (FaceID/TouchID) for every single transfer. In the realm of financial security, “friction” is your friend. By adding these extra seconds to the transaction process, you create a fail-safe against unauthorized access if your phone is ever lost or stolen.

Protecting Your Assets from Social Engineering and Scams

The greatest threat to your funds is often not a technical hack, but “social engineering.” Scammers frequently use “urgent” requests or “accidental” payment schemes to trick users into sending money. A cardinal rule of personal finance in the digital age is: Never send money to someone you do not know or for a “too good to be true” offer. Transactions on Cash App are usually instantaneous and irreversible. Unlike a credit card chargeback, once the money is sent, it is effectively gone unless the recipient chooses to refund it.

Best Practices for Dispute Resolution and Fraud Prevention

If you do suspect fraudulent activity, immediate action is required. You should use the app’s built-in support features to report the transaction and, more importantly, contact your linked bank or card issuer. Because Cash App is often linked to a primary bank account, ensuring that your external financial institutions are aware of the breach is the final line of defense in protecting your overall net worth.

Conclusion: Integrating Cash App into Your Wealth Strategy

Learning how to send money on Cash App is merely the entry point. To truly master the tool, one must view it as a cog in a larger financial machine. By utilizing its speed for daily transactions, its “Savings” feature for emergency funds, and its “Boosts” for automated discounts at retailers, you transform a simple app into a comprehensive financial assistant.

In a world where time is money, the ability to move capital securely, instantly, and efficiently is a vital skill. By following the logistical steps and security protocols outlined in this guide, you can navigate the modern digital economy with the confidence and sophistication of a seasoned financial professional.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.