Embarking on the journey of financial management can often feel overwhelming, yet few tools are as powerful and accessible as a well-crafted monthly budget. Far from being a restrictive exercise, a budget is your personalized financial roadmap, empowering you to understand where your money goes, make conscious spending decisions, and ultimately achieve your most ambitious financial aspirations. Whether you dream of buying a home, paying off debt, building an emergency fund, or simply gaining a clearer picture of your financial health, the fundamental step is learning how to construct and stick to a practical monthly budget. This guide will demystify the process, offering a professional, insightful, and engaging pathway to financial control and freedom.

Understanding the Foundation of Financial Control

Before diving into the mechanics of creating a budget, it’s crucial to grasp the underlying philosophy and undeniable benefits it offers. Budgeting is more than just numbers; it’s a mindset shift towards intentional spending and proactive saving.

Why Budgeting Matters More Than Ever

In an increasingly complex economic landscape, marked by inflation, fluctuating job markets, and the ever-present temptation of consumerism, personal financial management has never been more critical. A budget provides clarity, turning abstract financial anxieties into concrete, actionable plans. It offers several profound benefits:

- Revealing Your Spending Habits: Many people are surprised to discover where their money truly goes. A budget shines a light on often-overlooked expenditures, highlighting areas where cuts can be made or where money is being spent unintentionally.

- Achieving Financial Goals: Whether short-term (like a vacation) or long-term (like retirement), a budget transforms vague desires into achievable targets by allocating specific funds towards them.

- Reducing Financial Stress: A clear understanding of your financial situation, coupled with a plan, significantly reduces anxiety about money. You gain a sense of control and predictability.

- Building Wealth: By optimizing your spending and intentionally saving, a budget is the bedrock upon which wealth accumulation is built, allowing you to invest and grow your assets over time.

- Preparing for the Unexpected: An effective budget incorporates savings for emergencies, providing a crucial safety net against unforeseen expenses like medical bills or job loss.

Dispelling Budgeting Myths

The concept of budgeting often comes with a host of misconceptions that deter individuals from even starting. It’s essential to address these to approach budgeting with an open and empowered mindset:

- Myth: Budgeting is Restrictive and Takes Away All the Fun.

- Reality: While it requires discipline, a budget isn’t about deprivation. It’s about conscious choice. By understanding your financial limits, you can prioritize what truly brings you joy and cut back on expenses that don’t, ultimately allowing you to enjoy your chosen splurges guilt-free.

- Myth: Budgeting is Only for People Struggling Financially.

- Reality: From recent graduates to high-net-worth individuals, everyone can benefit from budgeting. It’s a tool for optimizing resources, regardless of income level. Wealthy individuals often budget meticulously to manage their investments and grow their assets strategically.

- Myth: Budgeting is Too Complicated and Time-Consuming.

- Reality: While the initial setup requires some effort, modern tools and simplified methods have made budgeting more accessible than ever. Once established, maintenance can take as little as 15-30 minutes per week. The complexity is often in the perception, not the process itself.

The Step-by-Step Guide to Crafting Your Monthly Budget

Creating a budget is a structured process that, when followed diligently, leads to profound financial insight and control. Here’s a detailed, step-by-step approach.

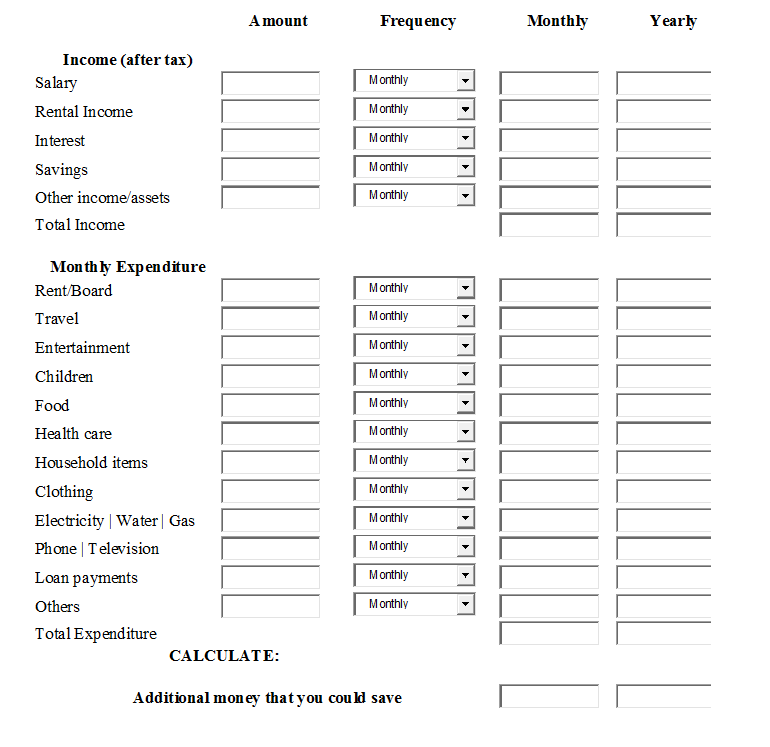

Step 1: Calculate Your Monthly Income

The very first step is to get a clear picture of all the money flowing into your accounts. This typically involves identifying your net (after-tax) income.

- Primary Income Sources: For most, this will be your salary or wages. If paid bi-weekly or weekly, you’ll need to multiply your pay by the number of paychecks you expect in the month (e.g., 2 or 4) or average it out.

- Secondary or Variable Income: Include any income from side hustles, freelance work, rental properties, alimony, child support, or investment dividends. If this income is irregular, it’s often wise to take a conservative average from the past few months or only budget with your fixed income and treat variable income as a bonus for savings or debt repayment.

- Total Monthly Income: Sum up all your reliable income sources. This figure represents the total amount you have available to allocate for the month.

Step 2: Track Your Spending Habits

This is often the most revealing part of the budgeting process. You need to understand precisely where your money has been going.

- Gather Financial Statements: Collect bank statements, credit card statements, and receipts from the past 1-3 months. This data will provide a historical record of your spending.

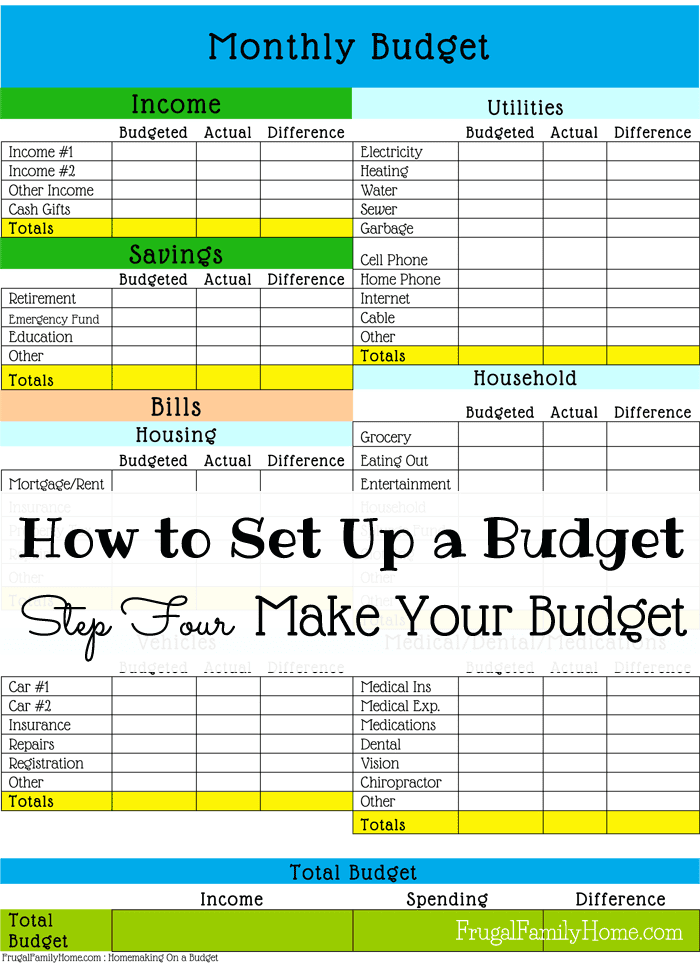

- Categorize Every Expense: Go through each transaction and assign it to a category. Common categories include housing (rent/mortgage), utilities, groceries, transportation, dining out, entertainment, subscriptions, personal care, and debt payments.

- Identify Fixed vs. Variable Expenses:

- Fixed Expenses: These are predictable amounts that remain relatively constant each month, like rent, mortgage payments, loan repayments, insurance premiums, and most subscription services.

- Variable Expenses: These fluctuate from month to month, such as groceries, dining out, entertainment, clothing, and transportation (gas, public transport). These are often the areas where the most significant adjustments can be made.

Step 3: Categorize and Allocate Funds

With your income and spending data in hand, it’s time to create your financial blueprint for the upcoming month.

- List All Expenses: Start by listing all your fixed expenses and their exact amounts.

- Estimate Variable Expenses: Based on your spending tracking, estimate realistic amounts for your variable expenses. Be honest with yourself; underestimating here will sabotage your budget.

- Allocate to Savings and Debt: Crucially, allocate funds for savings goals (emergency fund, down payment, retirement) and debt repayment before you’ve spent it. This is often referred to as “paying yourself first.”

- Balance Your Budget: The goal is for your total expenses (including savings and debt payments) to be less than or equal to your total monthly income.

- Income – Expenses = Zero or Positive. If you have a surplus, you can allocate more to savings, investments, or debt. If you have a deficit, you’ll need to identify areas to cut back. This is where the insights from tracking your variable expenses become invaluable.

Step 4: Set Realistic Financial Goals

A budget is a tool, and its effectiveness is amplified when it’s aligned with clear financial goals.

- Define Your Goals: What do you want your money to do for you? Examples include building a $1,000 emergency fund, paying off a credit card, saving for a down payment, or funding a specific investment.

- Make Them SMART:

- Specific: Clearly defined (e.g., “save $5,000 for a car down payment”).

- Measurable: Quantifiable (e.g., “$400 per month”).

- Achievable: Realistic given your income and expenses.

- Relevant: Aligned with your values and broader financial plan.

- Time-bound: With a deadline (e.g., “by December 31st next year”).

- Integrate into Your Budget: Allocate specific line items in your budget for these goals. Treat savings goals like a non-negotiable expense.

Step 5: Monitor, Review, and Adjust Regularly

A budget is not a static document; it’s a living, breathing financial plan that requires ongoing attention.

- Track Throughout the Month: Regularly log your spending and compare it against your budgeted categories. Many budgeting apps automate this by linking to your bank accounts.

- Review Monthly: At the end of each month (or the beginning of the next), sit down and review your budget.

- Did you stick to your limits?

- Where did you overspend, and why?

- Where did you underspend?

- Have your income or fixed expenses changed?

- Adjust as Needed: Based on your review, make necessary adjustments for the upcoming month. Life happens, and your budget needs to be flexible enough to accommodate changes in income, expenses, and priorities. This iterative process is key to long-term budgeting success.

Tools and Strategies for Budgeting Success

While the principles of budgeting remain constant, the methods and tools you employ can significantly impact your experience and effectiveness.

Digital Budgeting Tools and Apps

For many, technology offers the most convenient and powerful way to manage finances.

- Automated Tracking: Many apps link directly to your bank accounts and credit cards, automatically categorizing transactions and providing real-time updates on your spending.

- Visualization and Reporting: These tools often come with intuitive dashboards, graphs, and reports that make it easy to visualize your financial health, track progress towards goals, and identify spending trends.

- Examples:

- Mint: A popular free tool that connects to your accounts, tracks spending, and provides budget templates.

- YNAB (You Need A Budget): A paid app that focuses on “giving every dollar a job” through zero-based budgeting, ideal for those who want a highly disciplined approach.

- Personal Capital: Combines budgeting with investment tracking, offering a holistic view of your financial net worth.

- Spreadsheets (Google Sheets/Excel): For those who prefer a DIY approach, customizable spreadsheets offer immense flexibility and control, though they require manual data entry.

Traditional Methods: Pen, Paper, and Envelopes

For individuals who prefer a more tangible, hands-on approach, traditional methods remain highly effective.

- Notebook and Ledger: A simple notebook or ledger can be used to manually record all income and expenses, offering a clear, physical record of your financial movements.

- The Envelope System: This method is particularly useful for controlling variable spending categories (like groceries, entertainment, or dining out).

- At the beginning of the month, you withdraw cash for these categories and place it into labeled envelopes.

- When you spend, you take money only from the relevant envelope. Once an envelope is empty, you stop spending in that category until the next month. This system forces a strict adherence to spending limits.

Popular Budgeting Methodologies Explained

Beyond the tools, various budgeting philosophies can guide your approach.

- The 50/30/20 Rule:

- 50% Needs: Allocate half of your after-tax income to essential expenses like housing, utilities, groceries, transportation, and minimum loan payments.

- 30% Wants: Dedicate 30% to discretionary spending that improves your quality of life but isn’t strictly essential, such as dining out, entertainment, hobbies, and shopping.

- 20% Savings & Debt Repayment: The remaining 20% goes towards financial goals like an emergency fund, retirement savings, and extra payments on debt (beyond the minimums). This rule offers a straightforward framework for balancing priorities.

- Zero-Based Budgeting:

- Every dollar of your income is assigned a “job” (spending, saving, debt repayment) until your income minus your expenses equals zero.

- This method ensures that no money is left unaccounted for and forces intentional decision-making for every single dollar, making it highly effective for maximizing financial control.

- The Envelope System (as detailed above): While also a tool, it’s a budgeting philosophy that promotes strict cash-based spending for variable categories, preventing overspending by making the depletion of funds physically evident.

Overcoming Common Budgeting Challenges

Even with the best intentions and tools, challenges can arise. Anticipating and preparing for them is key to long-term success.

Dealing with Irregular Income

For freelancers, commission-based workers, or those with seasonal jobs, irregular income can make budgeting feel impossible.

- Average Income Over Time: Look at your income over the past 6-12 months to determine a realistic monthly average. Base your budget on this conservative average.

- Buffer Account: Create a separate savings account to hold excess income during high-earning months. This “buffer” can then be drawn upon during lower-earning months to ensure a stable monthly income for your budget.

- Prioritize Fixed Expenses: Ensure your fixed, essential expenses are covered first, even in lean months, relying on your buffer for variable spending.

Staying Motivated and Disciplined

Budgeting is a marathon, not a sprint. Maintaining motivation is crucial.

- Celebrate Small Wins: Acknowledging progress, no matter how minor, reinforces positive behavior. Did you stick to your grocery budget for a month? Treat yourself to a small, non-budget-breaking reward.

- Find an Accountability Partner: Discussing your financial goals and progress with a trusted friend, family member, or financial mentor can provide external motivation and support.

- Automate Savings: Set up automatic transfers from your checking account to your savings or investment accounts immediately after payday. “Out of sight, out of mind” can be a powerful motivator for saving.

- Focus on Your “Why”: Regularly remind yourself of the larger financial goals your budget is helping you achieve. Visualizing your dream vacation or debt-free life can be incredibly powerful.

Adapting to Unexpected Expenses

Life is unpredictable, and even the most meticulously planned budget can be derailed by unforeseen costs.

- The Emergency Fund is Paramount: This is not merely a “nice to have”; it’s a non-negotiable component of a robust financial plan. Aim for 3-6 months’ worth of living expenses in a separate, easily accessible savings account.

- Build a “Buffer” Category: In your budget, include a small line item for miscellaneous or “unexpected” expenses. This allows for minor surprises without derailing the entire budget.

- Prioritize and Adjust: If a large, unexpected expense arises, evaluate your budget to see where you can temporarily cut back (e.g., reduce entertainment, pause extra debt payments) to cover the cost without incurring new debt.

Beyond the Monthly Budget: Long-Term Financial Health

While a monthly budget is the cornerstone, it’s also a stepping stone to broader financial well-being. Integrating your budget into a larger financial strategy ensures sustained prosperity.

Building an Emergency Fund

As mentioned, an emergency fund is critical. It acts as a financial shock absorber, preventing minor setbacks from escalating into major crises that could force you into debt. Your budget is the vehicle through which you consistently contribute to this vital safety net. Start small, even $25-$50 a month, and steadily increase contributions until you reach your target.

Tackling Debt Strategically

For many, a significant portion of their budget goes towards debt repayment. A budget allows you to see this clearly and develop a strategic plan.

- Debt Snowball: Pay off the smallest debt first to gain momentum and motivation, then roll those payments into the next smallest debt.

- Debt Avalanche: Focus on paying off debts with the highest interest rates first, which saves you more money over time.

- Your budget will help you identify extra funds to accelerate these repayment strategies, freeing up future income for savings and investments.

Planning for Future Investments and Retirement

Once your emergency fund is robust and high-interest debt is under control, your budget becomes a powerful tool for building long-term wealth.

- Automate Investment Contributions: Just like savings, set up automatic transfers from your checking account to your investment accounts (e.g., 401(k), IRA, brokerage account).

- Factor into Your Budget: Allocate a specific portion of your income each month towards investments. This ensures consistent growth and prevents you from spending money that could be compounding for your future.

- Review Investment Goals: Periodically, perhaps annually, review your investment goals alongside your budget to ensure they are still aligned with your financial trajectory.

In conclusion, making a monthly budget is not about living a life of scarcity; it’s about embracing a life of intention, clarity, and control. It’s the most effective personal finance tool for understanding your money, aligning your spending with your values, and systematically progressing towards your financial dreams. By calculating your income, tracking expenses, allocating funds strategically, setting clear goals, and consistently reviewing your plan, you’ll transform your financial landscape from one of uncertainty to one of empowered prosperity. Start today, and witness the profound impact a well-managed monthly budget can have on your life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.