For many Americans, the arrival of tax season brings a mixture of anticipation and anxiety. While some look forward to a significant refund, others harbor a nagging fear that they might actually owe money to the federal government. Understanding your tax position is not merely a matter of annual compliance; it is a fundamental pillar of personal finance management. Knowing whether you owe the Internal Revenue Service (IRS) allows you to plan your cash flow, avoid mounting interest penalties, and maintain a healthy relationship with your financial obligations.

The complexity of the U.S. tax code means that liability can often sneak up on even the most diligent taxpayers. From changes in side hustle income to shifts in investment portfolios, various factors can tip the scales from a refund to a balance due. This guide provides an in-depth exploration of how to identify your tax status, the tools available to verify your balance, and the strategic steps to take if you find yourself in debt to the Treasury.

Identifying the Red Flags: Common Signs You Might Have a Tax Balance

The first step in managing tax liability is recognizing the signs that you might owe money. Often, the IRS provides direct communication, but there are also internal financial indicators that can alert you to a potential balance before a formal notice even arrives in your mailbox.

Understanding IRS Notices and Correspondence

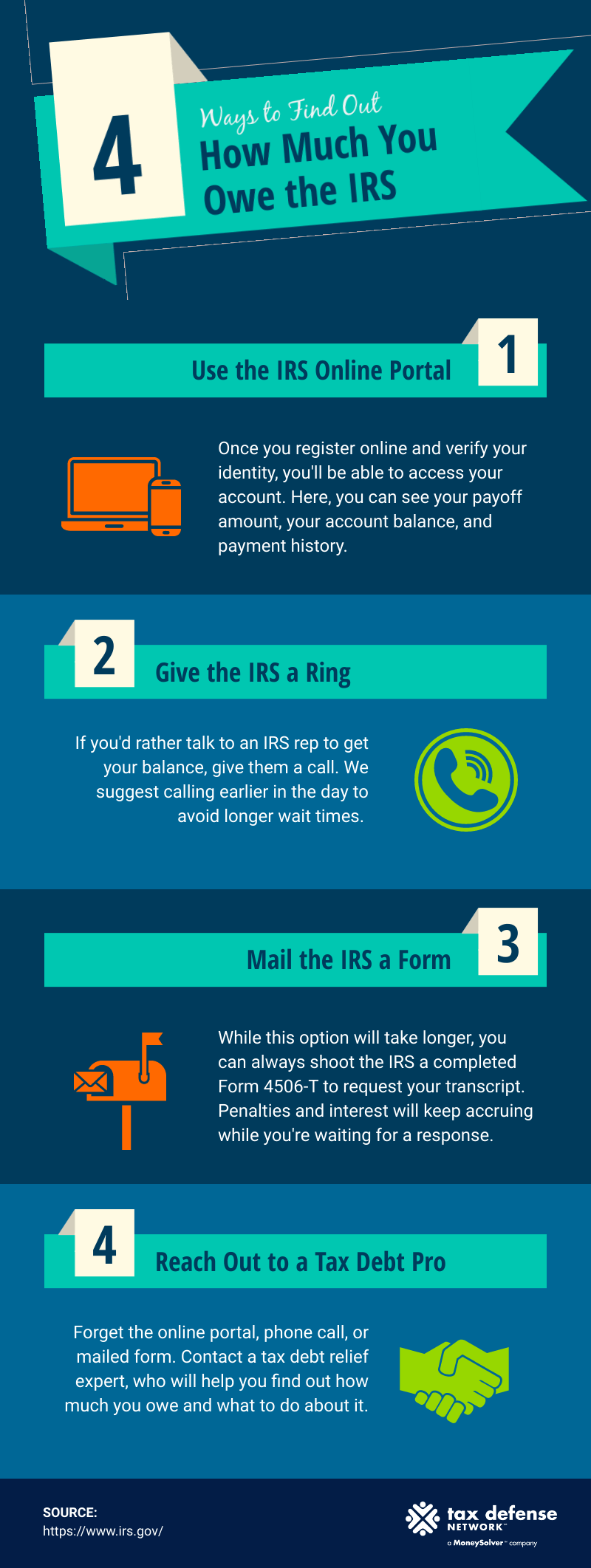

The most definitive way to know if you owe the IRS is through official correspondence. The IRS communicates primarily via physical mail sent through the United States Postal Service. If you receive a letter, such as a Notice CP14 (Balance Due) or a CP2000 (Notice of Underreported Income), it is a clear signal that the agency’s records do not match your filings or that a payment was missed. It is vital to read these documents carefully, as they outline the specific tax year in question, the amount owed, and the deadline for response. Ignoring these letters is a critical financial mistake, as interest and penalties begin accruing from the original due date of the return.

Tracking Your Tax Withholding and Estimated Payments

For those who are traditionally employed (W-2 earners), tax liability often arises when withholdings are set too low. If you haven’t updated your Form W-4 in several years or if you have recently experienced a significant life event—such as marriage, the birth of a child, or a spouse returning to the workforce—your employer may not be taking out enough tax. Similarly, for entrepreneurs and freelancers, failing to make sufficient quarterly estimated tax payments is the leading cause of a surprise year-end bill. If your income has increased significantly but your estimated payments have remained stagnant, you are likely looking at a balance due.

Changes in Life Status and Tax Bracket Shifts

Financial growth is generally positive, but it often comes with increased tax responsibilities. If you moved into a higher tax bracket due to a promotion or a successful business venture, the percentage of your income owed to the government increases. Furthermore, the “phase-out” of certain tax credits, such as the Child Tax Credit or the Earned Income Tax Credit (EITC), can result in a higher tax bill than in previous years. Monitoring your Adjusted Gross Income (AGI) throughout the year is a proactive way to anticipate these shifts.

Leveraging Digital Financial Tools to Verify Your Tax Status

In the modern financial landscape, you no longer have to wait for a paper letter to arrive to understand your tax standing. The IRS has significantly upgraded its digital infrastructure, allowing taxpayers to access real-time information regarding their accounts.

Utilizing the IRS Online Account Feature

The most efficient tool at your disposal is the “Your Online Account” portal on the official IRS website. By creating an account (which typically requires identity verification through services like ID.me), you can view the total amount you owe, including a breakdown by tax year. This dashboard also displays your payment history, any scheduled payments, and digital copies of select notices. For anyone serious about their personal finance, checking this portal at least twice a year—once during tax season and once in the fall—is a best practice to ensure no surprises are lurking.

Requesting Tax Transcripts for Historical Accuracy

If you are unsure why you owe a balance or if you suspect an error in your previous filings, requesting a tax transcript is a powerful diagnostic step. There are several types of transcripts, but the “Tax Account Transcript” is particularly useful for identifying adjustments made by the IRS after you filed your return. This document shows your original return data plus any subsequent assessments or payments. Reviewing your transcripts can help you reconcile your personal accounting with the IRS’s records, providing a clear path to correcting discrepancies.

Checking the “Where’s My Refund?” and Payment Status Tools

While primarily used for those expecting money back, the “Where’s My Refund?” tool and the “Direct Pay” status portals can offer clues about your account. If a refund you were expecting is “offset,” it means the IRS has applied that money toward an existing debt, which could include back taxes, overdue child support, or federal student loan defaults. Following the trail of an offset refund is a common way taxpayers discover they had an outstanding balance they were previously unaware of.

The Math Behind the Debt: Why You Might Owe More Than Expected

Understanding the “why” behind your tax debt is essential for future planning. Tax liability is rarely arbitrary; it is almost always the result of specific financial activities that were not fully covered by prepayments or withholdings.

Unreported Income and Form 1099 Discrepancies

The IRS receives copies of every 1099 form issued to you. If you work as a contractor or have a side hustle, and you forget to report income from a specific client, the IRS’s automated systems will eventually flag the discrepancy. This “matching” process often results in a notice several months or even years after the return was filed. In the world of online income and the “gig economy,” keeping meticulous records of every 1099-K, 1099-NEC, and 1099-MISC is non-negotiable for avoiding unexpected debt.

The Impact of Capital Gains and Investment Income

For investors, the sale of assets such as stocks, real estate, or cryptocurrency can trigger significant tax events. If you sold an asset for a profit (capital gain) in a non-retirement brokerage account, you owe taxes on that gain. Many novice investors fail to set aside a portion of their profits for the IRS, leading to a “liquidity crunch” come April. Furthermore, high-income earners may be subject to the Net Investment Income Tax (NIIT), an additional 3.8% tax that can catch many by surprise if they haven’t factored it into their annual projections.

Business Expenses and the Self-Employment Tax Trap

Small business owners and freelancers are responsible for both the employer and employee portions of Social Security and Medicare taxes, commonly known as the self-employment tax. This totals approximately 15.3% of net earnings. A common mistake is focusing only on income tax and forgetting this additional self-employment obligation. Additionally, if the IRS audits your return and disallows certain business deductions, your taxable income rises retroactively, resulting in a new balance due plus interest.

Proactive Management Strategies for Tax Liability

Discovering that you owe the IRS is not the end of the world, but it does require immediate and strategic action. The IRS is often called the “world’s most powerful collection agency,” but it also offers several avenues for taxpayers to resolve their debt reasonably.

Adjusting Your W-4 for Future Compliance

If you find that you consistently owe money every year, the most effective “set it and forget it” solution is to update your Form W-4 with your employer. You can request that an additional specific dollar amount be withheld from every paycheck. This micro-adjustment ensures that you are paying your liability incrementally throughout the year, rather than facing a massive lump sum in April. For those with complex income streams, using the IRS Tax Withholding Estimator tool can provide the exact figures needed to reach a “zero balance” or a small refund.

Setting Up Payment Plans and Installment Agreements

If you cannot pay your tax bill in full immediately, the IRS offers several payment options. A “Short-term Payment Plan” gives you up to 180 days to pay the balance in full, often with reduced penalties. For larger debts that require more time, a “Long-term Payment Plan” (Installment Agreement) allows you to make monthly payments for up to 72 months. While interest still accrues, being on a formal plan protects you from more aggressive collection actions like wage garnishments or bank levies.

![]()

The Importance of Working with a Certified Tax Professional

When tax debt becomes significant—typically over $10,000—or involves complex business issues, seeking professional help is a wise investment. Certified Public Accountants (CPAs) and Enrolled Agents (EAs) can represent you before the IRS. They can help you navigate advanced options like an “Offer in Compromise” (where you settle the debt for less than you owe) or “Currently Not Collectible” status if you are experiencing severe financial hardship. A professional can also review your past returns to ensure you haven’t missed deductions that could lower the amount you owe.

In conclusion, knowing if you owe the IRS is a matter of staying informed, utilizing digital tools, and maintaining a proactive stance toward your financial health. By understanding the triggers of tax liability and the methods for verification, you can transform a potentially stressful situation into a manageable part of your broader financial strategy. Remember, the IRS values communication and compliance over perfection; taking the first step to identify and address your balance is the most important move you can make.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.