Navigating the complexities of federal taxes can be daunting, and for many, the question of whether they owe the IRS money looms large. Understanding your tax obligations and knowing how to verify your status is crucial for financial peace of mind and avoiding potential penalties. The U.S. tax system operates on a pay-as-you-go principle, meaning taxpayers are expected to pay taxes throughout the year as they earn income. If these payments—either through employer withholdings or estimated tax payments—don’t sufficiently cover your annual tax liability, you will likely owe the IRS money when you file your return.

Understanding Your Tax Obligations and the Pay-As-You-Go System

The foundation of the U.S. tax system rests on the “pay-as-you-go” philosophy. This means that instead of paying a lump sum once a year, taxpayers are expected to remit taxes throughout the year as income is earned. For most employed individuals, this happens automatically through income tax withholding from their paychecks, managed by their employer based on the W-4 form they submit. Each pay period, a portion of their gross earnings is sent to the IRS, pre-paying their tax bill.

However, for self-employed individuals, gig workers, those with significant investment income, rental income, or other income not subject to withholding, this responsibility shifts. They are typically required to make estimated tax payments quarterly, usually on April 15, June 15, September 15, and January 15 of the following year. These payments are their way of fulfilling the pay-as-you-go requirement.

Taxable Income Sources

Your total tax liability is determined by your taxable income, which can come from various sources. Beyond standard wages and salaries (W-2 income), this includes income from self-employment (Form 1099-NEC), interest (Form 1099-INT), dividends (Form 1099-DIV), capital gains from selling investments (Form 1099-B), rental income, royalties, and even certain types of gambling winnings. Each of these income streams contributes to your overall tax burden, and if taxes aren’t adequately withheld or paid on them, it increases the likelihood of owing money.

Deductions vs. Credits

It’s important to differentiate between tax deductions and tax credits, as both impact your final tax bill but in different ways. Deductions reduce your taxable income, meaning you pay tax on a smaller amount. For example, a $1,000 deduction means you’ll pay tax on $1,000 less income. Common deductions include contributions to traditional IRAs, student loan interest, and certain itemized deductions like mortgage interest or state and local taxes. Credits, on the other hand, directly reduce the amount of tax you owe, dollar for dollar. A $1,000 tax credit means your tax bill is reduced by $1,000. Examples include the Child Tax Credit, Earned Income Tax Credit, or education credits. Miscalculating or overlooking eligible deductions and credits can lead to an artificially higher tax liability, potentially making it seem like you owe more than you truly do, or conversely, claiming too many without proper qualification could lead to an underpayment that requires adjustment later.

Key Indicators and Warning Signs

While the exact calculation of your tax liability occurs when you file your return, several situations throughout the year can serve as strong indicators that you might owe the IRS money. Recognizing these early can help you adjust your strategy and avoid surprises.

Changes in Income or Employment

A significant increase in your income, whether through a promotion, a substantial raise, or taking on a high-paying second job, can push you into a higher tax bracket or simply result in your existing withholdings being insufficient. Similarly, if you transition from traditional employment to self-employment, where no taxes are withheld automatically, you become solely responsible for making estimated tax payments. Failing to adjust your W-4 form with your employer after a raise or neglecting to make estimated payments as a freelancer are common reasons for underpayment.

Significant Life Events

Major life changes often have significant tax implications. Getting married can alter your filing status (usually to “Married Filing Jointly”), potentially moving you into a different tax bracket, or changing your eligibility for certain credits and deductions. Divorce also has complex tax ramifications, especially concerning alimony, child support, and asset division. The birth of a child brings new credits (like the Child Tax Credit) but might also warrant a review of your overall tax strategy. Even seemingly simple events, like buying or selling a home, can introduce new deductions or taxable gains that need to be accounted for.

Untaxed Income

Not all income is subject to automatic withholding. If you engage in freelance work, consulting, or receive income from the gig economy, these earnings are typically paid without tax deductions. Similarly, income from investments such as stock dividends, capital gains from selling assets (including cryptocurrency), or even significant gambling winnings are usually paid out gross, meaning you’re responsible for the taxes. Failing to track these untaxed income sources and make corresponding estimated tax payments is a primary cause of owing money at tax time.

Under-Withholding from Paychecks

One of the most common reasons individuals owe money is incorrect withholding from their paychecks. This usually stems from filling out your Form W-4 incorrectly. Claiming too many allowances in the past (before the W-4 was redesigned in 2020) or, more recently, failing to account for multiple jobs, significant deductions, or other income sources can lead to less tax being withheld than necessary. Regularly reviewing your pay stubs to see how much federal tax is being withheld and using the IRS Tax Withholding Estimator tool can help identify and correct under-withholding issues.

Incorrect Estimated Tax Payments

For those required to pay estimated taxes (the self-employed, independent contractors, etc.), underestimating your annual income or simply forgetting to make one or more of the quarterly payments can quickly lead to an underpayment. The IRS typically requires taxpayers to pay at least 90% of their current year’s tax liability or 100% of their prior year’s tax liability (110% for high-income earners) through withholdings or estimated payments to avoid penalties. Missing this threshold can result in a balance due and potential penalties.

Proactive Steps: Monitoring Your Tax Situation

Being proactive about your tax situation can significantly reduce the chances of owing the IRS money and help you avoid unnecessary stress. By regularly monitoring your income and withholdings, you can make adjustments throughout the year as needed.

Reviewing Your Pay Stubs and W-4

Your pay stub is a valuable tool for monitoring your federal income tax withholding. Regularly checking the amount withheld for federal tax allows you to gauge whether enough is being set aside. If you notice a discrepancy or have experienced a change in your financial situation (e.g., marriage, new job, significant raise), it’s a good time to revisit your Form W-4 with your employer. The IRS Tax Withholding Estimator tool (available on IRS.gov) is an excellent resource that provides a personalized recommendation for your W-4 based on your current income, deductions, and credits. Using this tool once or twice a year can prevent both over- and under-withholding.

Tracking Income and Expenses

For anyone with income not subject to automatic withholding—such as freelancers, small business owners, or those with rental properties—meticulous record-keeping of all income and expenses is paramount. Software like QuickBooks, FreshBooks, or even simple spreadsheets can help you track earnings and deductible expenses in real-time. This provides an accurate picture of your net income, which is crucial for calculating estimated tax payments and preventing an unexpected tax bill. Keeping receipts and digital records organized throughout the year also simplifies tax preparation.

Utilizing Tax Software or Professional Guidance

Modern tax software solutions (e.g., TurboTax, H&R Block, TaxAct) are not just for filing. Many offer features that allow you to input your financial data throughout the year to get a running estimate of your tax liability. This “mock tax return” approach can highlight potential shortfalls early on. For more complex financial situations, consulting a tax professional (such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA)) is invaluable. They can provide personalized tax planning advice, help you project your tax liability, ensure you’re taking advantage of all eligible deductions and credits, and make recommendations for adjusting your withholdings or estimated payments.

Annual Tax Projections

Even if you don’t have complex finances, performing a “tax projection” around mid-year (e.g., in July or August) can be a smart move. This involves estimating your total income, deductions, and credits for the entire year and comparing it to the amount of tax you’ve already had withheld or paid through estimated taxes. This projection allows you to identify any potential gap between what you’ve paid and what you’re likely to owe, giving you several months to adjust your W-4, make additional estimated payments, or plan for a balance due, thus avoiding end-of-year surprises.

Official IRS Communications and Resources

The most definitive way to know if you owe the IRS money, or if they believe you do, is through official communication channels and their online resources. It is critical to distinguish legitimate IRS communications from scams.

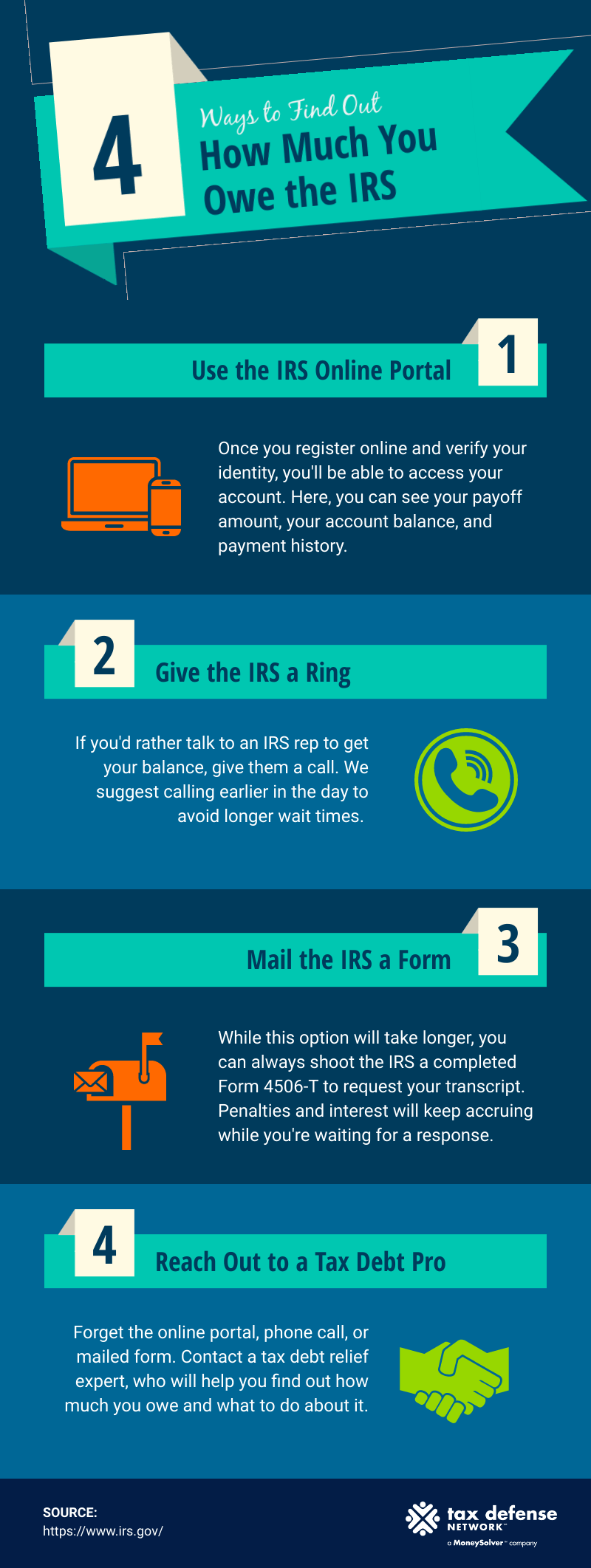

Setting Up an IRS Online Account

The IRS provides an invaluable tool called “IRS Online Account” accessible via IRS.gov/accounts. By creating and logging into your secure online account, you can:

- View your current tax balance, including any amounts owed, interest, and penalties.

- Access your tax records, including prior tax returns, payment history, and information from income documents like W-2s and 1099s.

- Make payments directly from your bank account or apply for a payment plan.

- Review notices sent by the IRS.

This account is the most direct and reliable way to ascertain your official tax balance with the agency.

IRS Tax Transcripts

Another useful resource available through your IRS Online Account or by mail is an IRS Tax Transcript. An “Account Transcript” specifically provides a summary of your tax return, payment history, and any balance due for a particular tax year. It can help you reconcile your records with those of the IRS and confirm if there’s an outstanding balance.

Notice of Underpayment/Balance Due

The IRS will always notify you by physical mail if they believe you owe money or if there’s an issue with your tax return. Common notices include:

- CP14: This notice informs you that you have a balance due for a specific tax year.

- CP2000: This notice (often called an “underreporter inquiry”) indicates that the income reported on your tax return doesn’t match the income reported to the IRS by third parties (like employers or financial institutions). This often means you underreported income and, as a result, owe more tax.

- Notices about Estimated Tax Underpayment: If you didn’t pay enough estimated tax throughout the year, you might receive a notice about penalties.

It is crucial to understand that the IRS never initiates contact about a balance due via phone calls, emails, or social media. Any such contact is a scam. Always verify the legitimacy of any IRS letter by comparing it to official samples on IRS.gov or by contacting the IRS directly using their official phone numbers.

Filing Your Tax Return

Ultimately, the most comprehensive method for determining if you owe money is to prepare and file your annual tax return (Form 1040). Whether you use tax software, a tax professional, or the free fillable forms on IRS.gov, the process of completing your return will calculate your total tax liability, subtract any payments already made (through withholding or estimated taxes), and clearly show whether you are due a refund or if you owe a balance. Filing your return, even if you can’t pay the full amount, is vital as it avoids the potentially higher “failure to file” penalty.

What to Do If You Owe

Discovering you owe the IRS can be unsettling, but having a plan of action is crucial. Ignoring the debt will only lead to greater penalties and interest.

Verify the Amount

The first step is always to verify the amount owed. If you used tax software or a tax professional to prepare your return, double-check their calculations. If you received a notice from the IRS, review it carefully. Compare the IRS’s figures to your own records. If you believe there’s a discrepancy or an error, gather your documentation and contact the IRS for clarification, or consult with a tax professional who can help you respond appropriately.

Payment Options

The IRS offers several convenient ways to pay a tax balance:

- IRS Direct Pay: Pay directly from your checking or savings account for free.

- Debit Card, Credit Card, or Digital Wallet: Payments can be made via third-party processors, though these usually involve a processing fee.

- Electronic Federal Tax Payment System (EFTPS): A free service from the Treasury Department allowing individuals and businesses to make federal tax payments electronically.

- Check or Money Order: Mailed with a payment voucher (Form 1040-V) to the IRS.

Paying your balance in full by the tax deadline (typically April 15) is the best way to avoid interest and penalties.

Payment Plans

If you cannot pay the full amount by the due date, it’s essential to communicate with the IRS and explore payment options to avoid greater penalties.

- Short-Term Payment Plan: You may be granted up to 180 days to pay your tax liability in full, though interest and penalties still apply.

- Offer in Compromise (OIC): For taxpayers experiencing significant financial hardship, an OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. The IRS evaluates your ability to pay, income, expenses, and asset equity.

- Installment Agreement: If you can’t pay your taxes in full within 180 days, you might be able to request an installment agreement. This allows you to make monthly payments for up to 72 months. Interest and late-payment penalties still apply but are often lower than if you do not establish a plan. You can typically set this up online via your IRS Online Account.

Understanding Penalties and Interest

The IRS imposes penalties for failure to file on time and failure to pay on time.

- Failure-to-File Penalty: This is typically 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid tax.

- Failure-to-Pay Penalty: This is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, also capped at 25%.

Interest is also charged on underpayments and accrues daily from the payment due date until the balance is paid in full. The interest rate can change quarterly. Filing your return on time, even if you can’t pay, can help you avoid the much steeper failure-to-file penalty.

Seeking Professional Help

If you’re overwhelmed by a tax bill or notice from the IRS, or if you need assistance setting up a payment plan or negotiating an Offer in Compromise, a qualified tax professional (CPA or Enrolled Agent) can provide invaluable assistance. They can communicate with the IRS on your behalf, help you understand your options, and work towards the best possible resolution for your financial situation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.