Car insurance is often viewed as a legal hurdle—a necessary box to check before driving off the lot. However, from a personal finance perspective, securing the right auto policy is one of the most critical components of a robust wealth-management strategy. It is not merely about staying compliant with state laws; it is about risk mitigation and the preservation of your net worth. One significant accident without adequate coverage can lead to financial ruin, liquidating years of savings and future earnings.

Getting car insurance requires a blend of market research, financial self-assessment, and an understanding of how insurance products integrate into your overall budget. This guide explores the strategic steps to acquiring car insurance, focusing on maximizing value while ensuring your financial foundations remain unshakable.

Understanding the Financial Fundamentals of Auto Insurance

Before you begin soliciting quotes, you must understand what you are actually buying. In the world of finance, insurance is a contract where you transfer the risk of a catastrophic financial loss to a third party in exchange for a fee (the premium).

The Importance of Liability Coverage

Liability coverage is the bedrock of any policy. It protects you from the financial fallout if you are found legally responsible for injury to others or damage to their property. From a money management perspective, “state minimums” are rarely sufficient. If you have significant assets—such as a home, investments, or a high-earning career—you are a target for litigation following an accident. Financial experts typically recommend liability limits that meet or exceed your total net worth to ensure that a single mistake on the road doesn’t result in a court-ordered liquidation of your portfolio.

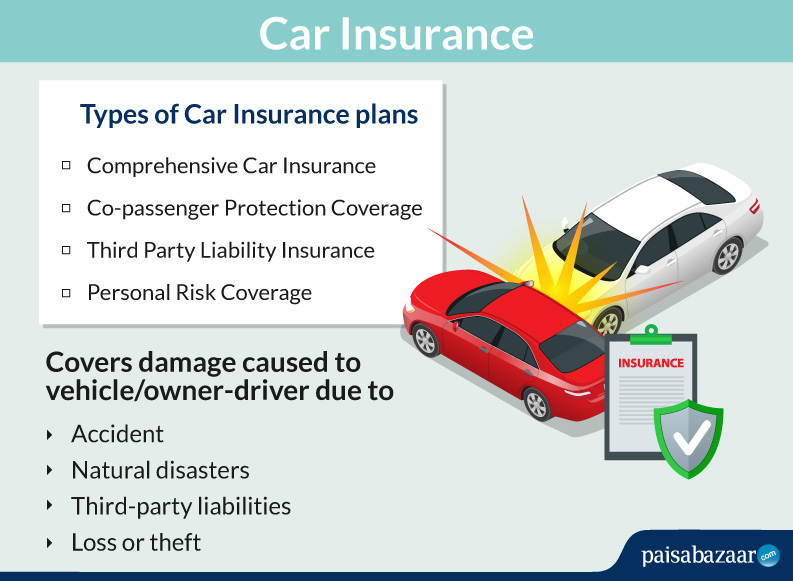

Comprehensive vs. Collision: Assessing Risk and Value

While liability protects others, collision and comprehensive coverage protect your own vehicle. Collision pays for repairs after an accident, regardless of fault, while comprehensive covers non-collision events like theft, fire, or natural disasters.

The financial decision to carry these coverages should be based on the “replacement cost” of the vehicle versus the “premium cost” over time. If you are driving an older vehicle with a low market value, the premiums paid over three years might exceed the potential payout in the event of a total loss. In such cases, “self-insuring” (dropping these coverages and keeping an emergency fund instead) may be the more fiscally responsible choice.

Deductibles and Premium Relationships

The deductible is the amount you pay out of pocket before your insurance kicks in. In financial terms, choosing a deductible is a balancing act between liquidity and cash flow. A higher deductible (e.g., $1,000) will lower your monthly premium, freeing up cash flow for investments or other expenses. However, you must ensure that you have the liquidity—specifically in an emergency fund—to cover that $1,000 at a moment’s notice. Lowering your deductible increases your fixed monthly costs but reduces the volatility of your expenses in the event of a claim.

Navigating the Market: How to Compare Quotes for Maximum ROI

Once you understand the product, the next step is procurement. The insurance market is highly fragmented, and prices for the exact same coverage can vary by hundreds of dollars between providers.

The Power of Independent Agents vs. Direct Carriers

There are two primary ways to shop: through direct carriers (like Geico or Progressive) or through independent insurance agents. Direct carriers offer convenience and often lower overhead, which can translate to lower premiums. However, independent agents have access to a variety of “behind-the-scenes” markets and can compare multiple companies simultaneously. For those with complex financial profiles—such as multiple properties or a mix of business and personal vehicle use—an agent can provide a bespoke financial analysis that an algorithm might miss.

Leveraging Bundling and Multi-Policy Discounts

One of the most effective ways to optimize your insurance spend is through “bundling.” Most insurers offer significant discounts if you carry both your auto and homeowners (or renters) insurance with them. This is a classic example of a “volume discount” in the financial services sector. By consolidating your risk under one umbrella, you reduce the administrative cost for the insurer, and they pass those savings on to you. Always calculate the total cost of bundled policies versus separate policies to ensure the discount is truly providing a net gain.

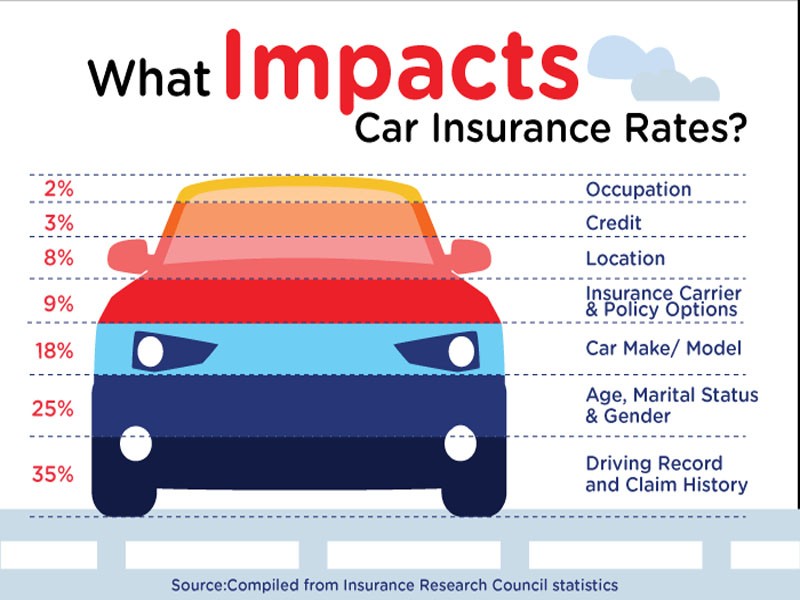

The Impact of Credit Scores on Your Premium

In many regions, insurance companies use a “credit-based insurance score” to determine your premium. From a financial health perspective, this highlights the interconnectedness of your money habits. A high credit score suggests to underwriters that you are a low-risk individual, resulting in lower premiums. If you are looking to get car insurance in the near future, improving your credit utilization and ensuring on-time payments can be just as effective at lowering your insurance costs as shopping around.

The Step-by-Step Process of Securing Your Policy

Securing the policy is a formal financial transaction that requires precision and documentation.

Gathering Necessary Financial and Vehicle Documentation

To get an accurate quote and formalize the contract, you will need several pieces of information:

- Vehicle Identification Number (VIN): This determines the safety rating and repair costs of the car.

- Driver’s License and Driving History: Your “risk profile” as a driver.

- Current Policy Declarations Page: If you are switching carriers, this helps the new insurer match or improve upon your current coverage.

- Banking Information: Most insurers offer discounts for “EFT” (Electronic Funds Transfer) or paying the full six-month/annual premium upfront.

Evaluating Your Net Worth to Determine Coverage Limits

As you fill out the application, you will be asked to select your limits. This is where you should consult your balance sheet. If you have $500,000 in home equity and $200,000 in a 401(k), a “25/50” policy (which covers $25,000 per person and $50,000 per accident) is a financial liability. You are essentially leaving $650,000 of your wealth exposed. For high-net-worth individuals, getting car insurance often involves adding an “Umbrella Policy” which provides an extra layer of $1 million or more in liability protection over and above the auto policy.

Finalizing the Contract and Setting Up Payments

Once you select a provider, you will sign a binding agreement. From a cash-flow management perspective, look at the payment options. Paying in full usually eliminates “installment fees,” which can add 5% to 10% to the total cost of the policy. If you cannot pay in full, set up automated payments to avoid late fees and the risk of a “lapse in coverage.” A lapse is a major financial red flag that can cause your future premiums to skyrocket, as insurers view uninsured periods as high-risk behavior.

Advanced Financial Strategies to Lower Long-Term Costs

Getting car insurance is not a one-time event; it is an ongoing expense that should be audited regularly to ensure it remains aligned with your financial goals.

Pay-Per-Mile and Usage-Based Insurance Models

For those who work from home or use public transit, traditional “static” insurance policies may be a poor financial investment. Usage-based insurance (UBI) uses telematics to track your actual driving habits. If you drive fewer miles or demonstrate safe driving behaviors, your premiums are adjusted downward. This “pay-as-you-go” model allows you to align your insurance expenses directly with your actual usage, much like a utility bill, potentially saving hundreds of dollars a year.

The Self-Insurance Alternative for High-Net-Worth Individuals

In some jurisdictions and for some very wealthy individuals, “self-insurance” is a legal and financial option. This involves depositing a large sum of money (often $50,000 to $100,000) with the state’s Department of Motor Vehicles to prove you have the liquidity to cover an accident. While this eliminates premiums, it carries high opportunity costs. That $50,000 could be earning 7-10% in the stock market. For 99% of people, traditional insurance remains the superior financial tool because it provides millions in coverage for a relatively small annual fee.

Annual Policy Audits: Keeping Costs Aligned with Depreciating Assets

Vehicles are depreciating assets. As your car loses value, the amount of insurance you need changes. Every year, during your financial “spring cleaning,” you should review your car insurance policy. Does the “actual cash value” of the car still justify a $500 deductible? Have you improved your credit score? Have you moved to a ZIP code with lower crime rates? Each of these factors can be leveraged to renegotiate your premium.

In conclusion, getting car insurance is an exercise in strategic financial planning. By understanding the mechanics of risk, comparing providers with an eye for ROI, and maintaining a high credit profile, you can secure protection that not only keeps you legal on the road but also safeguards your long-term financial health. Treat your insurance policy as a dynamic part of your portfolio, and it will serve as a resilient shield for your wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.