Securing a credit card is often viewed as a rite of passage in one’s financial journey. It represents a transition from simple cash transactions to a more sophisticated ecosystem of credit building, consumer protection, and financial leverage. However, the process of obtaining a credit card is governed by a complex set of regulations, credit scoring models, and institutional risk assessments. Understanding how to navigate this landscape is essential not just for approval, but for ensuring that the financial tool you acquire aligns with your long-term wealth-building goals.

In the modern economy, a credit card is more than just a payment method; it is a gateway to financial flexibility. From earning travel rewards to establishing the credit history necessary for a mortgage, the stakes are high. This guide provides a detailed roadmap for securing a credit card, emphasizing the “Money” niche through the lens of personal finance management and strategic planning.

1. Understanding the Prerequisites: What You Need Before Applying

Before you submit an application, you must understand that banks and credit unions are essentially evaluating your “creditworthiness.” They are trying to predict the likelihood that you will pay back what you borrow. This assessment is based on several foundational pillars.

The Role of the Credit Score and History

Your credit score is arguably the most critical factor in the approval process. Most lenders rely on FICO or VantageScore models, which aggregate your history of borrowing and repayment. Scores typically range from 300 to 850. If you are a first-time applicant, you may have a “thin file,” meaning there isn’t enough data to generate a score. In this case, lenders look for other signs of stability. If you already have a history, knowing your score allows you to target cards you are actually qualified for, preventing unnecessary “hard inquiries” that can temporarily lower your score.

Income and Debt-to-Income (DTI) Ratio

Under the Credit CARD Act of 2009, lenders are required to evaluate a borrower’s ability to make payments. This means you must provide proof of income. For individuals over 21, this can include “accessible” income, such as a spouse’s salary or household earnings. For those between 18 and 21, the requirements are stricter, often requiring independent income or a co-signer. Furthermore, lenders look at your Debt-to-Income (DTI) ratio—the percentage of your monthly gross income that goes toward paying debts. A lower DTI suggests you have the financial “breathing room” to handle a new line of credit.

Legal and Personal Documentation

To comply with “Know Your Customer” (KYC) regulations and anti-money laundering laws, financial institutions require specific documentation. You will need a Social Security Number (SSN) or an Individual Taxpayer Identification Number (ITIN). Additionally, you must provide a valid residential address (usually not a P.O. Box for the initial application) and proof of legal age.

2. Choosing the Right Card for Your Financial Goals

Not all credit cards are created equal. Applying for the “wrong” card—one that doesn’t fit your spending habits or credit profile—is a common financial mistake. Selecting a card should be a strategic decision based on where you are in your financial journey.

Rewards vs. Utility: Identifying Your Needs

For those with established credit, rewards cards offer a way to “gamify” spending. These cards provide cash back, points, or miles on every dollar spent. However, these often come with higher interest rates. If your goal is to carry a balance (which is generally discouraged in personal finance), you should prioritize a Low-APR card rather than a rewards card. If you are a frequent traveler, a card with no foreign transaction fees and airport lounge access might be the priority. Identifying the “utility” of the card ensures you aren’t paying for features you won’t use.

Understanding the Cost of Ownership: Fees and APR

Professional financial planning requires a deep dive into the fine print. You must evaluate the Annual Percentage Rate (APR), which is the cost of borrowing if you don’t pay your balance in full each month. Additionally, be wary of annual fees. While some high-end cards charge $500 or more per year, they often provide “credits” that offset the cost. If you are just starting out, a “no-annual-fee” card is typically the smartest move to minimize overhead costs while building your credit profile.

The Specialized Market: Student and Secured Cards

If you have no credit history or a damaged score, the “standard” cards may be out of reach. This is where student cards and secured cards come in. Student cards are designed for young adults with limited income and history, often offering modest rewards and lower barriers to entry. Secured cards, on the other hand, require a refundable security deposit that usually acts as your credit limit. In the world of personal finance, a secured card is a vital “rebuilding” tool that proves to lenders you can handle credit responsibly.

3. The Step-by-Step Application Process

Once you have identified the right card, the application process itself requires precision. In the digital age, this process is faster than ever, but it still requires a methodical approach to ensure the best possible outcome.

Prequalification and Soft Inquiries

Many major issuers offer a “prequalification” or “pre-approval” tool on their websites. This is a crucial step for the savvy consumer. Prequalification uses a “soft pull” on your credit report, which does not affect your credit score. It gives you a high-level indication of whether you might be approved. While not a guarantee, it significantly reduces the risk of applying for a card that is out of your reach and suffering a useless hard inquiry.

Accuracy in the Application Form

When filling out the formal application, accuracy is paramount. Discrepancies in your income, employment history, or address can trigger a fraud alert or an automatic denial. Ensure that the income you report is verifiable. In many cases, digital applications use automated underwriting systems that provide a decision within seconds. If your application is “pending,” it usually means a human underwriter needs to review your documentation manually.

Navigating the Hard Inquiry and Decision

When you click “submit,” the lender performs a “hard inquiry” (or “hard pull”). This allows them to see your full credit report. A single hard pull typically knocks fewer than five points off your FICO score, but multiple pulls in a short period can signal “credit hunger,” which is a red flag to lenders. If you are denied, the lender is legally required to send you an “Adverse Action Notice,” which explains why you were turned down and which credit bureau provided the data. This document is a valuable financial diagnostic tool.

4. Strategies for Success with Limited Credit History

If you are struggling to get your first “Yes” from a lender, you don’t have to wait idly. There are active financial strategies to make yourself a more attractive candidate over time.

The Authorized User Strategy

One of the fastest ways to “import” a credit history is by becoming an authorized user on a family member’s account. If the primary cardholder has a long history of on-time payments and low credit utilization, that positive data can often be reflected on your credit report. However, this is a double-edged sword; if the primary cardholder misses a payment, it could negatively impact your score as well. This strategy should only be used with a trusted, financially disciplined partner.

Building a Relationship with a Financial Institution

Banks are often more willing to extend credit to existing customers. If you have had a checking or savings account with a credit union or bank for several years, they have internal data on your cash flow that an outside credit bureau doesn’t have. Speaking with a representative at your local branch can sometimes lead to a “manual override” or a recommendation for a starter card that isn’t heavily advertised online.

Credit Builder Loans and Alternative Data

Some financial tech (FinTech) companies now offer credit-builder loans. Instead of receiving the money upfront, you make monthly payments into a locked savings account, and the lender reports these payments to the credit bureaus. Once the “loan” is paid off, you receive the capital. Additionally, some services allow you to add “alternative data”—such as rent and utility payments—to your credit file, which can boost your score enough to qualify for an entry-level credit card.

5. Responsible Usage: Maintaining Your Financial Health Post-Approval

Getting the card is only the beginning. The way you manage the card in the first six to twelve months will determine your future credit limit increases and your ability to access lower interest rates on car loans and mortgages.

The 30% Rule: Managing Credit Utilization

In the world of personal finance, “credit utilization” is a key metric. It is the ratio of your outstanding balance to your total credit limit. Professional financial advisors recommend keeping this ratio below 30%, though below 10% is ideal for a top-tier credit score. For example, if you have a $1,000 limit, try never to have a balance higher than $300 reported to the bureaus. This demonstrates that you have access to credit but are not reliant on it.

The Importance of the Statement Balance and Due Dates

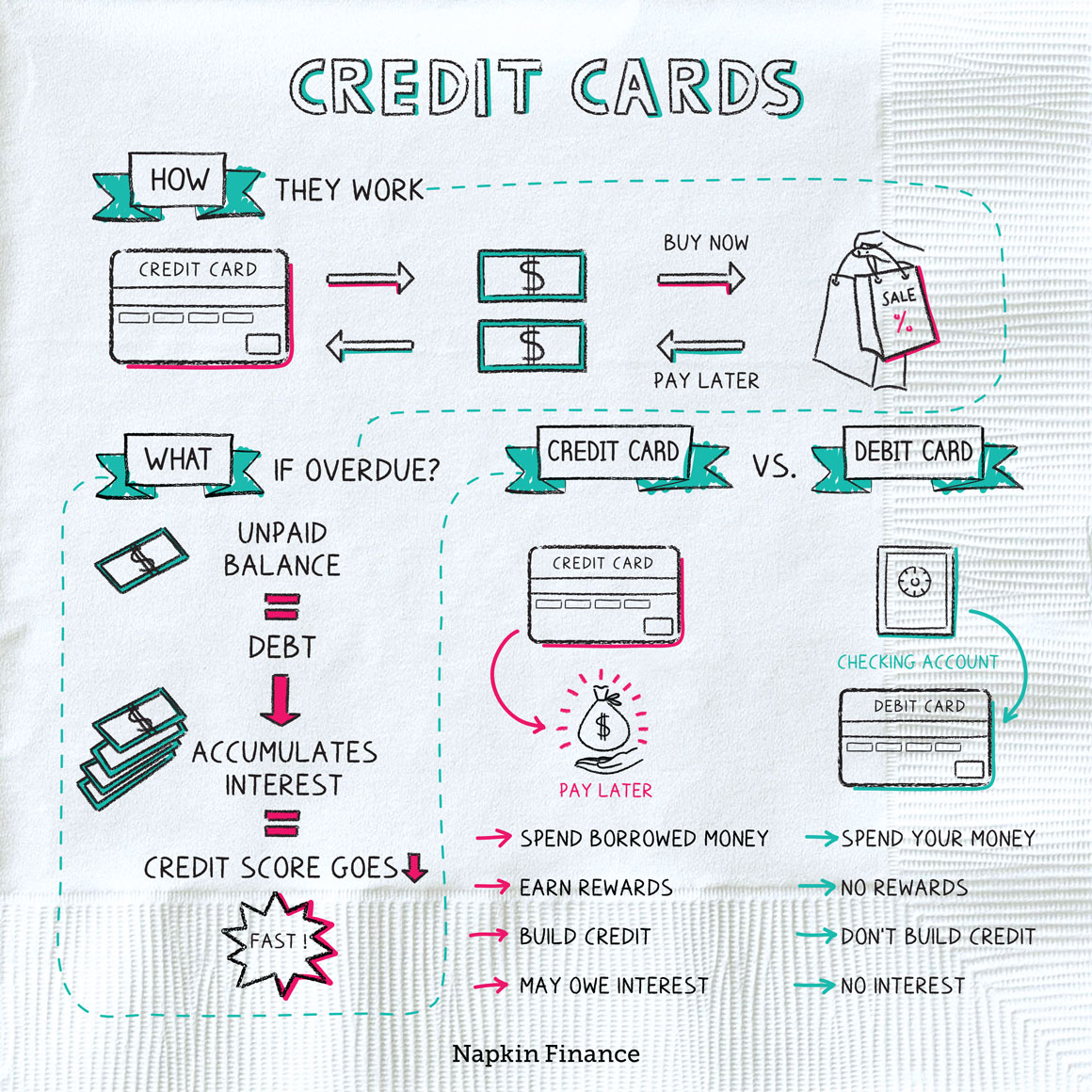

To avoid interest charges entirely, you must pay the “statement balance” in full by the due date every month. Paying only the “minimum amount” is a debt trap; the remaining balance will accrue interest at the card’s APR, which is often 20% or higher. By paying in full, you take advantage of the “grace period,” essentially getting an interest-free loan for 21 to 25 days. Setting up autopay is a fundamental habit for anyone looking to maintain a perfect payment history.

Monitoring for Fraud and Credit Health

Once you have a credit card, you are responsible for monitoring your statements. Most modern apps allow you to set up real-time transaction alerts. Furthermore, you should regularly check your credit report via sites like AnnualCreditReport.com to ensure no unauthorized accounts have been opened in your name. Managing a credit card is a continuous process of vigilance and strategic planning, ensuring that the card remains a tool for wealth creation rather than a source of financial stress.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.