The journey to homeownership is often described as one of life’s most significant financial milestones. For most, this journey begins not with finding the perfect house, but with securing the right financing. Your mortgage lender isn’t just a financial institution; they are a crucial partner in this process, guiding you through complex decisions and helping you unlock the door to your new home. But with a myriad of options available, the question naturally arises: how do you find a mortgage lender that is the best fit for your unique needs?

Navigating the mortgage landscape can feel daunting, with terms like interest rates, APR, closing costs, and loan types swirling around. This comprehensive guide aims to demystify the process, providing you with a structured approach to identifying, evaluating, and ultimately choosing the right mortgage lender. By understanding your options, preparing thoroughly, and asking the right questions, you can transform a potentially stressful search into a confident step towards homeownership.

Understanding Your Mortgage Lender Options

Before diving into the specifics of how to find a lender, it’s essential to understand the different types of institutions and professionals that offer mortgage services. Each has its own operational model, advantages, and potential drawbacks, making some better suited for certain borrowers than others.

Traditional Banks and Credit Unions

These are often the first places people think of when considering a mortgage. Large national banks, regional banks, and local credit unions have long been pillars of the lending industry.

- Banks: Offer a wide range of financial products, often have extensive branch networks, and can provide competitive rates, especially for existing customers. They typically underwrite and service their own loans.

- Credit Unions: Member-owned non-profit organizations. They often offer more personalized service and may have slightly lower interest rates or fees compared to traditional banks due to their non-profit status. Membership requirements usually apply.

Pros: Established reputation, in-person support, potential for bundled services.

Cons: Potentially slower application processes, less flexibility for unique financial situations.

Online Lenders

The digital age has ushered in a new era of mortgage lending. Online lenders operate primarily or exclusively through digital platforms, streamlining much of the application process.

- Examples: Quicken Loans (Rocket Mortgage), Better.com, LendingTree.

- Process: Often feature user-friendly websites, online portals for document submission, and automated underwriting processes.

Pros: Speed and convenience, often competitive rates and lower fees due to reduced overhead, transparent online tools.

Cons: Less personal interaction, may not be ideal for complex financial scenarios, reliance on technology.

Mortgage Brokers

A mortgage broker acts as an intermediary between borrowers and multiple lenders. They don’t lend money themselves but work with a network of banks, credit unions, and other lending institutions to find a loan that matches your profile.

- Role: Brokers shop around on your behalf, comparing different loan products, rates, and terms from various lenders. They are paid a commission either by the lender or, in some cases, by the borrower (or both).

Pros: Access to a wider range of loan products, expert guidance, can be beneficial for borrowers with unique financial situations, potential to find niche lenders.

Cons: May charge a fee, could have incentives to push certain lenders, you still need to vet the broker carefully.

Direct Lenders vs. Portfolio Lenders

It’s also helpful to distinguish between direct and portfolio lenders, though these categories can overlap with the above types.

- Direct Lenders: These are institutions that lend their own money directly to borrowers. Most banks, credit unions, and many online lenders fall into this category. They control the entire process from application to closing.

- Portfolio Lenders: A subset of direct lenders, portfolio lenders keep the loans they originate on their own books rather than selling them on the secondary market. This allows them more flexibility in underwriting and can be an advantage for borrowers who don’t fit conventional lending criteria.

Understanding these distinctions will help you refine your search and better appreciate the advice you receive from different sources.

Preparing for Your Mortgage Search

Before you even start contacting lenders, a solid foundation of preparation will significantly improve your chances of securing favorable terms and a smooth application process. Think of it as getting your financial house in order before buying a new one.

Assessing Your Financial Health

Lenders will scrutinize your financial history to assess your creditworthiness. Understanding where you stand is crucial.

- Credit Score: Your FICO score is paramount. Lenders use it to gauge your reliability in repaying debts. Aim for a score of 740 or higher for the best rates, though many loan programs are available for lower scores. Check your credit report from all three major bureaus (Equifax, Experian, TransUnion) annually for free at AnnualCreditReport.com and dispute any errors.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Most lenders prefer a DTI of 43% or lower, though some programs allow for higher. A lower DTI indicates you have more disposable income to put towards a mortgage payment.

Knowing Your Budget and Down Payment

Be realistic about what you can afford. This involves more than just the monthly mortgage payment.

- Purchase Price & Down Payment: Determine how much house you can realistically afford based on your income, savings, and desired down payment. A larger down payment (e.g., 20% or more) can lead to better interest rates and helps you avoid Private Mortgage Insurance (PMI).

- Additional Costs: Remember to factor in property taxes, homeowner’s insurance, potential HOA fees, and closing costs, which can add 2-5% of the loan amount.

Gathering Essential Documents

Having your paperwork ready demonstrates your seriousness and can expedite the application process.

- Income Verification: Pay stubs (last 30 days), W-2 forms (last two years), tax returns (last two years), and if self-employed, profit and loss statements.

- Asset Verification: Bank statements (last two months), investment account statements.

- Credit History: Explanation for any credit issues (e.g., bankruptcy, foreclosures).

- Identification: Driver’s license, Social Security card.

Strategies for Researching and Comparing Lenders

With your financial ducks in a row, it’s time to actively search for lenders. This phase requires diligence and a strategic approach to ensure you get the best possible deal.

Leveraging Online Comparison Tools

The internet offers powerful resources for an initial sweep of the market.

- Mortgage Rate Comparison Websites: Sites like LendingTree, Bankrate, Zillow Mortgages, and NerdWallet allow you to input your financial information and desired loan type to receive multiple quotes from various lenders simultaneously. This is an excellent starting point for comparing general rates and fees.

- Lender Websites: Once you have a shortlist, visit individual lender websites. Many offer rate calculators and detailed information on their loan products.

Seeking Recommendations and Reviews

Personal experiences can provide invaluable insights that online numbers might miss.

- Ask Your Network: Talk to friends, family, real estate agents, and financial advisors who have recently gone through the mortgage process. They can share their experiences, both positive and negative, with specific lenders or brokers.

- Read Online Reviews: Check platforms like Google Reviews, Yelp, and the Better Business Bureau. Look for consistent themes regarding customer service, transparency, speed of closing, and communication. Be wary of lenders with numerous complaints about hidden fees or poor communication.

Understanding Loan Types and Interest Rates

Not all loans are created equal, and the type you choose will significantly impact your monthly payments and long-term costs.

- Fixed-Rate Mortgages (FRM): Interest rate remains the same for the life of the loan (e.g., 15-year or 30-year fixed). Predictable payments, good for long-term stability.

- Adjustable-Rate Mortgages (ARM): Interest rate is fixed for an initial period, then adjusts periodically based on a market index. Can offer lower initial payments but carries interest rate risk.

- Government-Backed Loans: FHA loans (low down payment, easier credit requirements), VA loans (for eligible veterans, often no down payment), USDA loans (for rural properties, low-income borrowers).

- Interest Rates vs. APR: Understand the difference. The interest rate is the cost of borrowing money. The Annual Percentage Rate (APR) includes the interest rate plus certain fees and other costs, providing a more comprehensive measure of the total cost of the loan over its term. Always compare APRs for an apples-to-apples comparison.

The Importance of Getting Multiple Quotes (Loan Estimates)

This is arguably the most critical step in securing the best mortgage.

- Shop Around: Contact at least 3-5 different lenders (including banks, credit unions, and online lenders) and request a Loan Estimate.

- The Loan Estimate (LE): This is a standardized, three-page form that lenders are required to provide within three business days of receiving your application. It details the interest rate, monthly payment, closing costs, and other loan terms. Crucially, it allows for easy comparison between different lenders. Focus on comparing Section A (origination charges), Section B (services you cannot shop for), and the “Cash to Close” figure.

- Impact on Credit Score: Don’t worry about multiple inquiries for a mortgage within a short period (typically 14-45 days) affecting your credit score too much. Credit bureaus recognize this as rate shopping for a single loan, and it will usually count as only one hard inquiry.

Key Factors to Consider When Choosing a Lender

Beyond just the lowest interest rate, several other factors contribute to a positive borrowing experience and a financially sound decision.

Interest Rates and Fees (APR vs. Interest Rate)

While the lowest interest rate is appealing, ensure you understand all associated costs.

- Origination Fees: Charges for processing your loan application.

- Discount Points: Upfront fees paid to “buy down” your interest rate.

- Other Closing Costs: Appraisal fees, title insurance, recording fees, attorney fees, etc.

- Analyze the APR: As mentioned, the APR provides a more holistic view of the loan’s cost. A slightly higher interest rate with significantly lower fees might result in a better APR and lower overall cost.

Customer Service and Communication

The mortgage process can be complex and requires clear communication.

- Responsiveness: How quickly do they respond to your inquiries? Are they proactive in providing updates?

- Clarity: Do they explain terms and processes in an understandable way? Are they patient with your questions?

- Accessibility: How easy is it to reach your loan officer or their support team?

- Trust: Do you feel comfortable and confident in their guidance?

Loan Program Variety and Flexibility

A good lender should have a range of options to suit different borrower profiles.

- Diverse Offerings: Do they offer FHA, VA, USDA, conventional, jumbo, or portfolio loans? This indicates their ability to cater to various needs.

- Solutions for Unique Situations: If your financial situation is complex (e.g., self-employed, non-traditional income), inquire about their flexibility and experience with such cases.

Lender Reputation and Reliability

A lender’s track record speaks volumes.

- Industry Standing: Are they well-established and reputable in the mortgage industry?

- Accreditations: Check for memberships in professional organizations.

- Compliance: Do they adhere to lending regulations and ethical practices? A reliable lender ensures a smooth closing without last-minute surprises or changes to terms.

Closing Costs and Transparency

Surprises at the closing table are undesirable. A good lender provides clear, upfront information.

- Detailed Breakdown: Ensure the Loan Estimate provides a clear breakdown of all closing costs.

- No Hidden Fees: Ask direct questions about any potential fees not explicitly listed.

- Closing Timeline: Understand their typical closing timeline and any guarantees they offer.

Navigating the Application and Approval Process

Once you’ve chosen a lender, the next phase involves the formal application and approval steps. Understanding this journey will help manage expectations.

Pre-Qualification vs. Pre-Approval

These terms are often used interchangeably but have crucial distinctions.

- Pre-Qualification: An informal estimate of what you might be able to borrow, based on self-reported financial information. It’s a good starting point for budgeting but carries no commitment from the lender.

- Pre-Approval: A conditional commitment from a lender to loan you a specific amount, based on a verified review of your credit report, income, and assets. It involves a hard credit pull and provides a much stronger offer when making bids on homes. Always aim for pre-approval.

Submitting Your Application

This involves formally providing all requested documentation to your chosen lender. Be prepared for follow-up questions and requests for additional information. Timeliness in responding will keep the process moving.

Underwriting and Appraisal

- Underwriting: The lender’s team reviews all your financial information, the property details, and the loan application to assess the risk involved and ensure everything meets their guidelines and regulatory requirements.

- Appraisal: An independent professional evaluates the home’s value to ensure it matches or exceeds the purchase price. This protects both the borrower and the lender.

- Title Search: A check is performed to ensure the property’s title is clear of any liens or disputes.

Closing Day Expectations

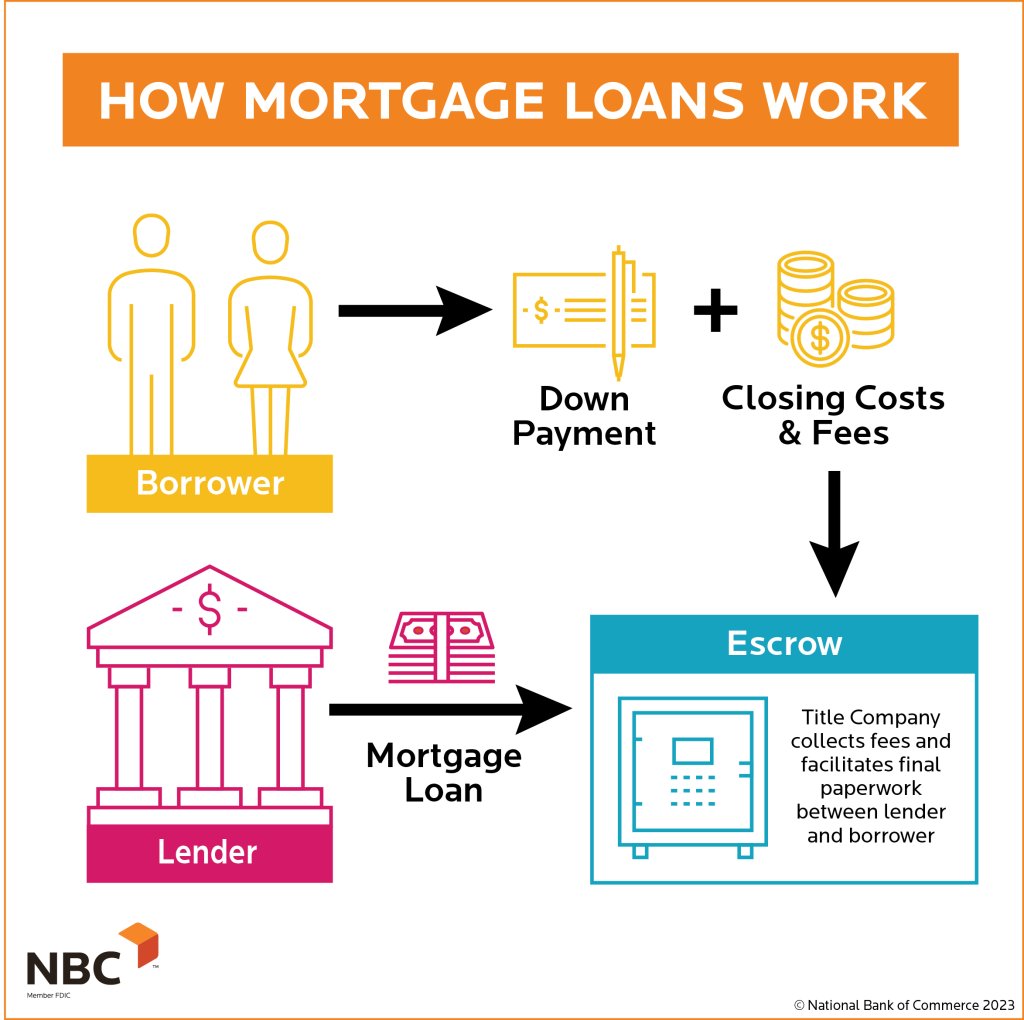

The final step where all documents are signed, funds are exchanged, and ownership is transferred. Your lender will work with the title company or attorney to coordinate this. Review your Closing Disclosure (CD) carefully against your last Loan Estimate at least three business days before closing to catch any discrepancies.

Finding the right mortgage lender is a critical step in your homeownership journey. By understanding your options, diligently preparing your finances, strategically comparing offers, and focusing on both rates and service, you empower yourself to make an informed decision. Remember, you’re not just looking for a loan; you’re looking for a reliable partner to guide you through one of life’s most significant investments. Take your time, ask plenty of questions, and choose wisely.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.