Navigating the world of car financing can often feel like deciphering a complex financial puzzle, and car leasing is no exception. For many consumers, the allure of lower monthly payments compared to purchasing a new vehicle makes leasing an attractive option. However, understanding how those payments are calculated is crucial for making an informed decision and ensuring you’re getting a fair deal. Rather than simply accepting a dealer’s quoted monthly figure, empowering yourself with knowledge of the underlying financial mechanics will transform you from a passive consumer into an astute negotiator. This article will demystify the car lease payment calculation, breaking down its core components, the formula, influencing factors, and strategies for securing a more favorable agreement, all within the realm of personal finance and smart money management.

The Core Components of a Car Lease Payment

At its heart, a car lease payment is a calculation based on how much the vehicle depreciates during your usage, plus a finance charge for the privilege of driving it. Unlike buying, where you pay for the entire car, leasing means you’re only paying for the portion of its value you “use up” over the lease term. Several key variables contribute to this figure, each playing a significant role in the final monthly cost.

Capitalized Cost (Cap Cost)

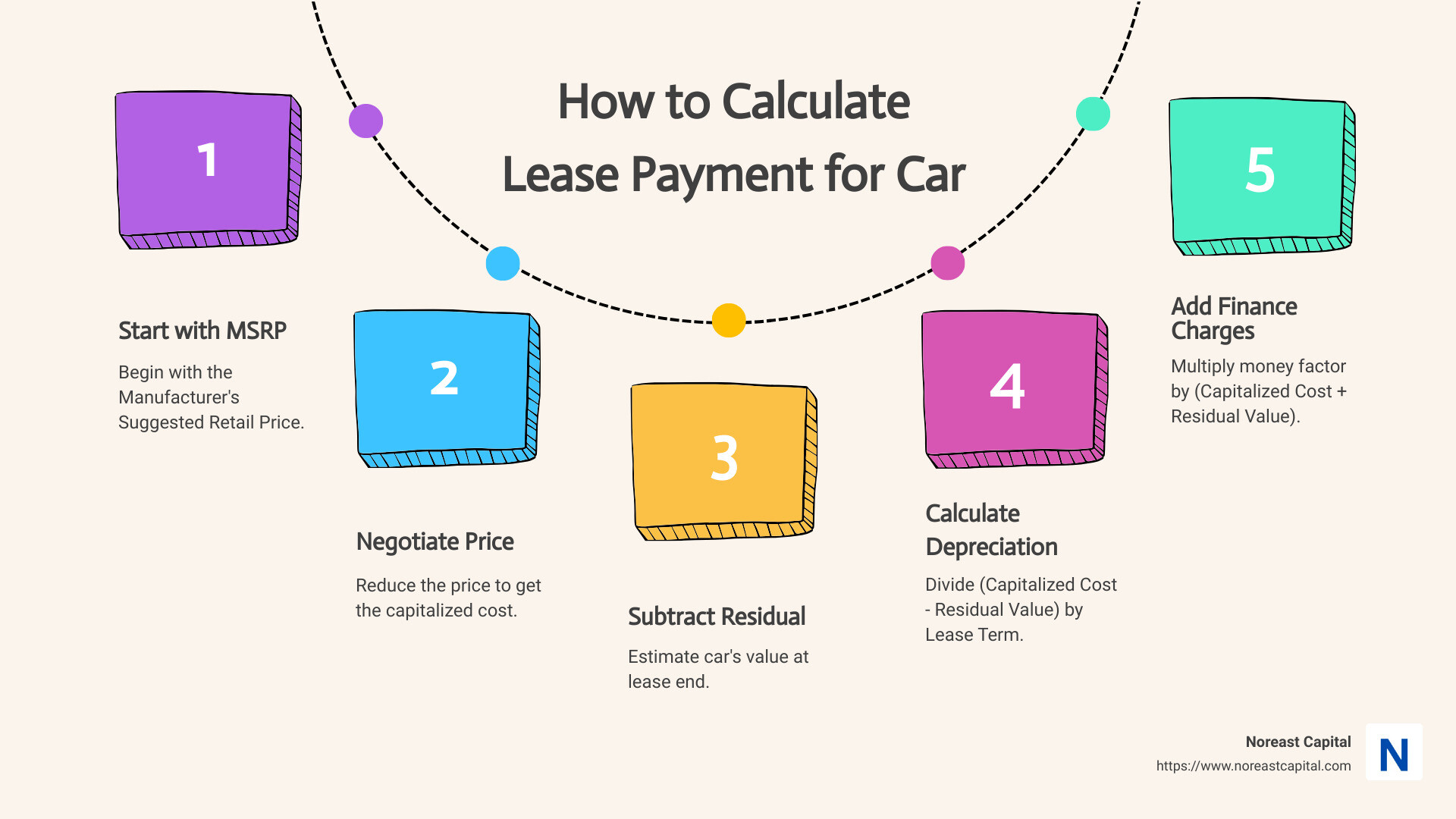

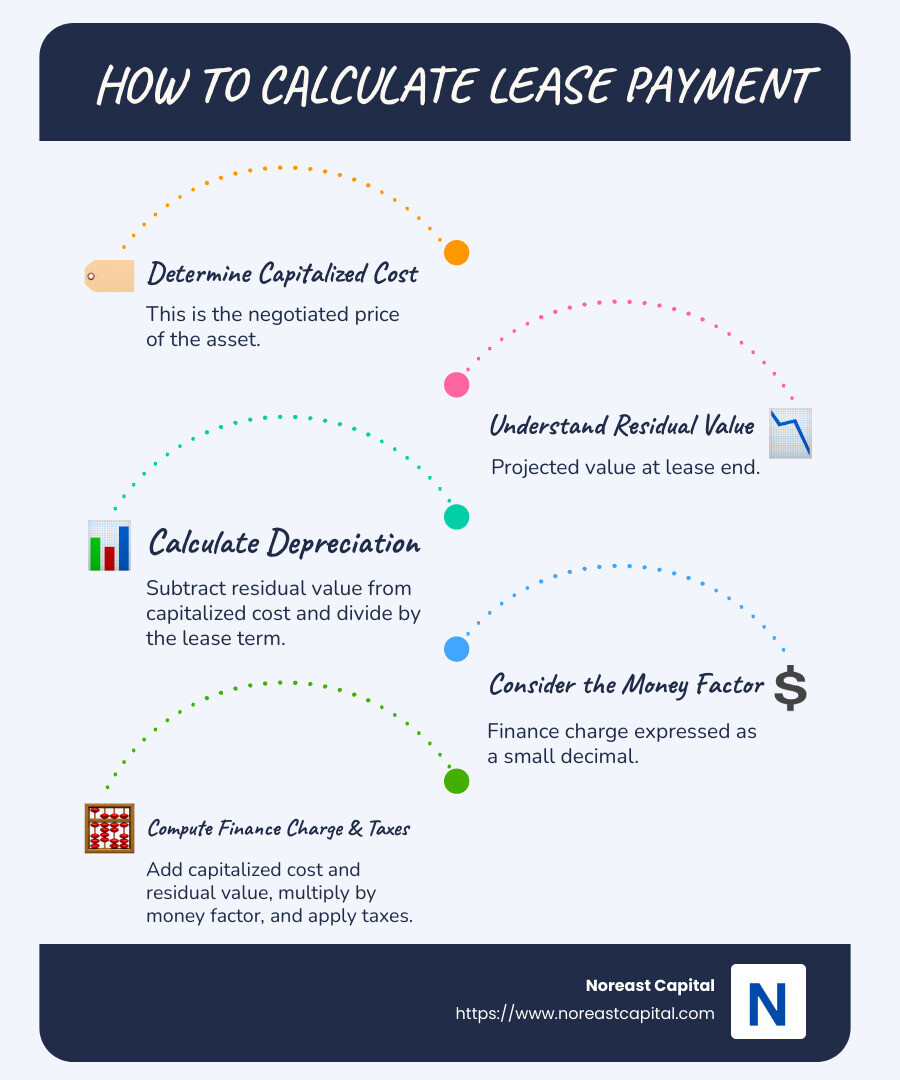

Often referred to as the “selling price” of the car in a lease context, the capitalized cost is the starting point for your lease calculation. It’s the agreed-upon value of the vehicle at the beginning of the lease term. Many consumers mistakenly believe the cap cost is non-negotiable, but this is a critical financial misstep. Just as you would negotiate the purchase price of a car, you can — and should — negotiate the capitalized cost. A lower cap cost directly translates to a lower monthly payment because it reduces the amount the car has to depreciate from, as well as the base for the finance charge. Discounts, rebates, and the value of any trade-in or down payment will all reduce this figure.

Residual Value

The residual value is arguably one of the most significant determinants of your monthly lease payment. It represents the estimated wholesale value of the vehicle at the end of the lease term, as determined by the leasing company (often based on industry data and projections). This value is usually expressed as a percentage of the car’s Manufacturer’s Suggested Retail Price (MSRP). The difference between the capitalized cost and the residual value is the total amount you will effectively “pay for” through depreciation over the lease term. A higher residual value means the car is expected to hold its value better, resulting in less depreciation and, consequently, lower monthly payments for you. Conversely, vehicles with lower residual values lead to higher payments. While generally non-negotiable, understanding the residual value helps compare different lease offers.

Money Factor (Lease Rate)

Think of the money factor as the interest rate equivalent in a lease agreement. It’s the cost of financing the lease, similar to the interest you’d pay on a loan. However, instead of being expressed as a straightforward annual percentage rate (APR), the money factor is typically a very small decimal (e.g., 0.00250). To convert a money factor to an approximate annual interest rate, you simply multiply it by 2400 (0.00250 x 2400 = 6%). A lower money factor signifies a cheaper cost of borrowing and will reduce your monthly lease payment. Your creditworthiness plays a substantial role here; excellent credit often qualifies you for the lowest money factors offered by the leasing company or manufacturer.

Lease Term

The lease term is simply the duration of your lease agreement, typically expressed in months (e.g., 24, 36, or 48 months). While a longer lease term might result in a lower monthly payment (because the total depreciation is spread out over more months), it can also mean you pay more in total finance charges over the life of the lease. Shorter terms often have higher monthly payments but can align better with specific depreciation curves and may allow you to upgrade to a newer model sooner. It’s a balance between affordability and how frequently you wish to change vehicles.

Understanding the Lease Payment Calculation Formula

With the core components identified, we can now assemble them into the formula used to calculate your monthly lease payment. It’s not as daunting as it might seem, boiling down to two primary parts: the depreciation charge and the finance charge.

Depreciation Portion

This segment of your payment covers the amount of value the car loses over the lease term. It’s calculated by taking the difference between the capitalized cost and the residual value, and then dividing that figure by the number of months in the lease term.

Formula: (Capitalized Cost – Residual Value) / Lease Term (in months)

For example, if your negotiated Cap Cost is $30,000, and the Residual Value is $18,000 for a 36-month lease:

($30,000 – $18,000) / 36 = $12,000 / 36 = $333.33 (Depreciation Portion)

Finance Charge Portion

This is the cost of borrowing, or the “interest” on your lease. It’s calculated by adding the capitalized cost and the residual value, and then multiplying that sum by the money factor. The logic here is that the leasing company is financing the average value of the vehicle over the lease term.

Formula: (Capitalized Cost + Residual Value) * Money Factor

Using the same example with a money factor of 0.00250:

($30,000 + $18,000) * 0.00250 = $48,000 * 0.00250 = $120.00 (Finance Charge Portion)

Monthly Payment Summation

Finally, to arrive at your base monthly lease payment, you simply add the depreciation portion and the finance charge portion together.

Formula: Depreciation Portion + Finance Charge Portion

Continuing our example:

$333.33 (Depreciation) + $120.00 (Finance Charge) = $453.33 (Base Monthly Payment)

Sales Tax and Fees

It’s important to remember that this base payment often doesn’t include sales tax or various fees. Sales tax is typically applied to the monthly payment in most states, while some states might tax the entire capitalized cost upfront. Additionally, acquisition fees, documentation fees, registration, and license plate fees can be rolled into the capitalized cost, paid upfront, or added to your monthly payment. Always clarify how these additional costs are handled before finalizing your lease agreement to avoid surprises.

Factors That Influence Your Monthly Lease Payment

While the core formula provides a clear framework, several other factors can significantly influence the final monthly figure you pay. Understanding these allows you to strategically manage your lease agreement and potentially lower your costs.

Down Payment (Capitalized Cost Reduction)

Making a down payment on a lease, often called a “capitalized cost reduction,” works similarly to a down payment on a purchase. It directly reduces the capitalized cost of the vehicle, which in turn lowers both the depreciation portion and the finance charge portion of your monthly payment. For example, a $2,000 down payment would reduce our example’s Cap Cost from $30,000 to $28,000, immediately lowering the depreciation. While this reduces your monthly outlay, financial advisors often caution against large down payments on leases due to the risk of losing that money if the car is stolen or totaled early in the lease term.

Trade-in Equity

If you have positive equity in your current vehicle (meaning its market value is greater than what you owe on it), you can use this equity as a capitalized cost reduction. Essentially, the dealership “buys” your old car for its equity, and that money is applied to lower the cap cost of your new lease. This is a common and effective way to reduce your monthly payments without directly taking money out of your pocket.

Manufacturer Incentives and Rebates

Manufacturers frequently offer special lease incentives to stimulate sales of particular models. These can take various forms: a direct reduction in the capitalized cost, a lowered money factor, or an inflated residual value. These “lease specials” are often advertised and can drastically reduce your monthly payment. Always research available manufacturer incentives for the specific make and model you’re interested in before stepping into a dealership.

Credit Score

Your credit score is a powerful determinant of the money factor you’ll be offered. Lenders reserve their lowest money factors for lessees with excellent credit histories, as they represent the least risk. A lower credit score will typically result in a higher money factor, meaning you pay more in finance charges over the life of the lease. Before negotiating a lease, it’s wise to check your credit score and history to ensure accuracy and understand your negotiating position.

Mileage Allowance

Lease agreements come with a specified annual mileage allowance (e.g., 10,000, 12,000, or 15,000 miles per year). This allowance is a critical factor in determining the car’s residual value. Vehicles with higher mileage allowances are projected to have lower residual values at the end of the lease, as they will have accumulated more wear and tear and depreciation. Consequently, opting for a higher mileage allowance will typically result in a higher monthly payment because the depreciation portion increases. Be realistic about your driving habits to avoid costly over-mileage penalties (often $0.15-$0.30 per mile) at lease end.

Strategies to Negotiate a Better Lease Deal

Equipped with an understanding of how lease payments are calculated, you’re no longer at the mercy of the dealership’s numbers. You can proactively negotiate a lease that aligns better with your financial goals.

Negotiate the Capitalized Cost

This is the most impactful negotiation point. Approach the lease as if you were buying the car outright. Research the fair market value of the vehicle you’re interested in and negotiate the lowest possible “selling price” before discussing lease terms. A lower capitalized cost directly reduces both the depreciation and finance charge components of your payment.

Understand and Negotiate the Money Factor

Don’t just accept the money factor presented to you. Ask the dealer for it upfront. Convert it to an approximate APR (multiply by 2400) to better understand the cost of financing. If you have excellent credit, you should expect to qualify for the manufacturer’s best lease rates. Be prepared to compare offers from multiple dealerships and even credit unions, which sometimes offer competitive direct lease options.

Be Aware of the Residual Value

While the residual value is largely set by the leasing company (and often uniform across dealerships for a given model and term), knowing it is crucial. It allows you to compare different vehicles and understand how well a particular model is expected to hold its value. A higher residual value for a similar vehicle can lead to a more affordable lease, even if the capitalized cost is slightly higher.

Shop Around

Just as with car purchases, comparing lease offers from multiple dealerships is essential. Different dealerships might have different pricing strategies, access to varying incentives, or more flexibility on the capitalized cost. Pit competing offers against each other to drive down your overall cost. Consider looking at different brands as well, as some manufacturers are more aggressive with lease programs at certain times.

Avoid Unnecessary Add-ons

Dealerships often try to include optional services and products, such as extended warranties, paint protection, or credit insurance, into your lease agreement. These can inflate your capitalized cost and, consequently, your monthly payment. Carefully scrutinize every item and only agree to those that genuinely provide value and are not already covered by the manufacturer’s warranty.

Essential Considerations Before Signing a Lease

Beyond the numbers, a comprehensive understanding of the lease agreement’s terms and conditions is vital to avoid unwelcome surprises down the road.

Total Cost vs. Monthly Payment

It’s easy to get fixated on the attractive low monthly payment of a lease. However, always calculate the total cost of the lease over its term. This includes any upfront payments (down payment, fees, first month’s payment), the sum of all monthly payments, and potential end-of-lease fees. Sometimes, a slightly higher monthly payment might be part of a deal with fewer upfront costs, leading to a similar or even lower total cost.

End-of-Lease Options

Know your options and obligations when the lease term concludes. You typically have three choices: return the vehicle, purchase it, or lease a new one. If you intend to purchase, understand the pre-determined buyout price (often the residual value plus a purchase option fee). If returning, be aware of inspection processes, potential charges for excess wear and tear, and disposition fees.

Wear and Tear Policy

Lease agreements have specific guidelines for what constitutes “excessive” wear and tear. Dings, dents, scratches, tire wear beyond a certain limit, or interior damage can result in significant penalties at lease end. Review these policies carefully and consider whether you typically maintain vehicles in pristine condition or if you might be prone to incurring such charges. Some leases offer wear-and-tear waivers, which might be worth considering if you anticipate minor damage.

Insurance Requirements

Lenders require comprehensive insurance coverage on leased vehicles to protect their asset. This often means higher liability limits and lower deductibles than you might typically carry. Obtain insurance quotes for the specific vehicle you intend to lease before signing, as the cost can be substantial and directly impact your overall monthly financial outlay.

Early Termination Penalties

One of the most critical aspects to understand is the high cost of terminating a lease early. If your circumstances change and you need to get out of the lease before its term is up, you could face substantial penalties, sometimes totaling thousands of dollars. These penalties often involve paying the remaining depreciation, all outstanding finance charges, and an early termination fee. Always consider your stability and potential future needs before committing to a lease term.

Conclusion

Figuring out a car lease payment involves more than just glancing at a monthly figure; it’s a strategic financial endeavor that requires understanding its core components, the underlying formula, and the various factors that influence the final cost. By familiarizing yourself with capitalized cost, residual value, and money factor, you empower yourself to approach negotiations with confidence and insight. Smart money management dictates that you not only understand what you’re paying for but also actively seek out ways to optimize that cost, whether through savvy negotiation of the cap cost or leveraging manufacturer incentives. Before committing to a lease, take the time to meticulously review all terms, understand end-of-lease obligations, and calculate the total financial commitment. With this knowledge, you can transform the often-opaque process of leasing into a transparent, advantageous financial decision that serves your transportation needs and personal finance goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.