Understanding exactly how much money flows into your bank account each month is the cornerstone of financial literacy. While the question “how do you calculate monthly income” might seem straightforward, the answer varies significantly depending on whether you are a salaried employee, an hourly worker, or a freelance entrepreneur. Calculating this figure accurately is not merely an academic exercise; it is a vital step for creating a sustainable budget, applying for credit, and planning for long-term wealth.

In this guide, we will explore the nuances of income calculation, the difference between gross and net figures, and how to account for the complexities of modern earnings.

Understanding the Fundamentals: Gross vs. Net Income

Before diving into the mathematics of your paycheck, it is essential to distinguish between the two primary types of income: gross and net. Failing to understand this distinction is one of the most common mistakes in personal finance management.

Defining Gross Monthly Income

Gross monthly income is the total amount of money you earn before any taxes, benefits, or other deductions are taken out. If you are a salaried employee, this is typically 1/12th of your annual offer letter. For those applying for a mortgage or a car loan, lenders usually ask for your gross income because it represents your total earning power. However, basing your daily lifestyle expenses on your gross income is a recipe for financial distress, as it does not reflect the actual cash available to you.

The Impact of Taxes and Deductions (Net Income)

Net income, often referred to as “take-home pay,” is the amount that actually hits your bank account. To calculate this, you must subtract several variables from your gross pay:

- Federal and State Income Taxes: These are mandatory withholdings based on your tax bracket.

- FICA Taxes: This includes Social Security and Medicare contributions.

- Health Insurance Premiums: If your employer provides benefits, your portion of the premium is usually deducted pre-tax.

- Retirement Contributions: Deductions for 401(k) or 403(b) plans.

- Garnishments or Other Fees: Any legal obligations or union dues.

Why the Distinction Matters for Your Budget

For the purpose of monthly budgeting, your net income is the only figure that truly matters. Using your gross income to plan your rent and grocery spending will leave you with a significant deficit every month. A professional approach to financial planning involves using your gross income for “big picture” ratios (like debt-to-income) and your net income for day-to-day cash flow management.

Calculating Income for Different Employment Types

Not every worker receives a consistent paycheck on the first of the month. The method you use to calculate your monthly average depends heavily on how you are compensated.

Fixed Salaried Employees (Annual to Monthly)

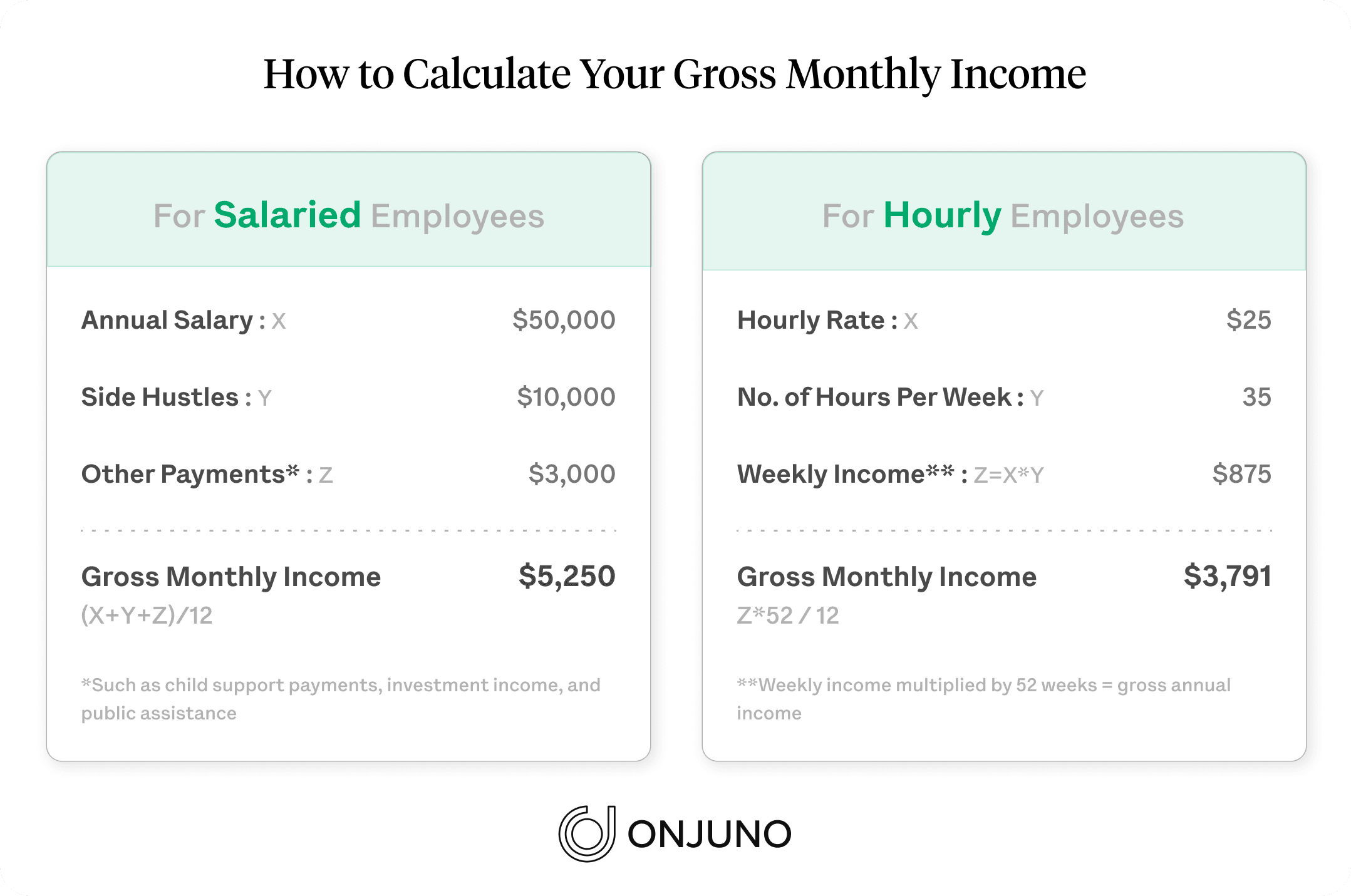

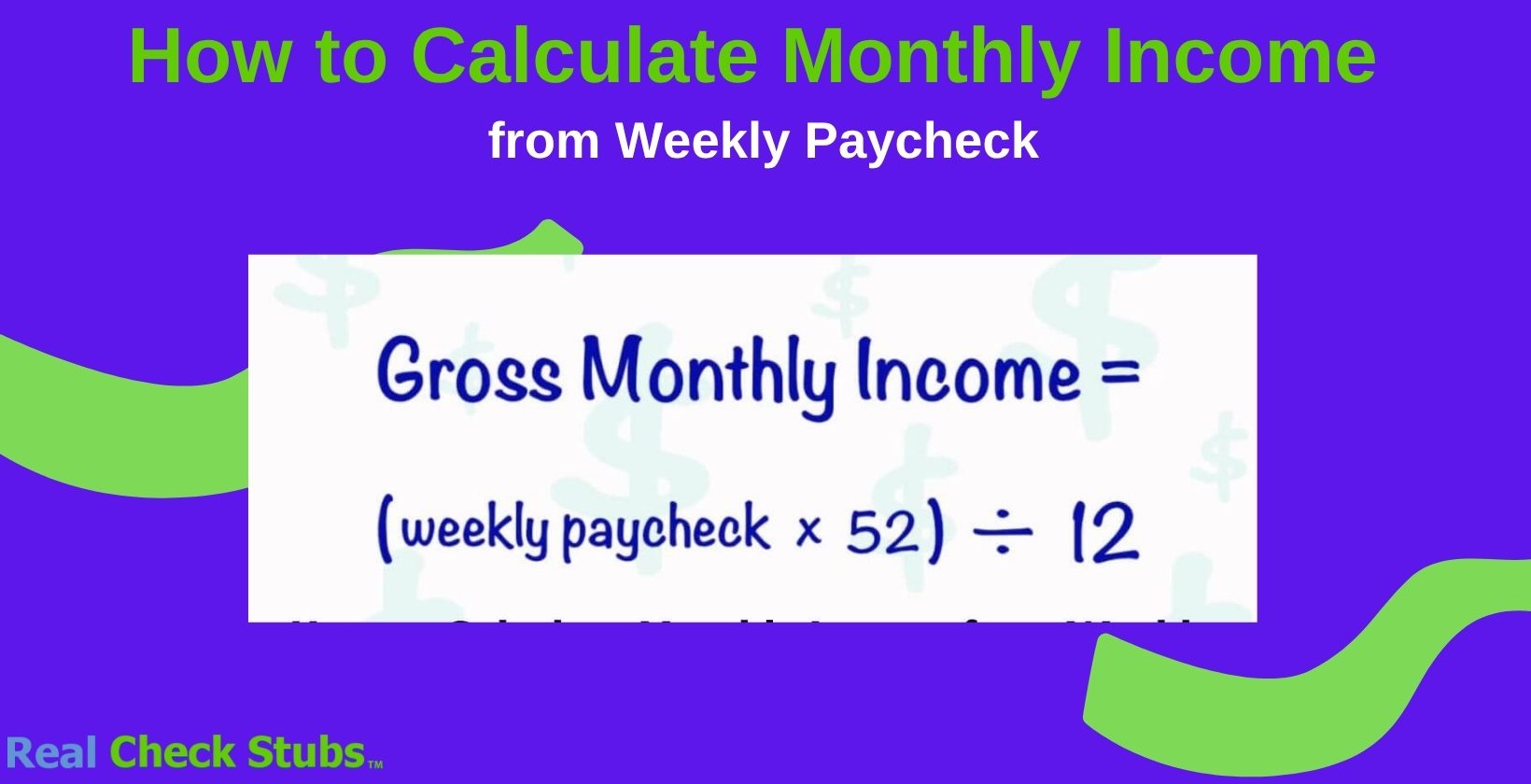

For those with a set annual salary, the calculation is the most stable. If you earn $72,000 a year, your gross monthly income is $6,000 ($72,000 / 12). However, many companies pay bi-weekly (every two weeks) rather than semi-monthly (twice a month).

If you are paid bi-weekly, you will receive 26 paychecks a year. To find your average monthly net income, multiply one paycheck by 26 and divide by 12. This method accounts for the “extra” two months a year where you receive three paychecks instead of two—a common windfall that many people use for savings or debt repayment.

Hourly Workers and Overtime Considerations

For hourly employees, the calculation requires a more granular look at historical data. The formula is:

(Hourly Rate x Hours Per Week) x 52 weeks / 12 months.

If your hours fluctuate, it is best to look at the last three to six months of paystubs to find a “weighted average.” Be cautious with overtime. Unless overtime is guaranteed and consistent, financial experts recommend excluding it from your baseline monthly income calculation. Treat overtime pay as a “bonus” for savings or investments rather than a reliable source for fixed expenses like rent.

Freelancers, Gig Workers, and Variable Income

Calculating income for the self-employed is the most complex task. Because income can swing wildly from month to month, using a single month as a benchmark is dangerous. Instead, professionals recommend a “trailing 12-month” average.

Sum your total net profit (revenue minus business expenses) over the last year and divide by 12. For those in their first year of business, use a “conservative floor”—calculate the lowest amount you’ve earned in a month over the last six months and use that as your budgeting baseline. This ensures that even during a “dry” month, your essential expenses are covered.

Incorporating Additional Revenue Streams

In today’s economy, many individuals have “fragmented” income. Your primary job might be your largest source of funds, but it may not be the only one. To get a true picture of your monthly financial health, you must aggregate all sources.

Investment Dividends and Interest

If you have a significant brokerage account or high-yield savings account, you may be generating passive income. While many choose to reinvest these funds, they still count toward your total monthly income. To calculate this, look at your annual 1099-INT or 1099-DIV forms from the previous year. Divide the total by 12 to find the monthly contribution. However, if these funds are in a locked retirement account like an IRA, they should generally not be counted as “current” monthly income.

Rental Income and Passive Ventures

For those who own real estate, rental income is a significant factor. However, you should never count the full rent check as income. You must subtract the mortgage, property taxes, insurance, and a “maintenance reserve” (usually 10% of the rent). The remaining “cash flow” is your actual monthly income from the property.

Side Hustles and Bonuses

Seasonal bonuses, commissions, and side gigs (like ride-sharing or consulting) should be calculated separately. Because these are often taxed at a different effective rate or require self-employment tax (around 15.3% in the U.S.), the net amount is often lower than expected. Calculate the average of these “extra” streams over a six-month period to determine a reliable monthly addition to your budget.

Practical Methods and Tools for Accurate Calculation

Precision is the enemy of financial stress. Once you understand the formulas, you need a system to track these numbers consistently.

Manual Calculation and Spreadsheets

A simple Excel or Google Sheets document is often the most effective tool. Create columns for “Source,” “Gross Amount,” “Deductions,” and “Net Deposit.” By updating this monthly, you can see trends in your income. This is particularly helpful for tracking how much of your income is being lost to “lifestyle creep” or where tax withholdings might need adjustment.

Leveraging Financial Software and Apps

Modern fintech tools can automate much of this process. Apps that link to your bank accounts can automatically categorize deposits as “Income.” These tools are excellent for identifying your “Burn Rate” (how much you spend versus how much you earn). However, be wary of apps that misidentify internal transfers or tax refunds as “monthly income.” Always perform a manual “sanity check” on automated data.

Organizing Documentation

To ensure your calculations are accurate—especially when preparing for a loan application—maintain a digital folder of your financial documents. This should include:

- Your last three months of paystubs.

- The last two years of W-2s or 1099s.

- Bank statements showing direct deposits.

- Profit and Loss (P&L) statements if you are self-employed.

Using Your Monthly Income Figure for Financial Growth

The ultimate goal of calculating your monthly income is to leverage that information for better decision-making. Once you have a firm number, you can evaluate your financial standing through several key metrics.

Debt-to-Income Ratio (DTI) Assessment

Lenders use your DTI to determine your creditworthiness. It is calculated by dividing your total monthly debt payments (rent, car loans, student loans, credit card minimums) by your gross monthly income. A DTI of 36% or lower is generally considered healthy. If your calculation shows a higher ratio, your primary financial goal should be debt reduction or income scaling.

Optimizing Your Savings Rate

Once you know your net monthly income, you can determine your savings rate. Financial experts often suggest the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and debt repayment. If you don’t know your exact monthly income, it is impossible to know if you are hitting that 20% target. By accurately calculating your income, you can identify “surplus” cash that can be moved into high-growth investments or emergency funds.

Planning for Future Financial Milestones

Whether you are saving for a down payment on a home, planning a career pivot, or preparing for retirement, your monthly income is the engine that drives your progress. Knowing this figure allows you to create a “reverse budget”—where you decide how much you want to save first, and then fit your lifestyle into the remaining income.

In conclusion, calculating your monthly income is more than just a math problem; it is an act of taking control of your future. By distinguishing between gross and net, accounting for variable streams, and using the right tools, you move from financial ambiguity to a position of professional financial management. This clarity is the first step toward building lasting wealth and achieving true financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.