Understanding how to calculate interest payable is a fundamental skill for anyone managing personal finances, operating a business, or making investment decisions. Whether you’re taking out a loan, using a credit card, or financing an asset, interest payable represents the cost of borrowing money. Ignoring this crucial calculation can lead to significant financial strain, whereas mastering it empowers you to make informed decisions, minimize costs, and optimize your financial strategy.

This comprehensive guide will demystify the process of calculating interest payable, breaking down the core concepts, common formulas, practical applications, and the tools available to simplify this essential financial task. By the end, you’ll have a clear understanding of how interest accrues and how to accurately determine your financial obligations.

1. The Fundamentals of Interest Payable

Before diving into calculations, it’s essential to grasp what interest payable truly is and the key components that drive its computation. In essence, interest payable is the amount of interest owed on a debt, loan, or credit facility over a specific period. It’s the price paid by a borrower to a lender for the use of their money.

What is Interest Payable?

Interest payable represents a liability on your financial statements, indicating money that you owe to creditors due to borrowing. It accrues over time based on the principal amount borrowed, the interest rate charged, and the duration of the loan. For businesses, it’s a critical expense that impacts profitability. For individuals, it dictates the true cost of mortgages, car loans, student loans, and credit card debt.

Key Components of Interest Calculation

Three primary variables dictate the amount of interest payable:

- Principal (P): This is the initial amount of money borrowed or the face value of the loan. It’s the base upon which interest is calculated.

- Interest Rate (R): Expressed as a percentage, this is the cost of borrowing the principal amount, typically on an annual basis. It’s crucial to distinguish between annual percentage rate (APR) and annual equivalent rate (AER), especially when compounding is involved. The rate must always be converted to a decimal (e.g., 5% becomes 0.05) and adjusted for the compounding period if it’s not annual.

- Time (T): This refers to the duration for which the money is borrowed, usually expressed in years. If the interest is calculated for a period less than a year, time will be a fraction of a year (e.g., 6 months would be 0.5 years).

Simple vs. Compound Interest

The method by which interest is applied significantly impacts the total amount payable.

- Simple Interest: Calculated only on the original principal amount. It remains constant throughout the loan term, assuming no changes to the principal.

- Compound Interest: Calculated on the principal amount and on the accumulated interest from previous periods. This “interest on interest” effect can lead to a much larger total interest payable over time, making it a powerful force for both savings (when you’re the lender) and debt (when you’re the borrower). Most modern loans, especially long-term ones like mortgages and credit cards, use compound interest.

2. Core Formulas for Calculating Interest Payable

Understanding the core formulas is the cornerstone of accurately calculating interest payable. While calculators and software automate much of this, knowing the underlying math provides invaluable insight.

Calculating Simple Interest Payable

Simple interest is the most straightforward to calculate. It’s often used for short-term loans or bonds where interest is paid out periodically rather than added back to the principal.

The formula for simple interest is:

I = P * R * T

Where:

- I = Total Interest Payable

- P = Principal Amount

- R = Annual Interest Rate (as a decimal)

- T = Time (in years)

Example:

You borrow $10,000 at a simple interest rate of 6% per year for 3 years.

I = $10,000 * 0.06 * 3

I = $1,800

So, the total interest payable would be $1,800. Your total repayment would be $10,000 (principal) + $1,800 (interest) = $11,800.

Calculating Compound Interest Payable

Compound interest is more complex due to its iterative nature, but the formula accounts for this. It’s crucial to know the compounding frequency (annually, semi-annually, quarterly, monthly, daily).

The formula for the future value of a compounded loan (Principal + Interest) is:

A = P (1 + R/n)^(nt)

Where:

- A = Amount after time T (Principal + Total Interest)

- P = Principal Amount

- R = Annual Interest Rate (as a decimal)

- n = Number of times interest is compounded per year

- t = Time (in years)

To find only the interest payable, subtract the principal from the total amount: Total Interest = A – P

Example:

You borrow $10,000 at an annual interest rate of 6%, compounded monthly, for 3 years.

P = $10,000

R = 0.06

n = 12 (compounded monthly)

t = 3

First, calculate A:

A = $10,000 (1 + 0.06/12)^(12*3)

A = $10,000 (1 + 0.005)^(36)

A = $10,000 (1.005)^36

A = $10,000 * 1.196689

A ≈ $11,966.89

Then, calculate total interest payable:

Total Interest = $11,966.89 – $10,000

Total Interest = $1,966.89

Notice how monthly compounding results in more interest ($1,966.89) than simple interest ($1,800) over the same period, illustrating the power of compounding.

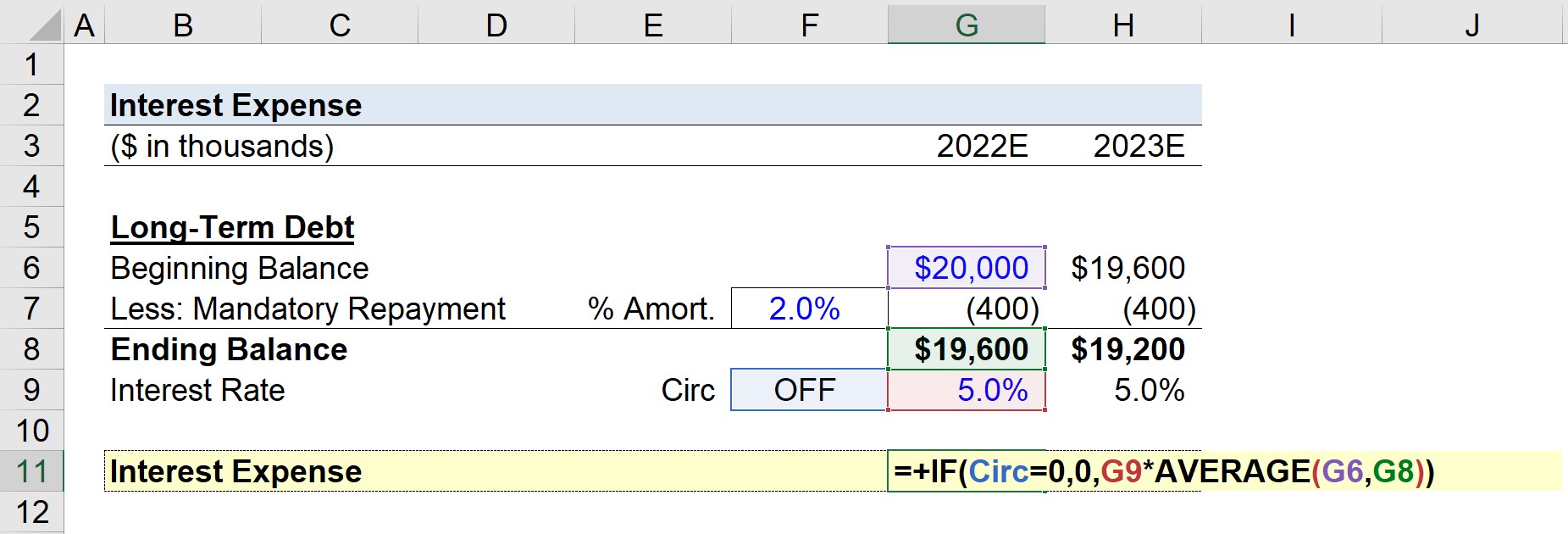

Amortization Schedules

For installment loans like mortgages or car loans, which involve regular, fixed payments over time, interest payable is best understood through an amortization schedule. This table breaks down each payment into its principal and interest components. Early in the loan term, a larger portion of your payment goes towards interest, while later, more goes towards reducing the principal.

Creating an amortization schedule manually is tedious but can be done with a loan payment formula:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount

- i = Monthly Interest Rate (Annual rate / 12)

- n = Total Number of Payments (Loan term in years * 12)

Once you have the monthly payment (M), you can construct the schedule:

- Interest for the period: Outstanding Principal * Monthly Interest Rate (i)

- Principal paid in the period: Monthly Payment (M) – Interest for the period

- New Outstanding Principal: Previous Outstanding Principal – Principal paid in the period

This iterative process shows how the interest payable gradually decreases as the principal is paid down over the loan’s life.

3. Practical Applications and Scenarios

The calculation of interest payable manifests differently across various financial products. Understanding these nuances is key to managing your debt effectively.

Personal Loans and Mortgages

These are typically long-term, fixed-installment loans using amortization. The interest payable each month will decrease as the principal balance shrinks. Lenders provide amortization schedules, but understanding how to interpret them or generate your own (even a simplified one) is empowering. Key considerations include the total interest paid over the life of the loan and how extra principal payments can significantly reduce interest.

Credit Cards

Credit cards operate on a revolving credit basis, meaning the principal balance fluctuates. Interest is typically compounded daily, but applied monthly. If you pay your balance in full by the due date, you usually avoid interest charges (the grace period). However, if you carry a balance, interest accrues rapidly on the average daily balance. The high APRs on credit cards make them one of the most expensive forms of debt if not managed carefully.

Business Loans and Lines of Credit

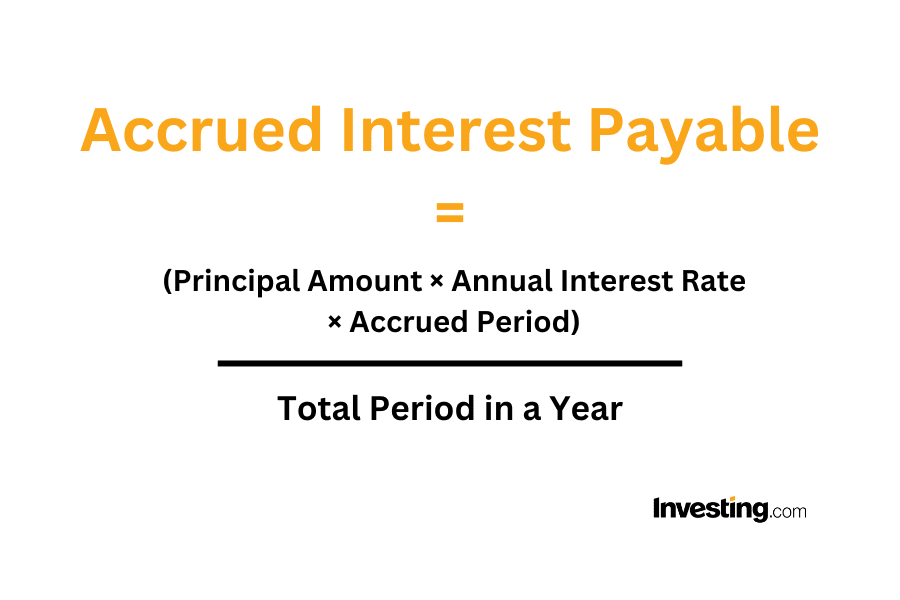

Businesses use various forms of debt, from term loans (often amortized) to lines of credit (revolving, like credit cards, but typically with lower rates). Understanding interest payable is vital for cash flow management, budgeting, and financial reporting. Accrued interest payable on a balance sheet indicates an obligation that needs to be settled, impacting the company’s liabilities and expenses. For businesses, interest expense can also be tax-deductible, adding another layer of calculation.

4. Tools and Resources for Calculation

While the formulas provide the theoretical framework, practical application often involves using tools that automate the calculations, reduce errors, and provide clear visualizations.

Spreadsheets (Excel, Google Sheets)

Spreadsheets are incredibly versatile for calculating interest payable. You can set up custom amortization schedules, calculate simple or compound interest for various scenarios, and even model different payment strategies. Functions like FV (Future Value), PMT (Payment), IPMT (Interest Payment), and PPMT (Principal Payment) in Excel or Google Sheets are specifically designed for these calculations.

Online Calculators

Numerous free online interest and loan calculators are available. These tools are excellent for quick estimates, comparing different loan offers, or understanding the impact of varying interest rates and terms. Simply input the principal, rate, and time, and the calculator provides the interest payable, total repayment, and often a basic amortization breakdown.

Financial Software and Apps

Personal finance management software (e.g., Quicken, Mint) and budgeting apps often include features to track loans, display interest accrual, and even project future interest payments. For businesses, accounting software (e.g., QuickBooks, Xero) automatically handles interest expense tracking and reporting, integrating it directly into financial statements. These tools offer a holistic view of your financial obligations and performance.

5. Impact and Management of Interest Payable

Beyond just calculating the numbers, understanding the impact of interest payable and actively managing it is crucial for long-term financial health.

Financial Planning and Budgeting

Accurate calculation of interest payable allows for precise financial planning. For individuals, it helps in budgeting monthly expenses, understanding the true cost of debt, and setting realistic payoff goals. For businesses, it informs cash flow forecasts, profit projections, and debt-to-equity ratios. Including interest payable as a line item in your budget prevents surprises and ensures funds are allocated appropriately.

Strategies for Reducing Interest Costs

Once you know how interest is calculated, you can develop strategies to minimize the amount you pay:

- Make Extra Payments: Directing extra funds towards the principal balance (especially on amortized loans) reduces the base on which future interest is calculated, saving you substantial amounts over the loan term.

- Refinance: If interest rates drop or your credit score improves, refinancing a loan at a lower rate can significantly reduce your interest payable.

- Debt Consolidation: Combining multiple high-interest debts (like credit cards) into a single loan with a lower interest rate can simplify payments and reduce overall interest costs.

- Pay Off High-Interest Debts First: Focus on debts with the highest interest rates (e.g., credit cards) using strategies like the “debt avalanche” method to minimize total interest paid.

- Understand Terms and Conditions: Always read the fine print of any loan agreement to understand the interest rate, compounding frequency, penalties, and any hidden fees.

Tax Implications of Interest Payable

For businesses, interest expense is typically tax-deductible, reducing taxable income. This is a significant consideration in financial planning and can effectively lower the net cost of borrowing. For individuals, interest on certain loans, like mortgages (up to a limit) or student loans, may also be tax-deductible. Understanding these implications can lead to further financial optimization. However, interest on personal consumer debt, like credit cards or car loans, is generally not tax-deductible.

Conclusion

Calculating interest payable is more than just a mathematical exercise; it’s a fundamental aspect of financial literacy and responsible money management. Whether you’re dealing with simple or compound interest, personal loans or business debt, the ability to accurately determine your interest obligations provides clarity and control. By utilizing the formulas, leveraging available tools, and implementing strategic management techniques, you can minimize the cost of borrowing, accelerate debt repayment, and build a more secure financial future. Empower yourself by understanding every dollar you pay and why you pay it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.