Navigating the world of car loans can often feel like deciphering a complex financial puzzle. Among the various terms thrown around—interest rate, principal, loan term, monthly payment—one stands out as the ultimate arbiter of a loan’s true cost: the Annual Percentage Rate, or APR. Far more encompassing than a simple interest rate, APR provides a holistic view of what you’ll pay to borrow money for your vehicle. Understanding how to calculate it, or at least how to interpret it, is paramount for making informed financial decisions and securing the best deal.

This guide will demystify the APR for car loans, explaining its components, how it’s derived, and why it’s the most critical figure to consider when comparing financing options. By the end, you’ll not only understand the “how” but also the “why” behind maximizing your savings on your next car purchase.

Understanding APR: More Than Just the Interest Rate

To truly grasp the cost of a car loan, it’s essential to look beyond the advertised interest rate and focus on the Annual Percentage Rate (APR). While often used interchangeably by the uninformed, these two figures represent distinct aspects of borrowing.

What is APR? (Annual Percentage Rate)

The Annual Percentage Rate (APR) represents the true annual cost of borrowing money, expressed as a single percentage. Unlike a nominal interest rate, which only accounts for the cost of borrowing the principal amount, APR incorporates both the interest rate and certain additional fees and charges associated with the loan. It standardizes the cost of borrowing across different lenders, making it a powerful tool for comparison. Essentially, it’s the effective interest rate you’ll pay over the life of the loan when all relevant costs are factored in.

Components of APR

The nominal interest rate is undoubtedly the largest component of APR, but it’s not the only one. Lenders often charge various fees that, while seemingly small, can significantly inflate the total cost of the loan. These fees are “annualized” and folded into the APR calculation, providing a comprehensive picture. Common fees included in a car loan’s APR might include:

- Loan Origination Fees: A fee charged by the lender for processing a new loan application.

- Documentation Fees: Fees for preparing and processing loan documents.

- Processing Fees: General administrative charges.

- Certain Broker Fees: If a broker is involved in arranging the loan.

- Credit Report Fees: While sometimes paid upfront, if rolled into the loan, they contribute to APR.

It’s crucial to note that not all fees are included in APR. For instance, late payment fees, prepayment penalties (if applicable), or third-party costs like title and registration fees or extended warranty premiums not required by the lender are typically excluded. The key distinction is whether the fee is a condition of obtaining the credit itself.

Why APR Matters for Car Loans

For car buyers, understanding and comparing APRs is invaluable. Imagine two loan offers:

- Offer A: 5.0% interest rate with a $500 origination fee.

- Offer B: 5.2% interest rate with no origination fee.

Without considering APR, Offer A might initially seem more attractive due to its lower nominal interest rate. However, when that $500 fee is factored into Offer A’s APR, it might actually push its effective annual cost higher than Offer B’s 5.2%. APR allows you to make an “apples-to-apples” comparison between different loan products, regardless of how lenders structure their fees. It ensures transparency, helping you identify which loan truly offers the best value and minimizing the total amount you’ll pay over time.

The Mechanics of APR Calculation (Simplified)

While the precise mathematical formula for APR can be complex, involving actuarial science and present value calculations, the core concept revolves around equating the total value of your payments to the initial loan amount, while accounting for all included fees. For practical purposes, understanding the inputs and the general effect of fees is more important than memorizing an intricate formula.

The Basic Formula (and its complexities)

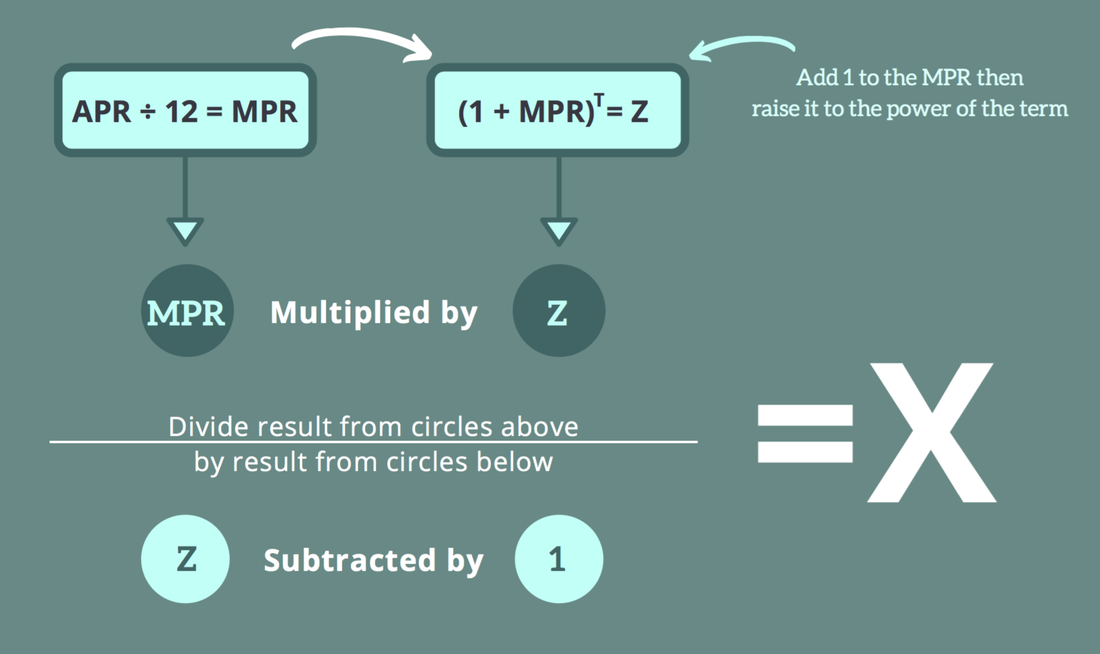

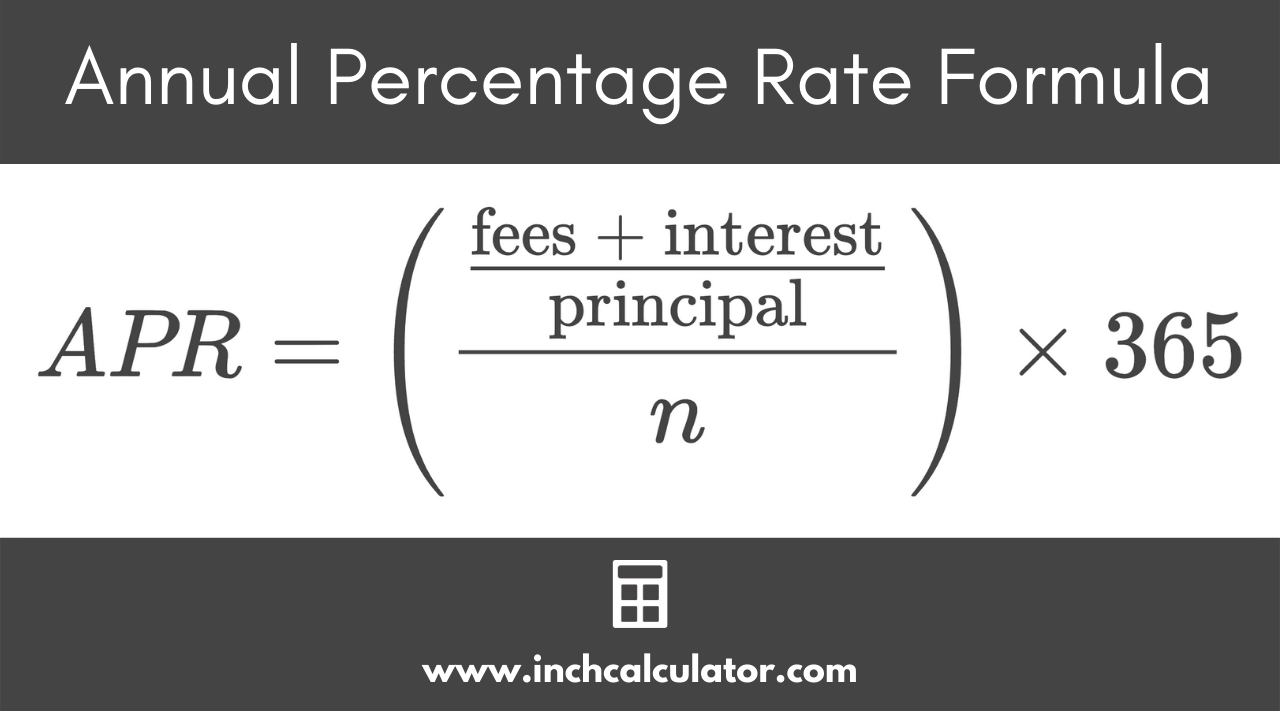

The most common method for calculating APR is based on the Truth in Lending Act (TILA) and involves finding the discount rate that equates the present value of all future payments to the net amount of credit advanced. This is often an iterative process that requires financial calculators or software to solve accurately, as there isn’t always a simple algebraic solution for “r” (the APR) in the equation for an annuity:

$$PV = sum_{t=1}^{N} frac{PMT}{(1 + r)^t}$$

Where:

- PV = Present Value (the loan amount minus upfront fees)

- PMT = Monthly Payment

- r = Monthly periodic rate (APR / 12)

- N = Total number of payments

However, for consumers, the objective isn’t to derive the formula but to understand how the various inputs contribute to the final APR figure disclosed by the lender.

Key Variables in APR Calculation

Several critical pieces of information are fed into any APR calculation. Understanding these variables will help you both anticipate your potential APR and scrutinize loan offers.

- Principal Amount (Loan Amount): This is the initial sum of money you borrow to purchase the car, after any down payment. A larger principal means more interest accrues, though it doesn’t directly change the rate itself unless a higher amount means more risk or different loan tiers.

- Interest Rate (Nominal): This is the base percentage rate at which the lender charges interest on the principal. It’s the starting point before fees are factored in to arrive at the APR.

- Loan Term (Duration): The length of time, typically in months, over which you agree to repay the loan (e.g., 36, 48, 60, 72, or 84 months). Longer terms often mean lower monthly payments but typically result in paying more total interest over the life of the loan, and sometimes even a slightly higher APR due to increased risk for the lender.

- Fees (Origination, Documentation, etc.): As discussed, these are the charges added by the lender that are rolled into the cost of the loan. The higher these fees are relative to the loan principal, the greater their impact on pushing the APR above the nominal interest rate.

- Payment Schedule: Most car loans have a monthly payment schedule. The frequency and timing of payments affect the compounding of interest, though for standard monthly payments, this is usually a fixed assumption.

Illustrative Example (Simplified)

Let’s consider a simplified scenario to understand how fees affect APR.

Suppose you are borrowing $20,000 for a car loan over 60 months (5 years) with a nominal interest rate of 4.5%.

Scenario 1: No Fees

If there were absolutely no fees, your monthly payment would be approximately $372.89. The APR would effectively be 4.5%, matching the nominal interest rate.

Scenario 2: With Fees

Now, let’s say the lender charges a $300 origination fee and a $50 documentation fee, totaling $350 in fees. These fees are often rolled into the loan or deducted from the principal amount disbursed. For the purpose of APR calculation, these fees effectively reduce the net amount of credit you receive while you still pay back the full $20,000 (plus interest).

If you are paying $372.89 per month for a loan that effectively cost you only $19,650 (i.e., $20,000 – $350 in fees) but you’re paying back as if it were $20,000, your true annual cost of borrowing is higher. Using a financial calculator or a spreadsheet, we would find that paying $372.89 per month on an initial effective credit of $19,650 over 60 months results in an APR closer to 4.95%.

This simple example demonstrates that even seemingly small fees can elevate the APR above the nominal interest rate, highlighting why APR is the more comprehensive metric.

Practical Approaches to Calculating or Estimating Your Car Loan APR

While you’re not expected to perform complex actuarial calculations, several practical methods can help you determine or estimate the APR for your car loan. The good news is that for consumers, the work is largely done by lenders and online tools.

Using Online APR Calculators

The easiest and most common way to estimate or verify an APR is through online calculators. Numerous reputable financial websites, banks, and loan aggregators offer free APR calculators. These tools typically require you to input:

- The loan principal amount.

- The nominal interest rate.

- The loan term in months.

- Any upfront fees included in the loan.

Once you enter this information, the calculator will provide an estimated APR. These calculators are excellent for comparing different scenarios and understanding the impact of various fees on your overall borrowing cost. Just ensure you’re using a calculator designed for loans with upfront fees, not just simple interest calculators.

Leveraging Loan Disclosure Documents

Perhaps the most direct and legally mandated way to find your car loan’s APR is to simply look at the official loan documents provided by the lender. Under the Truth in Lending Act (TILA), lenders are legally required to disclose the APR clearly and conspicuously before you sign any agreement. This disclosure ensures transparency and allows you to compare offers effectively.

When you receive a loan offer or a loan agreement, look for a section titled “Finance Charge,” “Total of Payments,” and most importantly, “Annual Percentage Rate (APR).” This figure is the official, legally binding APR that includes all the federally mandated costs. Always compare the APRs from different lenders, as this is the most reliable metric for cost comparison.

Spreadsheet Software (Excel/Google Sheets)

For those who are comfortable with spreadsheets, tools like Microsoft Excel or Google Sheets offer functions that can calculate APR. The RATE function is particularly useful for this.

The RATE function requires inputs such as:

nper: Total number of payment periods (loan term in months).pmt: The payment made each period (a negative value, as it’s an outflow).pv: The present value (the net amount of credit received, i.e., loan principal minus included fees).fv: Future value (usually 0 for a fully amortized loan).type: When payments are due (0 for end of period, 1 for beginning; usually 0 for loans).

By inputting these values, the RATE function will return the periodic interest rate. You then multiply this periodic rate by the number of periods in a year (e.g., 12 for monthly payments) to get the APR. This method offers a robust way to verify or calculate APR if you have all the necessary financial details of a loan offer.

Factors Influencing Your Car Loan APR

While the calculation methods explain how APR is derived, it’s equally important to understand the factors that influence the APR you’re offered in the first place. These elements determine your creditworthiness and the perceived risk you pose to a lender.

Credit Score and History

This is arguably the most significant factor. Lenders use your credit score (e.g., FICO, VantageScore) as a primary indicator of your financial reliability and likelihood of repaying debt. Borrowers with excellent credit scores (typically 750+) are considered low-risk and are generally offered the lowest APRs. Conversely, those with fair or poor credit will likely face higher APRs, reflecting the increased risk the lender is taking. A strong credit history, free of delinquencies and defaults, also demonstrates responsible financial behavior.

Loan Term

The length of your loan also plays a role. Shorter loan terms (e.g., 36 or 48 months) often come with slightly lower APRs compared to longer terms (e.g., 72 or 84 months). This is because a shorter term reduces the lender’s exposure to risk over time. While longer terms result in lower monthly payments, they often accrue more total interest and may come with a slightly higher APR.

Down Payment Amount

Making a substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. With less money at stake, lenders may be more willing to offer a lower APR. A larger down payment also signals financial stability and commitment, further enhancing your appeal as a borrower.

Debt-to-Income Ratio (DTI)

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to manage additional debt. A lower DTI (meaning you have more disposable income relative to your debt obligations) indicates less financial strain and a higher likelihood of loan repayment, potentially leading to a more favorable APR.

New vs. Used Car

The type of car you purchase can sometimes influence the APR. New cars, especially those from popular manufacturers, might qualify for special promotional APRs offered by captive finance companies (e.g., Toyota Financial Services, Ford Credit). Used cars, due to their typically lower value and higher depreciation risk, might carry slightly higher APRs, though this is not always a hard and fast rule and depends heavily on the car’s age, mileage, and condition.

Lender Type

Different types of lenders have different business models and risk appetites.

- Banks: Traditional banks often offer competitive rates to customers with strong credit.

- Credit Unions: Member-owned credit unions are known for often providing some of the lowest APRs, as their primary goal is to serve members rather than maximize shareholder profit.

- Dealership Financing: While convenient, dealership financing (often through a network of third-party lenders) can sometimes offer higher APRs, though they can also be competitive, especially for manufacturer incentives.

- Online Lenders: A growing segment, online lenders can offer quick approvals and competitive rates, particularly for those with good credit.

Shopping around across these different lender types is crucial for finding the best possible APR.

Beyond Calculation: Strategizing for a Better Car Loan APR

Understanding how APR is calculated and what influences it is the first step. The next is to proactively strategize to secure the lowest possible APR, thereby saving you hundreds or even thousands of dollars over the life of your car loan.

Improving Your Credit Score

Since your credit score is a primary determinant of your APR, take steps to improve it before applying for a car loan. Pay all your bills on time, reduce existing debt, avoid opening new lines of credit unnecessarily, and dispute any errors on your credit report. Even a few points’ improvement can make a difference in the APR you’re offered.

Shopping Around for Lenders

Never take the first loan offer you receive. Apply for pre-approvals from at least 3-5 different lenders (banks, credit unions, online lenders). These pre-approvals typically involve a “soft” credit inquiry, which doesn’t harm your score, and give you concrete APR offers to compare. This competitive shopping forces lenders to offer their best rates to win your business. Presenting a pre-approval from one lender can also serve as leverage when negotiating with another, including dealership financing.

Negotiating Fees

Some loan fees, particularly those from dealerships, might be negotiable. Understand which fees are legitimate and which are discretionary. Question every charge and be prepared to ask for reductions or even waivers. Remember, every dollar saved in fees directly translates to a lower overall cost of your loan, and potentially a lower APR if the fee is folded in.

Considering a Shorter Loan Term (if affordable)

While longer terms mean lower monthly payments, they almost always result in more total interest paid and potentially a higher APR. If your budget allows, opt for the shortest loan term you can comfortably afford. This not only reduces the total interest but often secures a more favorable APR from the outset.

Making a Substantial Down Payment

A larger down payment reduces the principal amount you need to borrow, which can lead to a lower APR. It also demonstrates financial discipline and reduces the lender’s risk. Aim for at least 10-20% of the car’s purchase price as a down payment if possible.

Conclusion

The Annual Percentage Rate (APR) is undeniably the most crucial figure to understand when financing a car. It encapsulates not just the nominal interest rate but also other mandatory fees, providing a transparent, apples-to-apples comparison of loan offers. While the underlying calculation can be complex, practical tools like online calculators, official loan disclosures, and even spreadsheet functions make it accessible for consumers.

By understanding the components of APR, recognizing the factors that influence it—such as your credit score, loan term, and down payment—and actively strategizing to improve your lending profile, you empower yourself to secure the most favorable car loan. Armed with this knowledge, you can navigate the car financing landscape with confidence, ultimately saving significant money and making a truly informed decision for your automotive purchase.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.