Investing in the S&P 500 has long been a cornerstone strategy for both novice and seasoned investors seeking broad market exposure and long-term growth. Often lauded as a barometer for the U.S. economy, the S&P 500 index represents the performance of 500 of the largest, most established publicly traded companies in the United States. While you can’t “buy” the index directly like a single stock, you can gain exposure to its performance through various accessible and cost-effective financial instruments. This guide will demystify the process, exploring the primary avenues for S&P 500 investing and providing practical steps to integrate this powerful strategy into your financial portfolio.

The allure of the S&P 500 stems from its inherent diversification and historical track record of resilient long-term returns. By investing in a vehicle that tracks the S&P 500, you are effectively buying a small piece of 500 diverse companies across various sectors—from technology and healthcare to finance and consumer goods. This broad exposure significantly reduces the idiosyncratic risk associated with investing in individual stocks, making it an attractive option for those who believe in the long-term prosperity of the U.S. market without wanting to pick individual winners and losers. Whether your goal is retirement planning, wealth accumulation, or simply a sound investment strategy, understanding how to effectively invest in the S&P 500 is a crucial step towards achieving your financial objectives.

Understanding the S&P 500 and Its Appeal

Before diving into the “how-to,” it’s essential to grasp what the S&P 500 truly represents and why it has earned its prominent place in investment portfolios worldwide. This understanding will underscore the strategic advantages of including it in your financial planning.

What is the S&P 500?

The S&P 500, short for the Standard & Poor’s 500, is a market-capitalization-weighted index of 500 of the largest U.S. publicly traded companies. Compiled by S&P Dow Jones Indices, it aims to be a leading indicator of U.S. equities and a proxy for the U.S. economy. Being “market-capitalization-weighted” means that companies with larger market values (share price multiplied by the number of outstanding shares) have a greater impact on the index’s performance.

The index’s constituents are chosen by a committee based on criteria such as market size, liquidity, and sector representation, ensuring it accurately reflects the broader market. These aren’t necessarily the 500 largest companies by market cap alone but rather a curated selection intended to capture approximately 80% of the total market value of U.S. stocks. From tech giants like Apple and Microsoft to financial powerhouses like JPMorgan Chase and consumer staples like Procter & Gamble, the S&P 500 offers a microcosm of American corporate might.

Why Invest in the S&P 500?

The reasons for the S&P 500’s widespread appeal among investors are compelling and multifaceted:

- Diversification: The most significant advantage is immediate diversification. Instead of betting on a single company, you gain exposure to 500 companies across 11 major sectors. This spreads your risk, meaning that a poor performance from one or a few companies won’t decimate your entire portfolio. It offers a balanced representation of the American economy.

- Historical Performance: Over the long term, the S&P 500 has demonstrated robust performance, averaging approximately 10-12% annual returns (including dividends) since its inception, though past performance is not indicative of future results. This track record makes it an attractive vehicle for long-term wealth accumulation, outperforming many actively managed funds after fees.

- Simplicity & Low Cost: Investing in an S&P 500 tracking fund is a form of passive investing. Instead of analysts and fund managers actively picking stocks, these funds simply aim to mirror the index’s performance. This passive approach typically translates to very low expense ratios (the annual fee charged as a percentage of your investment), which can significantly impact your net returns over decades.

- Reduced Idiosyncratic Risk: By investing in a broad index, you largely eliminate “idiosyncratic risk”—the risk specific to an individual company (e.g., poor management, product failures, scandals). While market risk (the risk that the overall market declines) remains, the highly diversified nature of the S&P 500 mitigates company-specific downturns.

Primary Avenues for Investing in the S&P 500

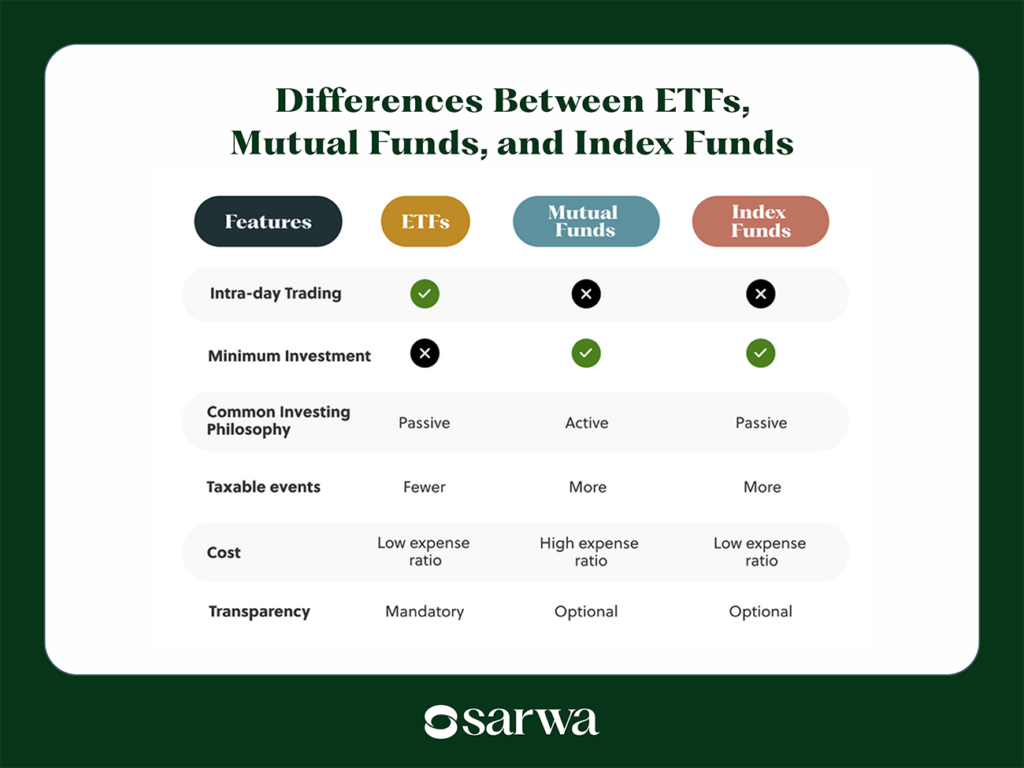

Since you cannot directly purchase the S&P 500 index itself, investors access its performance through financial products designed to mirror its composition and returns. The two most common and efficient methods are Exchange Traded Funds (ETFs) and Index Mutual Funds, with robo-advisors offering a simplified route.

S&P 500 Exchange Traded Funds (ETFs)

S&P 500 ETFs are investment funds that hold the underlying stocks in the S&P 500, aiming to replicate the index’s performance. They are bought and sold like individual stocks on stock exchanges throughout the trading day. This flexibility is a key differentiator from mutual funds.

- What they are: ETFs are a basket of securities that often track an underlying index, in this case, the S&P 500. When you buy an S&P 500 ETF, you are buying a share of a fund that owns a proportionate slice of all 500 companies in the index.

- Key Characteristics:

- Low Expense Ratios: ETFs typically boast very low expense ratios, often below 0.10% annually, making them incredibly cost-efficient for long-term investors.

- Intraday Trading Flexibility: Like stocks, ETFs can be traded throughout the day at market prices, allowing for greater control over entry and exit points compared to mutual funds.

- Liquidity: Popular S&P 500 ETFs are highly liquid, meaning they can be easily bought and sold without significantly impacting their price.

- Transparency: The holdings of ETFs are disclosed daily, offering full transparency into your investment.

- Popular Examples:

- SPDR S&P 500 ETF Trust (SPY): The oldest and one of the largest S&P 500 ETFs, managed by State Street.

- iShares Core S&P 500 (IVV): Managed by BlackRock, known for its low expense ratio.

- Vanguard S&P 500 ETF (VOO): Managed by Vanguard, also celebrated for its very low costs and efficient structure.

- Advantages: Cost-effectiveness, trading flexibility, and potential tax efficiency (due to their creation/redemption mechanism that can minimize capital gains distributions).

S&P 500 Index Mutual Funds

S&P 500 index mutual funds are another popular way to invest in the index. Unlike ETFs, mutual funds are typically purchased directly from the fund provider or through a brokerage at the end-of-day Net Asset Value (NAV).

- What they are: An S&P 500 index mutual fund is a type of investment fund that pools money from many investors to purchase the stocks that make up the S&P 500 index. They are professionally managed, but their objective is to passively track the index rather than trying to beat it.

- Key Characteristics:

- Daily Pricing: Mutual funds are priced only once per day, after the market closes, at their Net Asset Value (NAV).

- Automatic Reinvestment: Many mutual funds offer automatic dividend reinvestment, allowing your earnings to compound effortlessly.

- Minimum Investments: Some index mutual funds, particularly admiral or institutional share classes, may require higher initial minimum investments (e.g., $3,000 for Vanguard’s VFIAX), though investor share classes often have lower or no minimums.

- Automatic Contributions: Easy to set up recurring automatic investments, making dollar-cost averaging simple.

- Popular Examples:

- Vanguard 500 Index Fund Admiral Shares (VFIAX): One of the most well-known and low-cost S&P 500 index funds.

- Fidelity 500 Index Fund (FXAIX): Fidelity’s comparable offering, also with a very low expense ratio.

- Advantages: Simplicity, ideal for long-term investors who prefer a “set-it-and-forget-it” approach, and convenient for setting up regular contributions.

Leveraging Robo-Advisors

For those seeking an even more hands-off approach, robo-advisors offer a streamlined way to invest in diversified portfolios that often include S&P 500 ETFs.

- What they are: Robo-advisors are automated, algorithm-driven financial platforms that provide investment management services with minimal human intervention. They create and manage diversified portfolios tailored to your risk tolerance and financial goals.

- How they integrate S&P 500: Robo-advisors typically construct portfolios using a mix of low-cost ETFs, including S&P 500 ETFs, to achieve broad market exposure. They automate tasks like asset allocation, rebalancing, and dividend reinvestment.

- Benefits:

- Low Management Fees: Robo-advisors typically charge a small annual advisory fee (e.g., 0.25% to 0.50% of assets under management), which is often lower than traditional financial advisors.

- Automatic Rebalancing: They automatically adjust your portfolio to maintain your desired asset allocation, ensuring you stay on track.

- Ease of Use: User-friendly interfaces and automated processes make investing simple, especially for beginners.

- Goal-Based Planning: Many offer tools to help you plan for specific financial goals like retirement or a down payment on a house.

- Examples: Betterment, Wealthfront, Schwab Intelligent Portfolios.

Practical Steps to Begin Your S&P 500 Investment Journey

Once you’ve decided on the investment vehicle that best suits your needs, the actual process of buying into the S&P 500 is straightforward. It primarily involves opening an investment account and then funding it to make your purchase.

Choosing a Brokerage Account

The first critical step is selecting a reputable brokerage firm where you will open an investment account.

- Types:

- Discount Brokers: These offer low-cost trading, a wide range of investment products, and robust online platforms (e.g., Fidelity, Charles Schwab, Vanguard, E*TRADE, Robinhood, M1 Finance). They are suitable for investors who are comfortable making their own investment decisions.

- Full-Service Brokers: These provide comprehensive financial advice, portfolio management, and a wider array of services, often at a higher cost (e.g., Merrill Lynch, Morgan Stanley). They may be suitable for investors who need extensive guidance.

- Considerations:

- Fees: Look for brokers with $0 commission fees for stock and ETF trades. Check for account maintenance fees or inactivity fees.

- Research Tools: Does the platform offer good research resources and analytical tools to help you evaluate funds?

- Customer Service: Is customer support easily accessible and responsive?

- Investment Options: Ensure the broker offers the specific S&P 500 ETFs or mutual funds you’re interested in.

- Account Types: Decide whether you want to open a taxable brokerage account (general investment) or a tax-advantaged retirement account (e.g., Traditional IRA, Roth IRA, 401(k) if your plan allows self-directed brokerage or offers S&P 500 funds).

Funding Your Account

Once your brokerage account is open, you’ll need to deposit money into it.

- Methods: Common funding methods include linking your bank account for an Automated Clearing House (ACH) transfer (which can take a few business days), wire transfers (faster but often with fees), or mailing a check.

- Initial Deposit Requirements: Be aware of any minimum initial deposit requirements set by the brokerage or for specific mutual funds. ETFs typically don’t have minimums beyond the share price.

Selecting Your Investment Vehicle

Based on your preferences for trading flexibility, automation, and minimum investment, choose between an S&P 500 ETF or an S&P 500 index mutual fund.

- ETFs vs. Mutual Funds:

- If you want to trade throughout the day or prefer potentially greater tax efficiency, an ETF might be better.

- If you prefer automatic investments, don’t mind end-of-day pricing, and appreciate the simplicity of automatic dividend reinvestment, a mutual fund could be more suitable.

- Research Expense Ratios: Always prioritize funds with the lowest expense ratios, as these fees directly eat into your returns over time. A difference of even 0.10% can amount to thousands of dollars over decades.

Placing Your Buy Order

Finally, it’s time to make your purchase.

- For ETFs: You’ll typically enter a ticker symbol (e.g., SPY, IVV, VOO) and the number of shares you wish to buy. You can choose between:

- Market Order: Buys shares immediately at the current market price.

- Limit Order: Specifies the maximum price you’re willing to pay, ensuring you don’t overpay if the price suddenly spikes.

- For Mutual Funds: You’ll usually search for the fund by name or ticker (e.g., VFIAX, FXAIX) and specify the dollar amount you wish to invest. The trade will execute at the fund’s NAV at the close of the market.

- Automatic Investments: Consider setting up recurring automatic investments, especially for mutual funds, to implement dollar-cost averaging—a strategy that involves investing a fixed amount regularly, regardless of market fluctuations.

Essential Considerations for S&P 500 Investors

While investing in the S&P 500 is often praised for its simplicity, there are several crucial factors that intelligent investors must consider to optimize their strategy and maximize long-term returns.

Expense Ratios and Fees

The cost of investing might seem small on a percentage basis, but it compounds significantly over time.

- The Ongoing Cost: The expense ratio is the annual fee charged by the fund manager, expressed as a percentage of your investment. For example, an expense ratio of 0.03% means you pay $3 annually for every $10,000 invested.

- Impact on Long-Term Returns: Even a seemingly small difference in expense ratios can lead to substantial differences in your portfolio’s value over decades. Always compare expense ratios and opt for the lowest-cost option among funds that track the S&P 500.

- Other Fees: Be mindful of other potential fees, such as trading commissions (though many brokers offer commission-free ETF trades), account maintenance fees, or mutual fund transaction fees (like load fees, though index funds typically don’t have these).

Tax Implications

Understanding the tax implications of your investments is vital, particularly for long-term wealth growth.

- Capital Gains Tax: When you sell your ETF or mutual fund shares for a profit, you incur capital gains.

- Short-Term Capital Gains: For assets held for one year or less, these are taxed at your ordinary income tax rate, which can be as high as 37%.

- Long-Term Capital Gains: For assets held for more than one year, these are typically taxed at preferential rates (0%, 15%, or 20% depending on your income).

- Dividend Taxation: Funds that track the S&P 500 also pay out dividends from the underlying companies. These dividends are generally taxable in the year they are received, even if reinvested. Qualified dividends are taxed at the long-term capital gains rates.

- Tax-Advantaged Accounts: To mitigate immediate tax burdens, prioritize investing in S&P 500 funds within tax-advantaged accounts like IRAs (Traditional or Roth) or 401(k)s. Contributions to a Traditional IRA or 401(k) are often tax-deductible, and growth is tax-deferred until withdrawal in retirement. Roth accounts offer tax-free growth and withdrawals in retirement.

- Tax-Loss Harvesting: With ETFs, investors in taxable accounts can sometimes engage in tax-loss harvesting, selling an investment at a loss to offset capital gains and potentially a limited amount of ordinary income.

Long-Term Horizon and Dollar-Cost Averaging

S&P 500 investing is fundamentally a long-term strategy, best suited for patient investors.

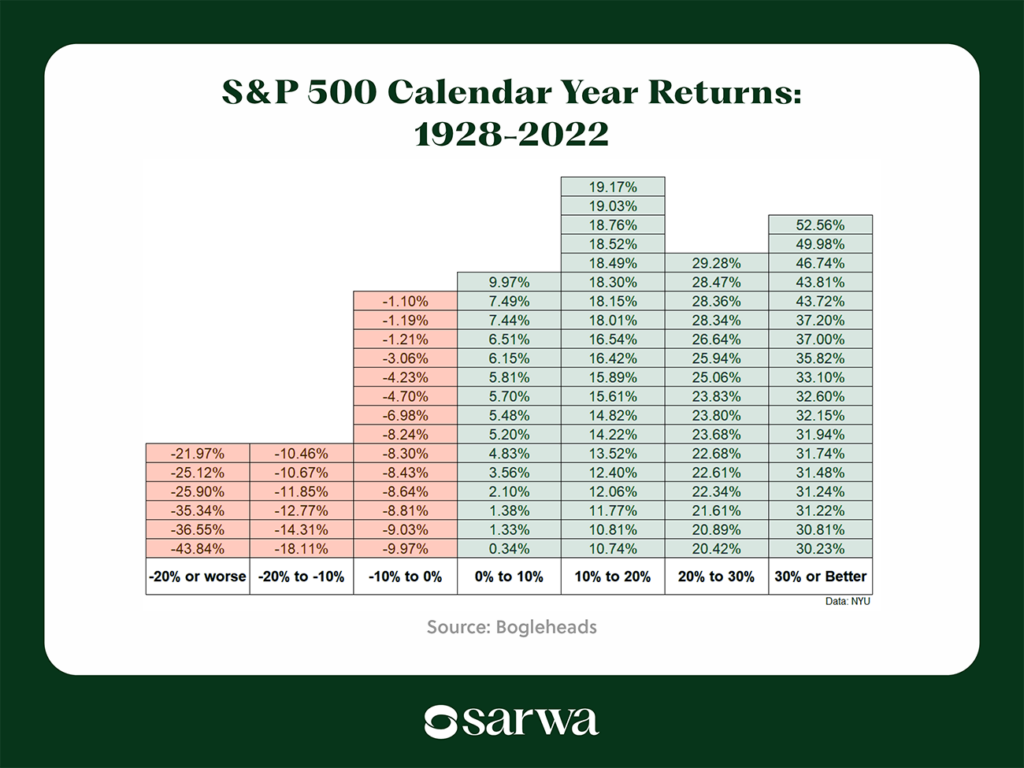

- Long-Term Growth: The S&P 500’s historical performance demonstrates its power over decades, weathering market downturns and recessions to deliver robust average returns. Short-term market fluctuations are normal and should not deter a long-term strategy.

- The Power of Compounding: By consistently reinvesting dividends and capital gains, your earnings begin to earn returns themselves, accelerating wealth accumulation through the magic of compounding. Starting early maximizes the benefit of this phenomenon.

- Dollar-Cost Averaging (DCA): This strategy involves investing a fixed amount of money at regular intervals (e.g., $200 every month), regardless of the market price. DCA helps mitigate the risk of market timing by averaging out your purchase price over time. When prices are low, your fixed amount buys more shares; when prices are high, it buys fewer. This disciplined approach often leads to better long-term results than trying to guess market peaks and valleys.

Risk vs. Reward

While highly diversified, S&P 500 investments are not without risk.

- Market Volatility: The S&P 500 is still subject to market risk, meaning the overall market can experience downturns. Economic recessions, geopolitical events, and other macro factors can lead to significant drops in the index’s value.

- No Guarantees: Past performance is never a guarantee of future results. While the S&P 500 has historically recovered from all major downturns, there’s no assurance this pattern will always hold.

- Staying Invested: The key to navigating market volatility with S&P 500 investments is to maintain a long-term perspective and avoid panic selling during downturns. History shows that those who stay invested and continue to contribute during bear markets are often rewarded when the market recovers. Your risk tolerance should align with your investment horizon and capacity to absorb potential short-term losses.

Investing in the S&P 500 offers a compelling blend of diversification, growth potential, and simplicity. By understanding the underlying index, choosing the right investment vehicle, and adhering to sound financial principles like minimizing fees, leveraging tax advantages, and embracing a long-term, disciplined approach, you can effectively integrate this powerful strategy into your journey toward financial independence. It’s a testament to the enduring strength of the U.S. economy and a strategy that empowers everyday investors to participate in its success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.