Small business loans serve as the lifeblood of the global economy, providing the necessary liquidity for entrepreneurs to scale operations, manage seasonal fluctuations, and invest in long-term growth. At its core, a small business loan is a contractual agreement where a lender provides capital to a business owner, who then agrees to repay the principal amount along with interest and fees over a predetermined period. However, beneath this simple definition lies a complex financial ecosystem governed by risk assessment, credit structures, and strategic capital management.

Understanding the mechanics of these loans is essential for any business owner looking to optimize their balance sheet. Whether you are seeking to bridge a cash flow gap or fund a major acquisition, knowing how the money moves and what lenders look for can mean the difference between financial stability and insolvency.

1. The Financial Mechanics of Lending and Repayment

To understand how small business loans work, one must first understand the fundamental relationship between risk and reward in the financial sector. Lenders—whether they are traditional banks, credit unions, or online fintech platforms—are in the business of selling money. The “price” of that money is the interest rate, which is calculated based on the perceived risk that the borrower might default.

The Relationship Between Lender and Borrower

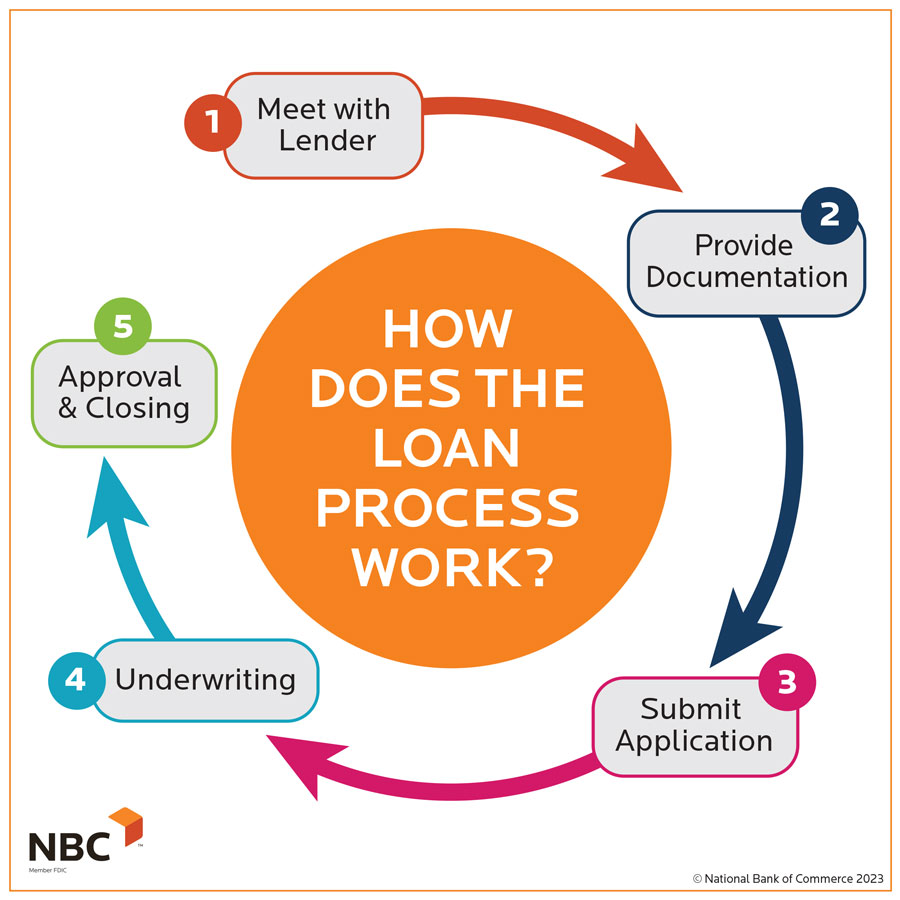

The lending process begins with an underwriting period, during which the lender evaluates the financial health of the business. This involves a deep dive into financial statements, tax returns, and bank statements. From a financial perspective, the lender is looking for “debt service coverage”—the ability of the business’s operating income to cover its debt obligations. Once a loan is approved, the borrower receives a lump sum or access to a credit line, establishing a fiduciary responsibility to return those funds according to the agreed-upon terms.

Principal, Interest, and Amortization Schedules

Every payment made toward a small business loan is typically divided into two parts: principal and interest. The principal is the original amount borrowed, while interest is the cost of borrowing. Most small business loans are “amortized,” meaning the payment schedule is structured so that the borrower pays a fixed amount every month. In the early stages of the loan, a larger portion of the payment goes toward interest. As the principal balance decreases, a larger portion of the payment is applied to the principal. Understanding your amortization schedule is vital for financial planning, as it dictates how quickly you are building equity in your business assets.

Secured vs. Unsecured Financing

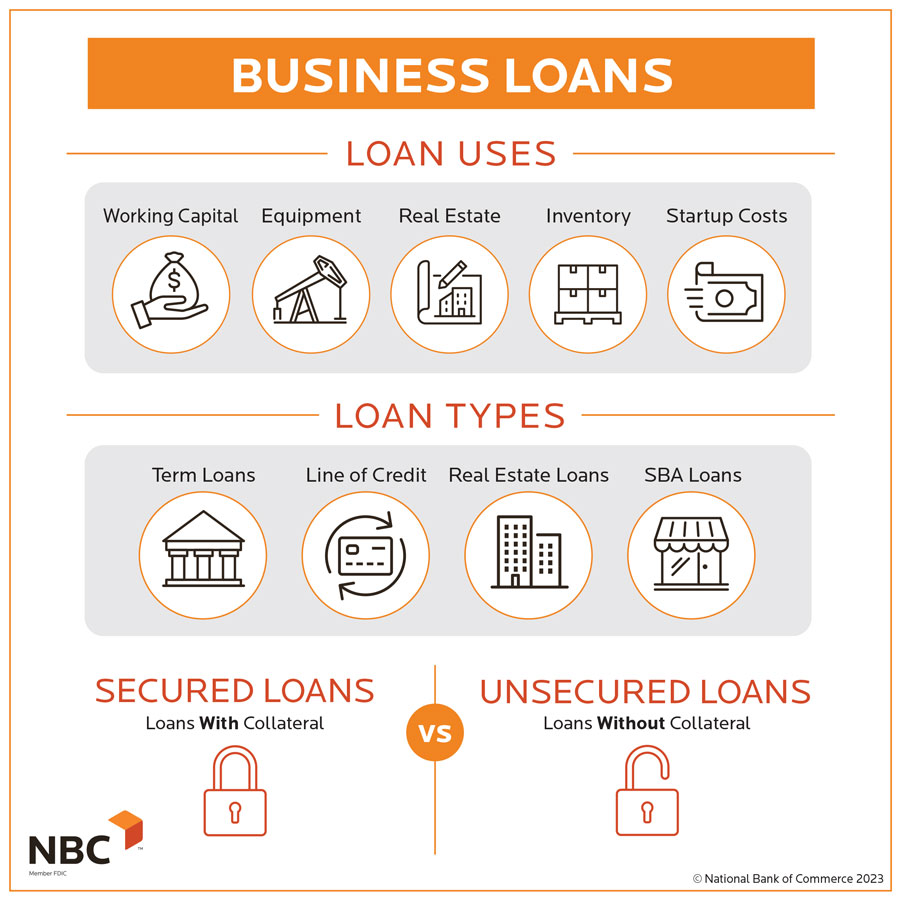

A critical component of how loans work is the presence or absence of collateral. A secured loan requires the borrower to pledge an asset—such as real estate, equipment, or inventory—as backing for the loan. If the borrower defaults, the lender has the legal right to seize the asset to recover their losses. Because this reduces the lender’s risk, secured loans often come with lower interest rates. Conversely, unsecured loans do not require collateral but are harder to qualify for and carry higher interest rates, as the lender is relying solely on the business’s creditworthiness and cash flow.

2. Navigating the Diverse Landscape of Loan Types

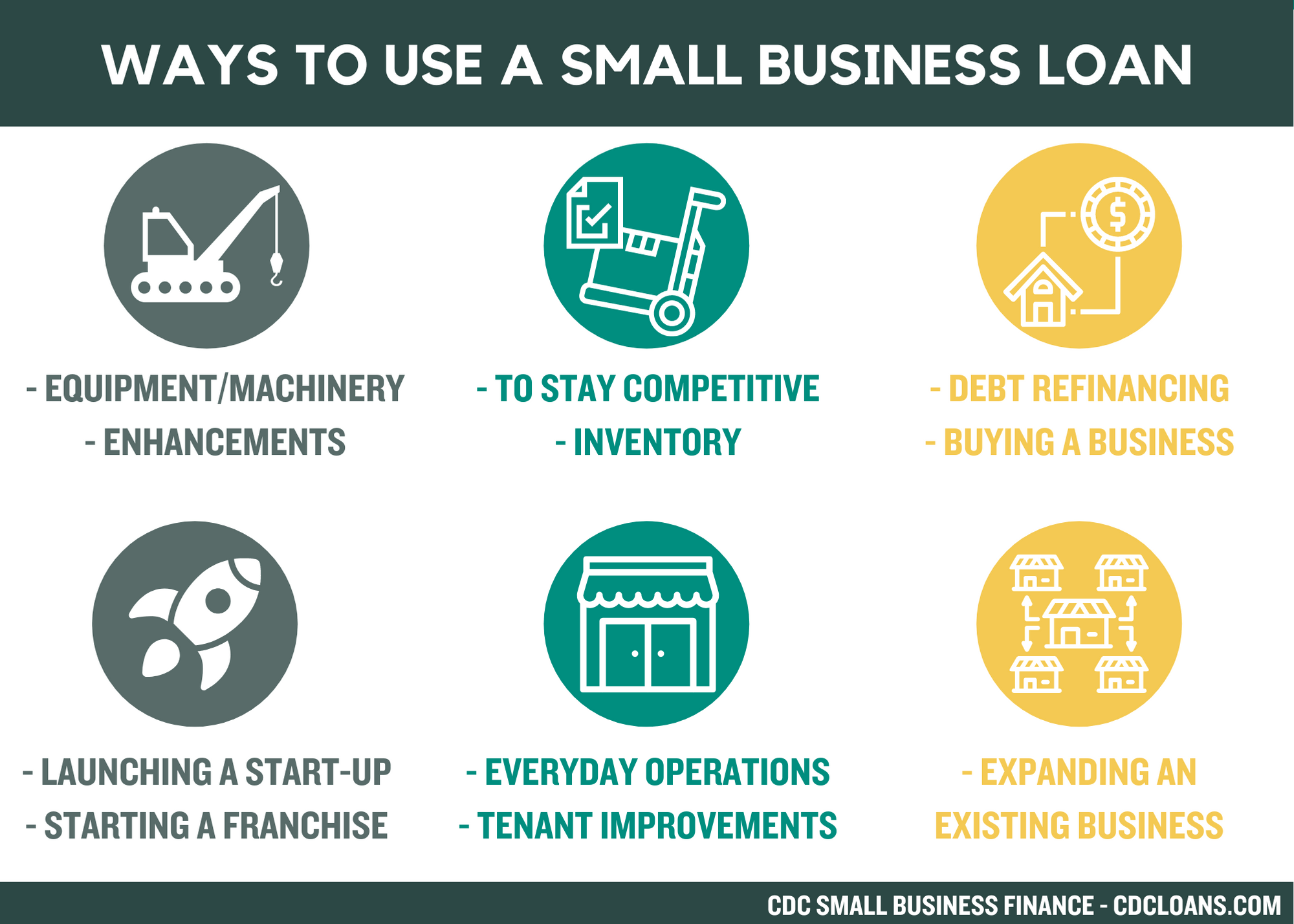

Not all small business loans are created equal. The financial structure of a loan should align with the specific purpose for which the funds are being used. Matching the wrong type of debt to a business need can lead to unnecessary costs or liquidity traps.

Traditional Term Loans and Lines of Credit

Traditional term loans are the most common form of business debt. They provide a specific amount of capital upfront, which is repaid over a set term (usually 1 to 10 years). These are best suited for long-term investments like purchasing a building or expanding to a new location. In contrast, a Business Line of Credit works more like a credit card. A business is approved for a maximum amount and can draw funds as needed. Interest is only paid on the amount actually borrowed. This is a premier tool for managing working capital and ensuring the business can handle unexpected expenses.

SBA-Backed Loans: The Gold Standard for Small Enterprises

The U.S. Small Business Administration (SBA) does not lend money directly to business owners. Instead, it provides a guarantee to banks and lenders, promising to pay back a portion of the loan if the borrower defaults. This “government-backed” security allows lenders to offer longer repayment terms and lower interest rates than they otherwise could. The SBA 7(a) program is the most popular, offering versatility for working capital, equipment, or debt refinancing. While the application process is rigorous and time-consuming, the financial benefits of an SBA loan are often superior to any other market offering.

Alternative Financing: Merchant Cash Advances and Invoice Factoring

For businesses that may not qualify for traditional bank loans, the “Money” niche offers alternative financing options. A Merchant Cash Advance (MCA) is not technically a loan but a sale of future credit card receivables. The provider gives the business a lump sum in exchange for a percentage of daily sales. While fast, these are often the most expensive forms of capital. Similarly, Invoice Factoring allows a business to sell its outstanding invoices to a third party at a discount to get immediate cash. These tools are high-cost, high-speed financial instruments used primarily for urgent liquidity needs.

3. The Financial Criteria and Qualification Process

Lenders use a specific set of metrics to determine whether a business is a “good bet.” In the world of finance, this is often referred to as the “Five Cs of Credit”: Character, Capacity, Capital, Collateral, and Conditions.

Credit Scores: Personal vs. Business Impact

For most small business owners, their personal financial history is inseparable from their business’s ability to borrow. Lenders look at personal FICO scores to gauge the owner’s reliability. However, as a business matures, it should develop its own business credit score (via bureaus like Dun & Bradstreet or Experian Business). A strong business credit profile allows the company to move away from personal guarantees, protecting the owner’s personal assets from business liabilities.

Debt-to-Income Ratios and Cash Flow Analysis

Cash flow is the most important metric in business finance. Lenders calculate the Debt Service Coverage Ratio (DSCR) by dividing the business’s annual net operating income by its total annual debt payments. A ratio of 1.25 or higher is generally required, indicating that the business has 25% more income than it needs to cover its debts. If your cash flow is inconsistent, lenders may view the loan as high-risk, regardless of how much profit you show on paper at the end of the year.

The Role of Collateral and Personal Guarantees

Even with a strong cash flow, many lenders require a Personal Guarantee. This is a legal agreement stating that the business owner will be personally responsible for the debt if the business cannot pay. This bridges the “trust gap” for the lender. Additionally, lenders look for “hard assets.” If you are borrowing to buy a $100,000 piece of equipment, that equipment serves as its own collateral, making the loan significantly easier to approve than a loan for “marketing expenses,” which leaves the lender with no tangible asset to recover in case of failure.

4. Evaluating the True Cost of Borrowing

One of the most common mistakes in business finance is focusing solely on the interest rate. To truly understand how a small business loan works, an entrepreneur must be able to calculate the total cost of capital.

APR vs. Interest Rates: Understanding the Discrepancy

The nominal interest rate is the percentage charged on the principal. However, the Annual Percentage Rate (APR) includes the interest rate plus all fees, such as origination fees, processing fees, and documentation costs. A loan with a 7% interest rate and high fees might actually have a 10% APR. When comparing different financial products, the APR is the only metric that provides an “apples-to-apples” comparison of what the debt actually costs.

Origination Fees and Hidden Closing Costs

When a loan is funded, the lender often takes an “origination fee” off the top—usually between 1% and 5% of the total loan amount. If you borrow $100,000 with a 3% origination fee, you only receive $97,000 in your bank account, yet you owe interest on the full $100,000. Other costs to watch for include “prepayment penalties,” which charge the borrower a fee for paying the loan off early, effectively locking them into a set amount of interest profit for the lender.

The Opportunity Cost of Debt

Finally, a sophisticated approach to business finance involves considering the opportunity cost. While debt carries a cost (interest), it should ideally be used to generate a return that exceeds that cost. If a small business loan has an APR of 8%, but the capital allows the business to increase its production capacity and generate a 20% increase in profit, the “net” gain is 12%. This is the essence of financial leverage: using borrowed money to increase the potential return on an investment.

Conclusion: Strategic Capital Management

Small business loans are not merely “handouts” or emergency funds; they are strategic tools used to fuel the engine of commerce. By understanding the mechanics of interest, the nuances of different loan types, and the rigorous criteria of lenders, business owners can navigate the financial landscape with confidence.

The key to successful borrowing lies in meticulous financial preparation and a clear understanding of the cost of capital. When used wisely, debt financing allows a business to grow faster than it could through organic cash flow alone, creating a path toward long-term wealth and enterprise value. In the world of money, those who understand how loans work are the ones best positioned to build lasting, profitable institutions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.