Managing personal finances often feels like a balancing act, where the most frequent and repetitive task is paying bills. While it may seem like a simple administrative chore, the way you approach your monthly obligations can significantly impact your credit score, your stress levels, and your overall financial health. In an era of digital banking and complex subscription models, “how do I pay bills?” is no longer a question of just writing a check; it is about building a sustainable system that ensures accuracy, punctuality, and strategic cash flow management.

This guide explores the multifaceted world of bill management, providing a professional roadmap for anyone looking to transition from reactive payments to a proactive financial strategy.

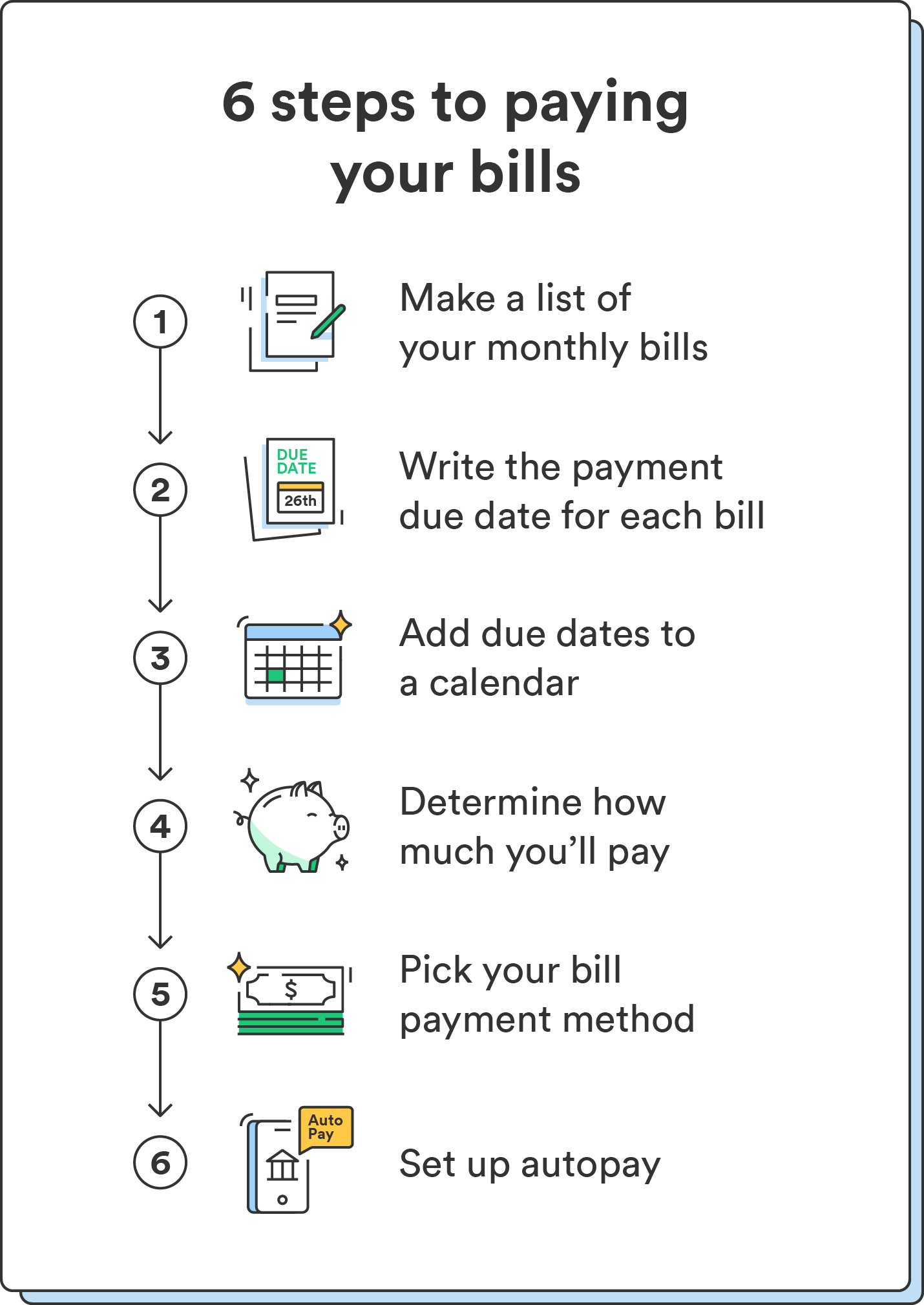

1. Establishing a Comprehensive Inventory of Your Financial Obligations

The first step in mastering bill payment is not the payment itself, but the organization of your liabilities. Without a clear bird’s-eye view of what you owe, who you owe it to, and when it is due, even the most diligent person can fall victim to late fees and service interruptions.

Categorizing Fixed and Variable Expenses

To build a functional system, you must distinguish between fixed and variable expenses. Fixed expenses remain constant month-over-month—think rent or mortgage payments, car insurance, and student loan installments. These are the easiest to plan for because the amount is predictable.

Variable expenses, such as electricity, water, or credit card balances, fluctuate based on usage or spending habits. By reviewing the past twelve months of utility statements, you can identify seasonal peaks (like high cooling costs in the summer) and adjust your budget accordingly. Understanding these fluctuations prevents the “sticker shock” that often disrupts a monthly budget.

Mapping the Billing Cycle

Every bill has a lifecycle: the statement date, the due date, and the grace period. Successful financial managers map these dates onto a master calendar. A common pitfall is having all major bills due in the first week of the month, which can strain cash flow if your income is distributed bi-weekly. If you find your due dates are poorly aligned with your paychecks, many service providers and credit card issuers allow you to request a change in your billing cycle to better suit your liquidity needs.

Auditing Subscriptions and Hidden Costs

In the modern economy, the “subscription creep” is a major drain on resources. From streaming services to software licenses and gym memberships, small monthly “micro-bills” can add up to hundreds of dollars. Part of paying your bills effectively is conducting a quarterly audit to ensure you are only paying for services that provide value. If you haven’t used a service in thirty days, it may be time to cancel the recurring payment.

2. Selecting the Most Efficient Payment Methods

Once you have organized your obligations, you must decide on the vehicle for payment. The method you choose can offer different levels of security, convenience, and even financial incentives.

The Power of Automation: Pros and Cons

Automated Clearing House (ACH) transfers and “Auto-pay” features are the gold standard for avoiding late fees. By linking your bank account directly to your service providers, you ensure that payments are made on time regardless of how busy your schedule becomes.

However, automation requires a “set it and monitor it” approach rather than “set it and forget it.” You must ensure that your checking account always maintains a sufficient buffer to cover these withdrawals. Overdraft fees can quickly negate the benefits of automation. For variable bills like credit cards, setting the automation to pay the “statement balance” rather than the “minimum payment” is crucial for avoiding high-interest debt.

Utilizing Online Bill Pay Through Financial Institutions

Most modern banks offer a centralized “Bill Pay” portal. Instead of logging into ten different websites to pay ten different vendors, you can manage everything from your bank’s dashboard. The bank either sends an electronic transfer or, in some cases, mails a physical check on your behalf. This centralized approach provides a single audit trail, making it much easier to track your spending and verify that payments were sent.

Strategic Use of Credit Cards for Bill Payment

For those with disciplined spending habits, paying bills via a rewards-bearing credit card can be a savvy financial move. By putting utilities, insurance, and cell phone bills on a card that offers 1% to 5% cash back, you effectively receive a discount on your cost of living.

The caveat is absolute: the credit card must be paid in full every month. If you carry a balance and incur interest, the interest charges will far outweigh any rewards earned. Additionally, some vendors (like utility companies or landlords) may charge a “convenience fee” for credit card payments, which usually exceeds the value of the rewards. Always calculate the cost-benefit ratio before choosing this method.

3. Integrating Bill Management into Your Broader Budget

Paying bills in isolation is a recipe for financial instability. True mastery comes from integrating these payments into a holistic budgeting framework that accounts for savings and discretionary spending.

The 50/30/20 Framework

A professional approach to bill payment often utilizes the 50/30/20 rule. In this model, 50% of your after-tax income is allocated to “Needs” (your essential bills like housing, utilities, and groceries), 30% to “Wants,” and 20% to savings and debt repayment. If your “Needs” category—your bills—consistently exceeds 50% of your income, it is a signal that you may need to downsize your lifestyle or find ways to increase your income to maintain long-term financial health.

The “Buffer” Method for Cash Flow Management

Cash flow timing is the most common reason people struggle to pay bills, even when they have enough total income. If a $2,000 mortgage is due on the 1st, but your $2,500 paycheck doesn’t arrive until the 5th, you have a liquidity crisis.

The “Buffer” method involves maintaining one month’s worth of expenses in your checking account at all times. This creates a “financial shock absorber” that ensures you are always paying this month’s bills with last month’s income. This eliminates the stress of “paycheck-to-paycheck” timing and provides a safety net against unexpected banking delays.

Prioritizing Payments in Times of Hardship

If you face a temporary financial setback, you must prioritize bills based on necessity. The hierarchy generally follows:

- Shelter and Utilities: Keeping the lights on and a roof over your head.

- Transportation: Necessary for getting to work to earn more income.

- Secured Debt: Such as car loans, where the asset can be repossessed.

- Unsecured Debt: Such as credit cards or personal loans.

While you should strive to pay everything, understanding this hierarchy helps you make logical decisions during a crisis.

4. Leveraging Technology and Security Protocols

In the digital age, paying bills is as much about data security as it is about mathematics. Utilizing the right tools can streamline the process while protecting your assets.

Specialized Financial Management Apps

Beyond your bank’s app, several third-party tools can help aggregate your bills. These apps can send you push notifications when a bill is generated, alert you to price hikes in your cable or internet service, and even negotiate lower rates on your behalf. When choosing an app, ensure it uses bank-level encryption and has a strong reputation for privacy.

Digital Security and Fraud Prevention

When paying bills online, security is paramount. Avoid using public Wi-Fi when accessing financial portals, as these networks are susceptible to “man-in-the-middle” attacks. Instead, use a secure home connection or a Virtual Private Network (VPN).

Furthermore, enable Multi-Factor Authentication (MFA) on every financial account. Even if a hacker obtains your password, they will be unable to access your account without the secondary code sent to your physical device. Regularly reviewing your bank statements for unauthorized transactions is the final line of defense in a robust bill-paying system.

5. Maintaining Credit Health Through Timely Payments

The ultimate goal of a bill-paying system—beyond keeping your services active—is the protection and improvement of your credit score. Your payment history is the single most important factor in your credit profile, typically accounting for 35% of your FICO score.

The Impact of 30-Day Delinquencies

A common misconception is that being a few days late on a bill will immediately trash your credit score. In reality, most creditors do not report a late payment to credit bureaus until it is at least 30 days past the due date. However, you will still incur late fees and potentially lose “promotional” interest rates. To maintain a “prime” credit score, you should aim for a 100% on-time payment history.

Communicating with Creditors

If you realize you cannot pay a bill on time, the most professional course of action is proactive communication. Most companies would rather set up a payment plan or grant a short extension than send an account to collections. Many utility companies have “hardship programs” or “levelized billing” options that can help stabilize your payments during difficult months. Reaching out before the due date demonstrates financial responsibility and can often result in waived late fees.

Conclusion

Paying bills is the foundational rhythm of adult financial life. By moving away from a disorganized, manual approach and toward a structured system of inventory, automation, and strategic budgeting, you transform a source of stress into a streamlined process.

The goal is to reach a state of “financial peace,” where your obligations are met automatically, your credit score is protected, and you have the mental bandwidth to focus on higher-level financial goals like investing and long-term wealth creation. Remember, you don’t just “pay” bills—you manage them. With the right tools and a disciplined mindset, you can ensure that your money is always working for you, rather than you simply working for your next bill.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.