The prospect of tax season often brings a mix of dread and anticipation, particularly the question of whether you’ll owe the IRS money or receive a refund. For many, the exact amount they owe remains a mystery until the very last minute, leading to stress, financial surprises, and sometimes, penalties. However, demystifying your tax liability is entirely possible with a proactive approach, leveraging available tools, and understanding the core principles of the U.S. tax system. This guide will walk you through the essential steps and resources to accurately determine how much you owe the IRS, empowering you with clarity and control over your financial obligations.

Understanding Your Tax Obligation: A Proactive Approach

Before diving into specific tools and methods, it’s crucial to grasp the foundational concepts that dictate your tax bill. Your tax liability isn’t a random number; it’s a calculation based on your income, deductions, credits, and filing status. Taking a proactive stance means understanding these elements throughout the year, rather than just in the weeks leading up to the April deadline.

Why Knowing Your Tax Bill Matters

Understanding your tax obligation well in advance offers significant advantages. Firstly, it allows for proper financial planning. No one wants an unexpected five-figure tax bill in April that throws their budget into disarray. By estimating what you owe, you can set aside funds, adjust your withholding, or even make estimated tax payments to avoid a large lump sum. Secondly, it helps prevent penalties. The IRS imposes penalties for underpayment, even if you eventually pay the full amount. Knowing your approximate liability can help you avoid these extra costs. Lastly, it fosters peace of mind, replacing anxiety with a sense of control over your financial health.

The Basics: Income, Deductions, and Credits

At its core, your federal income tax is calculated based on your taxable income. This isn’t just your gross income; it’s your gross income minus certain deductions.

- Income: This includes wages, salaries, freelance income, investment gains, rental income, and more. The IRS wants to know about all your income sources.

- Deductions: These reduce your taxable income. You can either take the standard deduction (a fixed amount based on your filing status) or itemize deductions (such as mortgage interest, state and local taxes, charitable contributions). The goal is to choose whichever reduces your taxable income more.

- Credits: These are even more powerful than deductions because they directly reduce your tax bill dollar-for-dollar. Examples include the Child Tax Credit, Earned Income Tax Credit, education credits, and credits for energy-efficient home improvements.

The more you understand how these three components interact, the better equipped you’ll be to estimate your tax liability and make informed financial decisions throughout the year.

Official IRS Resources for Determining Your Tax Liability

The IRS provides a wealth of tools and services designed to help taxpayers understand their current and past tax situations. These resources are authoritative, secure, and often the most accurate source of information.

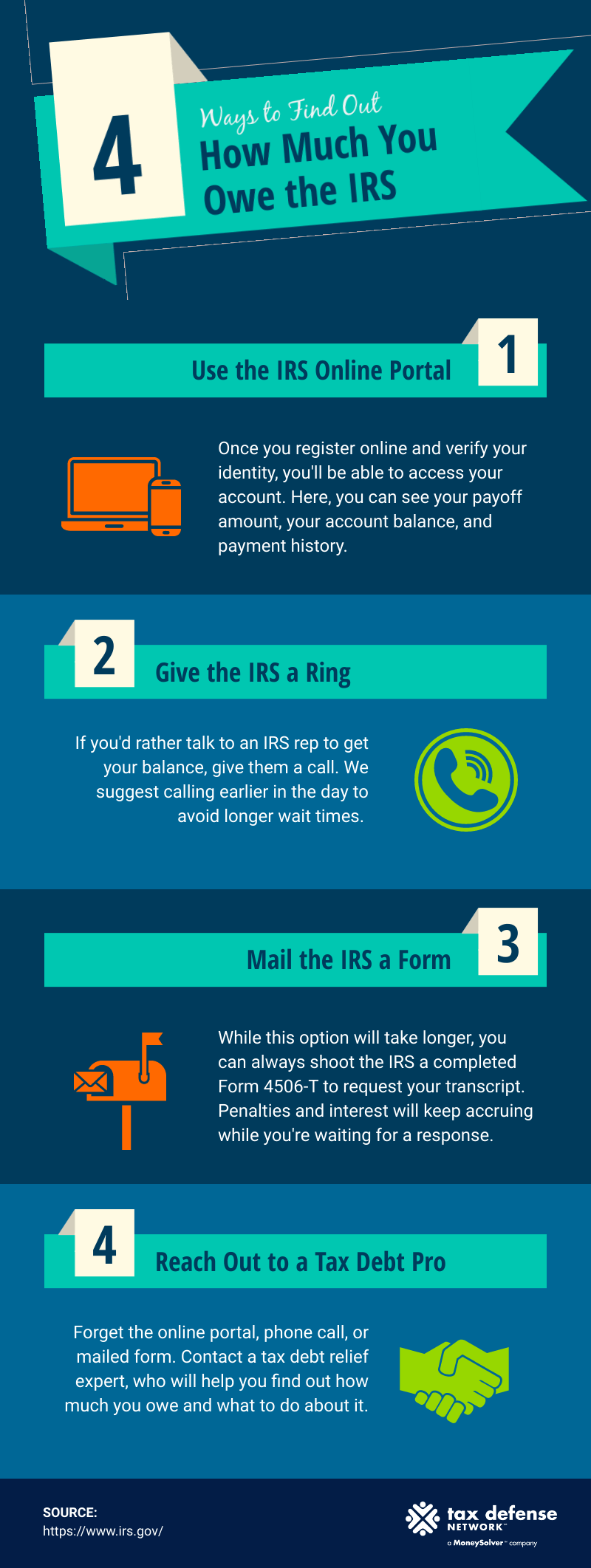

The IRS Tax Account: Your Digital Hub

The IRS online account is arguably the most valuable tool for taxpayers seeking to understand their current standing. After creating and verifying an account (a process that can take a few days due to security checks), you can:

- View your balance: See how much you owe, if anything, for current and past tax years.

- Access payment history: Review all payments you’ve made to the IRS, including estimated tax payments and prior year refunds applied to current year taxes. This helps you reconcile your records with theirs.

- Retrieve tax transcripts: These official documents provide various types of information, such as wage and income transcripts (showing data from W-2s, 1099s, etc.), account transcripts (showing financial transactions with the IRS), and record of account transcripts (combining both). Transcripts are vital for completing your current year’s return or verifying past information.

- View key data from your most recently filed tax return: This includes your Adjusted Gross Income (AGI), which is often needed for verification purposes.

Regularly checking your IRS online account can prevent surprises and provide a clear snapshot of your tax relationship with the government.

IRS Withholding Estimator

For employees, the IRS Withholding Estimator is an indispensable tool for preventing underpayment or overpayment of taxes throughout the year. Accessible on the IRS website, this free, online tool helps you:

- Adjust your W-4 form: Based on your projected income, deductions, and credits for the year, the estimator recommends how to fill out your Form W-4 to ensure the correct amount of tax is withheld from your paychecks.

- Account for life changes: It’s especially useful after major life events like marriage, divorce, having a child, buying a home, or changing jobs, which can significantly alter your tax situation.

- Plan for multiple income sources: If you have multiple jobs or also earn income from self-employment, the estimator helps you fine-tune your withholding to cover your total liability.

Using the Withholding Estimator can help you get closer to a “zero balance” at tax time, meaning you neither owe a large sum nor give the government an interest-free loan through an overly large refund.

Checking Payment Records and Filing Status

Beyond the IRS online account, it’s prudent to keep your own meticulous records of all tax-related payments and correspondence. When checking how much you owe, confirm that your records align with what the IRS has recorded. This includes:

- Employer withholdings: Your W-2 form, provided by your employer, details how much federal income tax was withheld from your pay.

- Estimated tax payments: If you’re self-employed or have significant income not subject to withholding, you likely make quarterly estimated tax payments. Keep records of these payments.

- Prior year refunds applied: If you chose to apply a refund from a previous year to the current year’s taxes, ensure this is accounted for.

Your filing status (Single, Married Filing Jointly, Head of Household, etc.) also significantly impacts your standard deduction and tax bracket. Ensure you are using the correct filing status based on your personal situation as of December 31st of the tax year.

Leveraging Tax Software and Professional Assistance

While IRS tools provide direct data, tax software and professionals are instrumental in calculating your actual tax liability by compiling all your financial information.

DIY Tax Software: Navigating the Options

Tax preparation software has revolutionized how many people file their taxes. Programs like TurboTax, H&R Block Tax Software, TaxAct, and FreeTaxUSA guide you through the process, performing complex calculations based on your inputs.

- Guided interviews: These programs ask a series of questions about your income, deductions, and credits, then populate the necessary forms for you.

- Accuracy checks: They often include built-in checks to flag potential errors or missed deductions.

- Real-time calculations: As you enter information, the software provides a running tally of your estimated refund or amount owed, giving you immediate feedback.

- e-Filing: Most software facilitates electronic filing (e-file), which is faster and more accurate than paper filing.

The key to using tax software effectively is honest and complete data entry. Any omissions or errors on your part will lead to an inaccurate calculation of what you owe. For simple tax situations, free versions of these programs or the IRS Free File program (available to taxpayers below certain income thresholds) can be excellent options.

The Value of a Tax Professional

For those with complex tax situations, significant life changes, or simply a desire for expert reassurance, a tax professional can be invaluable. This includes:

- Certified Public Accountants (CPAs): Licensed professionals with extensive knowledge of tax law, accounting, and financial planning.

- Enrolled Agents (EAs): Federally licensed tax practitioners who specialize in taxation and have unlimited practice rights before the IRS.

- Other Tax Preparers: Many reputable individuals and firms offer tax preparation services.

A professional can:

- Optimize deductions and credits: They can identify deductions and credits you might miss, potentially lowering your tax bill.

- Navigate complex scenarios: Dealing with self-employment income, investments, rental properties, foreign income, or stock options can be daunting; a professional can ensure accuracy and compliance.

- Provide strategic advice: Beyond just filing, they can offer insights into tax planning for future years.

- Represent you in audits: In the unfortunate event of an IRS audit, a professional can represent you and handle communication with the IRS.

While there’s a cost involved, the potential savings and peace of mind can often outweigh the fees, especially in complicated tax situations.

Understanding Your Tax Forms

Regardless of whether you use software or a professional, understanding the core tax forms that feed into your calculation is empowering:

- Form W-2: Wage and Tax Statement: From your employer, detailing wages earned and taxes withheld.

- Form 1099-NEC: Nonemployee Compensation: For independent contractors or freelancers.

- Form 1099-MISC: Miscellaneous Information: For certain other types of income (e.g., rents, royalties).

- Form 1099-DIV: Dividends and Distributions: For investment income.

- Form 1099-INT: Interest Income: For interest earned from banks.

- Form 1098: Mortgage Interest Statement: From your mortgage lender, for itemizing deductions.

- Schedule A: Itemized Deductions: If you choose to itemize instead of taking the standard deduction.

- Schedule C: Profit or Loss from Business (Sole Proprietorship): For self-employed individuals to report income and expenses.

Collecting all relevant forms before you start the calculation process is a critical first step.

Common Scenarios Leading to Unexpected Tax Bills

Understanding why you might unexpectedly owe money can help you prevent it in the future.

Under-Withholding from Paychecks

This is perhaps the most common reason people owe money. If you don’t have enough federal income tax withheld from your paychecks throughout the year, you’ll have a balance due at tax time. This often happens if:

- You filled out your W-4 form incorrectly (e.g., claiming too many dependents or deductions).

- You have multiple jobs and didn’t account for the combined income when setting withholding.

- You didn’t adjust your W-4 after a significant life event that decreased your deductions or increased your income.

- You simply claimed “exempt” from withholding without meeting the criteria.

Regularly reviewing and updating your W-4, especially after changes in income or family status, is vital. The IRS Withholding Estimator is your best friend here.

Untaxed Income Sources

Many types of income are taxable but don’t have taxes automatically withheld. This includes:

- Freelance/Gig Economy Income: If you work as an independent contractor, you’re responsible for paying your own self-employment taxes (Social Security and Medicare) in addition to income tax. The payer generally doesn’t withhold taxes.

- Investment Income: Interest, dividends, and capital gains from stocks, bonds, or mutual funds are often subject to tax.

- Rental Income: Income from renting out property.

- Gambling Winnings: Winnings from lotteries, casinos, and other forms of gambling are taxable.

If you have these types of income, you generally need to make estimated tax payments quarterly using Form 1040-ES to avoid an underpayment penalty.

Life Changes Affecting Tax Liability

Major life events can drastically alter your tax situation:

- Marriage or Divorce: Your filing status changes, which impacts your standard deduction, tax brackets, and eligibility for certain credits.

- New Dependents: Having a child can qualify you for credits like the Child Tax Credit, but also changes your withholding needs.

- Home Purchase or Sale: Mortgage interest, property taxes, and capital gains from a sale all have tax implications.

- Significant Income Change: A raise, new job, or starting a business directly affects your income and therefore your tax liability.

- Retirement: Different rules apply to retirement income and withdrawals from retirement accounts.

It’s critical to re-evaluate your tax planning after any major life change.

What to Do If You Owe Money

Even with the best planning, sometimes you’ll find you owe the IRS money. Knowing your options can alleviate stress.

Payment Options and Deadlines

The general deadline for filing and paying federal income taxes is April 15th (or the next business day if April 15th falls on a weekend or holiday). If you owe, you have several ways to pay:

- IRS Direct Pay: A free, secure way to pay directly from your checking or savings account.

- Debit Card, Credit Card, or Digital Wallet: Through third-party payment processors (fees apply).

- Electronic Federal Tax Payment System (EFTPS): A free service from the Treasury Department, ideal for making estimated tax payments or business tax payments.

- Electronic Funds Withdrawal: When e-filing your return, you can authorize the IRS to withdraw the payment directly from your bank account.

- Check or Money Order: Mailed with a Form 1040-V payment voucher.

Even if you can’t pay the full amount by the deadline, it’s crucial to file your return on time. The penalty for failure to file is generally higher than the penalty for failure to pay.

Dealing with Penalties and Interest

The IRS charges penalties for:

- Failure to File: If you don’t file your return by the due date.

- Failure to Pay: If you don’t pay the taxes you owe by the due date.

- Failure to Prepare an Accurate Return: If you significantly understate your tax liability.

- Underpayment of Estimated Tax: If you don’t pay enough tax throughout the year via withholding or estimated payments.

Interest is also charged on underpayments and unpaid penalties, compounding daily. If you receive a penalty notice, review it carefully. In some cases, you may be able to request penalty relief if you have a reasonable cause for the failure (e.g., natural disaster, serious illness).

Seeking Professional Guidance for Payment Difficulties

If you find yourself unable to pay your tax bill in full by the deadline, don’t ignore it. The IRS has options available, but you must initiate contact. A tax professional (CPA or Enrolled Agent) can help you navigate these solutions:

- Short-Term Payment Plan: You may be granted up to 180 additional days to pay your tax liability in full, though interest and penalties still apply.

- Offer in Compromise (OIC): Allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owed. This is generally an option if you’re facing significant financial hardship.

- Installment Agreement: Allows you to make monthly payments for up to 72 months. This is often an option if you owe less than $50,000 in combined tax, penalties, and interest.

The key is communication. The IRS is generally more amenable to working with taxpayers who are transparent and proactive about their inability to pay.

Knowing how much you owe the IRS doesn’t have to be a guessing game. By consistently monitoring your income and expenses, utilizing official IRS tools, leveraging reliable tax software, and seeking professional advice when needed, you can maintain a clear understanding of your tax obligations and approach tax season with confidence and control. This proactive financial management not only ensures compliance but also fosters greater peace of mind regarding your overall financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.