The S&P 500, or the Standard & Poor’s 500, stands as one of the most widely recognized and respected benchmarks for the U.S. stock market. Representing 500 of the largest publicly traded companies in the United States, it offers a broad snapshot of the nation’s economic health and corporate performance. For countless investors, both novice and seasoned, the idea of tapping into the consistent, long-term growth potential of these powerhouse companies is incredibly appealing. However, the direct question remains: how does one, a retail investor, effectively and intelligently put their capital into this influential index?

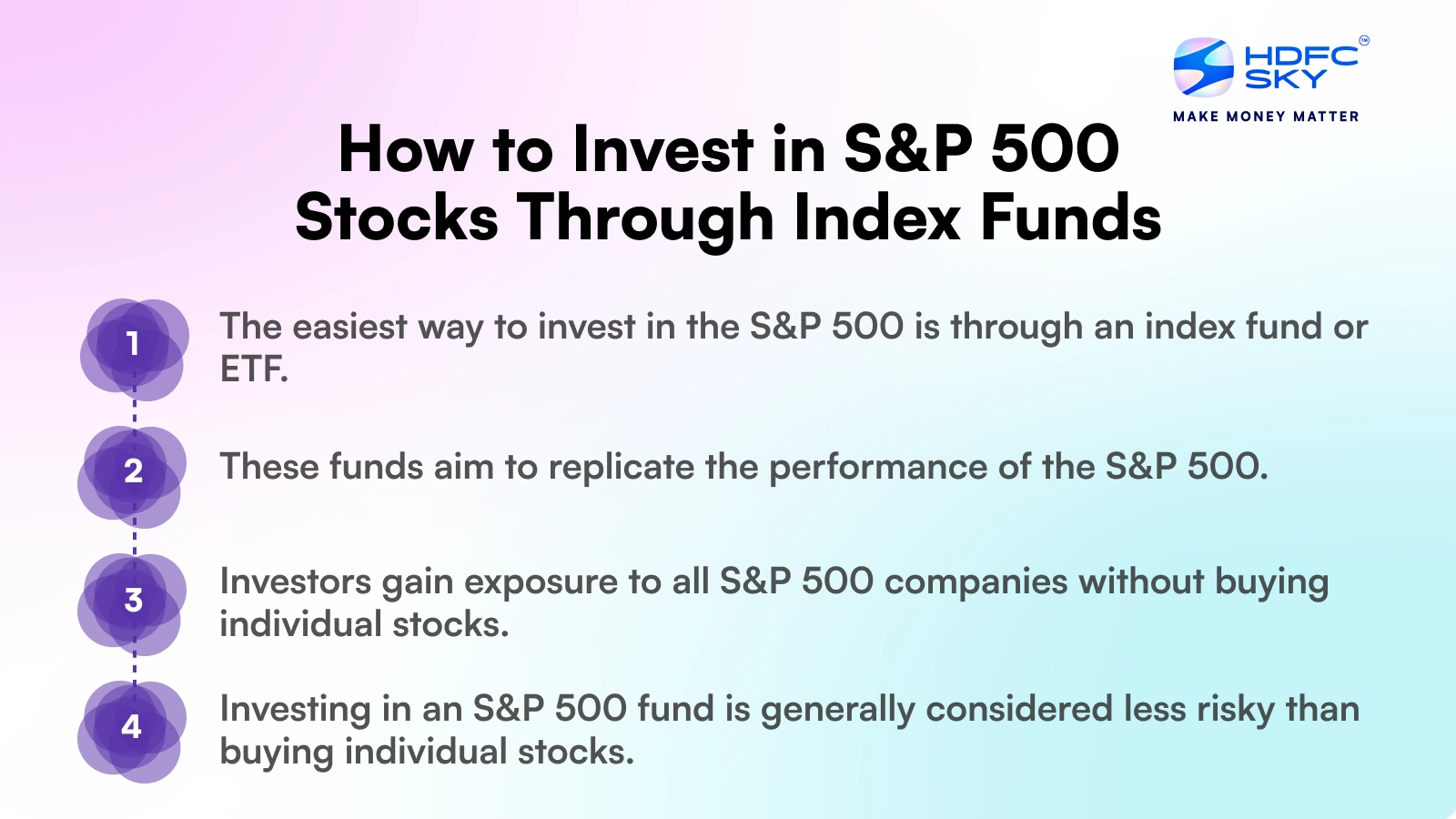

Investing in the S&P 500 isn’t about buying 500 individual stocks; rather, it’s about gaining exposure to the index as a whole through diversified investment vehicles. This approach simplifies portfolio management, reduces individual stock risk, and historically has delivered compelling returns over extended periods. This comprehensive guide will demystify the process, exploring the various avenues available, the practical steps involved, and the crucial considerations for anyone looking to make the S&P 500 a cornerstone of their investment strategy.

Understanding the S&P 500 and Why It Matters

Before delving into the “how,” it’s essential to grasp the “what” and “why” behind the S&P 500’s significance in the investment world. Its pervasive influence stems from its representative nature and its track record of long-term wealth creation.

What is the S&P 500?

The S&P 500 is a stock market index that reflects the performance of 500 of the largest U.S. publicly traded companies, selected by a committee at S&P Dow Jones Indices. These companies are chosen based on criteria such as market size, liquidity, and sector representation, making the index a robust gauge of the overall U.S. equity market and the broader economy. Unlike the Dow Jones Industrial Average, which is price-weighted and contains only 30 stocks, the S&P 500 is market-capitalization weighted, meaning companies with larger market values have a greater impact on the index’s performance. This weighting gives a more accurate representation of the market’s collective value. From tech giants like Apple and Microsoft to financial powerhouses like JPMorgan Chase and consumer staples like Coca-Cola, the index offers an unparalleled diversity across virtually every major sector.

The Allure of Index Investing

Investing in the S&P 500 is a classic example of “index investing,” a strategy championed by investment legends like Warren Buffett. The core appeal lies in its simplicity and efficiency. Instead of attempting the difficult and often unsuccessful task of picking individual winning stocks (active investing), index investing relies on the belief that over the long term, the market as a whole tends to rise. By investing in an S&P 500 index fund, you are essentially buying a tiny slice of all 500 companies in the index, instantly achieving broad diversification. This diversification significantly reduces the risk associated with a single company’s poor performance, as potential losses are offset by gains in other components of the index. It eliminates the need for extensive research into individual companies and bypasses the higher fees often associated with actively managed funds.

Historical Performance and Long-Term Growth

The S&P 500’s historical performance is arguably its most compelling feature. Over the past several decades, despite numerous recessions, market crashes, and geopolitical events, the S&P 500 has demonstrated an impressive average annual return, typically cited around 10-12% before inflation. While past performance is never a guarantee of future results, this consistent growth has allowed patient investors to build substantial wealth over the long term. This strong track record underscores the power of compounding returns and makes the S&P 500 an attractive option for retirement planning, wealth accumulation, and achieving other long-term financial goals. It’s a testament to the resilience and innovative spirit of American corporations, continuously adapting and growing.

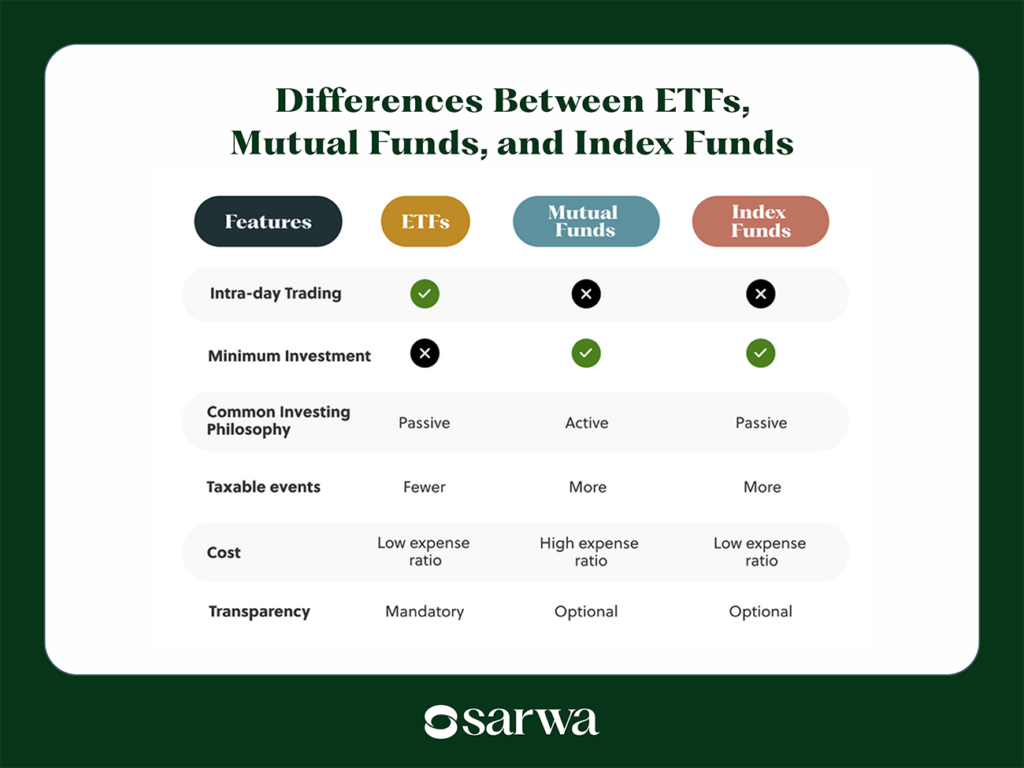

Direct Investment Routes: ETFs and Mutual Funds

For most individual investors, gaining exposure to the S&P 500 comes down to two primary, highly accessible investment vehicles: Exchange-Traded Funds (ETFs) and S&P 500 Index Mutual Funds. Both offer a diversified basket of the 500 underlying stocks, but they differ in their structure, trading mechanisms, and fee characteristics.

Exchange-Traded Funds (ETFs) Tracking the S&P 500

ETFs are popular investment funds that hold assets like stocks, commodities, or bonds and trade on stock exchanges much like individual stocks. An S&P 500 ETF, such as SPY (SPDR S&P 500 ETF Trust), IVV (iShares Core S&P 500), or VOO (Vanguard S&P 500 ETF), aims to replicate the performance of the S&P 500 index. When you buy shares of an S&P 500 ETF, you are buying a small portion of the entire portfolio that mirrors the index.

Advantages of S&P 500 ETFs:

- Liquidity: ETFs can be bought and sold throughout the trading day at market prices, offering flexibility.

- Low Expense Ratios: Many S&P 500 ETFs have extremely low expense ratios (annual fees), often less than 0.10%, making them very cost-effective.

- Diversification: Instantaneous diversification across 500 companies.

- Tax Efficiency: ETFs can be more tax-efficient than mutual funds due to their creation/redemption mechanism, which can minimize capital gains distributions.

S&P 500 Index Mutual Funds

S&P 500 index mutual funds are professionally managed funds that pool money from many investors to invest in the companies that make up the S&P 500. Unlike ETFs, mutual funds are typically bought and sold once per day at their Net Asset Value (NAV) after the market closes. Popular examples include Fidelity 500 Index Fund (FXAIX) and Vanguard 500 Index Fund (VFIAX).

Advantages of S&P 500 Index Mutual Funds:

- Simplicity: Automatic investing through regular contributions is straightforward.

- Professional Management: While passively managed to track the index, the fund is overseen by a management team.

- Low Minimums (for some): Some funds have relatively low initial investment minimums or allow for fractional share investing through regular contributions.

- No Bid-Ask Spreads: You buy at the NAV, avoiding potential bid-ask spread costs associated with ETFs.

Key Differences: ETFs vs. Mutual Funds

While both provide S&P 500 exposure, their operational differences matter:

- Trading: ETFs trade continuously like stocks; mutual funds trade once a day after market close.

- Pricing: ETFs have fluctuating market prices and bid-ask spreads; mutual funds are priced at NAV.

- Minimums: ETFs often have no minimums beyond the cost of one share; mutual funds can have higher initial investment minimums (though some brokers offer no-minimum versions).

- Tax Efficiency: ETFs generally offer greater tax efficiency due to their structure, which allows them to manage capital gains more effectively than traditional mutual funds.

The choice between an S&P 500 ETF and a mutual fund often comes down to personal preference for trading flexibility, minimum investment amounts, and specific tax considerations. Both are excellent, low-cost options for broad market exposure.

Indirect Investment through Robo-Advisors and Brokerage Accounts

Beyond choosing between ETFs and mutual funds, how you access and manage these investments is equally important. Robo-advisors offer automated, hands-off solutions, while traditional brokerage accounts provide greater control for self-directed investors.

Leveraging Robo-Advisors for S&P 500 Exposure

Robo-advisors are digital platforms that use algorithms to provide automated, low-cost investment management services. They typically construct diversified portfolios based on your risk tolerance, financial goals, and time horizon, often including S&P 500 ETFs as core components. Platforms like Betterment, Wealthfront, and Schwab Intelligent Portfolios are popular examples.

How it works: You answer a series of questions about your financial situation and risk appetite. The robo-advisor then recommends and manages a portfolio, automatically rebalancing it over time. Many of these diversified portfolios will include a significant allocation to a low-cost S&P 500 ETF to capture broad market growth.

Benefits:

- Automation: Set it and forget it – ideal for passive investors.

- Low Fees: Management fees are typically a small percentage of assets under management (e.g., 0.25% – 0.50%).

- Diversification: Provides a fully diversified portfolio, not just S&P 500 exposure, often including bonds, international stocks, and other asset classes for enhanced risk management.

- Accessibility: Low minimum initial investments.

Self-Directed Investing via Brokerage Platforms

For investors who prefer more control, opening an account with a traditional online brokerage firm is the most common route. Platforms like Fidelity, Charles Schwab, Vanguard, E*TRADE, and TD Ameritrade (now Schwab) allow you to open various account types (e.g., Roth IRA, Traditional IRA, taxable brokerage account) and directly purchase S&P 500 ETFs or mutual funds.

How it works: You open an account, deposit funds, and then use the platform’s trading interface to buy shares of your chosen S&P 500 ETF or mutual fund. You are responsible for monitoring your investments, rebalancing, and making future contributions.

Benefits:

- Control: Full control over investment choices and trading decisions.

- Variety: Access to a wider range of investment products beyond S&P 500 index funds.

- Lower Ongoing Fees (potentially): Once you pay transaction fees (if any) to buy the fund, there are typically no additional management fees from the brokerage itself for holding assets, unlike robo-advisors.

- Education: Most platforms offer extensive educational resources and research tools.

Understanding Fees and Minimums

Regardless of the route you choose, understanding the associated fees and minimums is critical.

- Expense Ratios: The annual fee charged by an ETF or mutual fund, expressed as a percentage of your investment. Aim for funds with expense ratios below 0.15% for S&P 500 index funds.

- Trading Commissions: Some brokerages charge a small fee ($0-$5) per trade for ETFs or mutual funds, though many now offer commission-free trading for a wide selection of funds.

- Robo-Advisor Management Fees: An annual percentage fee charged by robo-advisors for their automated service.

- Account Minimums: The minimum amount required to open an account or invest in a specific fund. Some S&P 500 mutual funds have minimums of $1,000 or $3,000, while ETFs often only require the price of one share.

Minimizing fees is paramount, as even small percentages can significantly erode your long-term returns due to the power of compounding.

Important Considerations Before Investing

While investing in the S&P 500 is generally considered a sound long-term strategy, it’s not without its nuances. A thoughtful approach requires understanding inherent risks, aligning investments with personal goals, and leveraging smart strategies.

Risk vs. Reward: Volatility and Diversification

Even though the S&P 500 offers diversification across 500 companies, it is still an investment in equities, which inherently carry market risk. The value of your investment will fluctuate with the overall market, experiencing periods of growth and decline (volatility). A market downturn, even if temporary, can cause anxiety and lead to temptation to sell low.

Key takeaway: While the S&P 500 provides excellent diversification within the U.S. large-cap equity space, it does not fully diversify against systemic market risk or global economic downturns. For true overall portfolio diversification, you might consider adding bonds, international stocks, and other asset classes, which many robo-advisors automatically do or which you can implement in a self-directed portfolio. Understand that the S&P 500 is a growth engine, but it comes with periods of turbulence.

Time Horizon and Investment Goals

Your investment time horizon is arguably the most crucial factor when investing in the S&P 500. Historically, the S&P 500 has proven to be an excellent long-term investment (10+ years), allowing ample time to recover from market downturns and benefit from compounding returns. However, for short-term goals (e.g., saving for a down payment in 1-3 years), the S&P 500 might be too volatile, and a sudden market dip could jeopardize your goal.

Align your investment:

- Long-term goals (retirement, college savings): S&P 500 is highly suitable.

- Mid-term goals (5-10 years): Potentially suitable, but consider a more conservative allocation.

- Short-term goals (<5 years): Generally not recommended for substantial S&P 500 exposure; look to safer assets like high-yield savings accounts or short-term CDs.

Tax Implications of S&P 500 Investing

Understanding the tax implications of your S&P 500 investments is essential for maximizing your returns.

- Dividends: S&P 500 companies pay dividends, which are taxable income in the year they are received, unless held in a tax-advantaged account.

- Capital Gains: When you sell an S&P 500 ETF or mutual fund for more than you paid, you realize a capital gain. Short-term capital gains (assets held for one year or less) are taxed at your ordinary income rate, while long-term capital gains (assets held for more than one year) are typically taxed at lower, preferential rates.

- Tax-Advantaged Accounts: Investing in an S&P 500 fund within a Roth IRA, Traditional IRA, 401(k), or other retirement accounts offers significant tax benefits (tax-deferred growth or tax-free withdrawals in retirement), making them ideal vehicles for long-term S&P 500 investing.

- Taxable Brokerage Accounts: If investing in a regular brokerage account, you will be subject to taxes on dividends and capital gains.

Consult with a tax professional to understand how S&P 500 investments fit into your overall tax strategy.

Dollar-Cost Averaging Strategy

Dollar-cost averaging (DCA) is a powerful strategy often employed when investing in volatile assets like the S&P 500. It involves investing a fixed amount of money at regular intervals (e.g., $100 every month), regardless of the asset’s price.

Benefits of DCA:

- Reduces Risk: It mitigates the risk of investing a large lump sum at an unfortunate market peak.

- Averages Out Cost: When prices are high, your fixed investment buys fewer shares; when prices are low, it buys more shares. Over time, your average cost per share tends to be lower.

- Removes Emotion: Automating investments removes the temptation to time the market, which is notoriously difficult and often counterproductive.

- Disciplined Investing: Encourages consistent contributions to your portfolio, fostering a habit of regular saving.

This strategy is particularly effective for long-term S&P 500 investors who are building wealth consistently over many years.

Getting Started: A Step-by-Step Guide

Embarking on your S&P 500 investment journey doesn’t have to be daunting. By following a clear, structured approach, you can confidently begin building your portfolio.

Define Your Investment Goals

Before opening any accounts, clarify what you’re investing for. Are you saving for retirement in 30 years? A down payment on a house in 10 years? Understanding your objectives will help determine your time horizon, risk tolerance, and the appropriate amount to invest. This foundational step ensures your investments align with your broader financial plan. Consider how much risk you’re comfortable taking and how much capital you can afford to invest consistently without impacting your immediate financial stability.

Choose Your Investment Vehicle

Based on your goals, preferences, and tax situation, decide whether to use a tax-advantaged account (like an IRA or 401(k)) or a taxable brokerage account. For most long-term investors, maximizing contributions to tax-advantaged accounts should be the priority. Next, choose your preferred investment product:

- S&P 500 ETF: Offers intraday trading flexibility and excellent tax efficiency for a self-directed approach.

- S&P 500 Index Mutual Fund: Simpler for automated, regular investments, especially if your brokerage offers no-fee versions with low minimums.

- Robo-Advisor: Best for hands-off investors seeking a fully diversified portfolio managed automatically, which will likely include S&P 500 exposure.

Research specific funds or robo-advisors, comparing expense ratios, minimums, and historical performance.

Open and Fund Your Account

Once you’ve chosen your vehicle and investment product, open an account with a reputable brokerage firm (e.g., Vanguard, Fidelity, Schwab) or a robo-advisor platform. The process typically involves:

- Providing personal information: Name, address, Social Security number, employment details.

- Verifying identity: Often requires uploading a photo ID.

- Linking a bank account: This allows you to transfer funds to your investment account.

- Funding the account: Initiate an electronic transfer from your bank. You can set up one-time transfers or recurring deposits, which is highly recommended for dollar-cost averaging.

Many platforms have user-friendly interfaces that guide you through each step.

Monitor and Rebalance Your Portfolio

Investing in the S&P 500 is not a set-it-and-forget-it endeavor without any oversight. While active trading is unnecessary, periodic monitoring is crucial.

- Regular Contributions: Consistently add funds to leverage dollar-cost averaging.

- Annual Review: At least once a year, review your portfolio’s performance against your goals.

- Rebalancing (if needed): If you have a diversified portfolio beyond just the S&P 500, or if your S&P 500 allocation becomes too large or small relative to your target, you may need to rebalance. This involves selling a portion of overperforming assets and buying more of underperforming ones to restore your desired asset allocation. Robo-advisors handle this automatically. For self-directed investors, this might mean simply directing new contributions to underweighted assets.

- Adjust as Goals Change: As you approach retirement or other major life events, you might gradually shift a portion of your S&P 500 exposure to more conservative investments.

Investing in the S&P 500 is a proven path to long-term wealth accumulation. By understanding its mechanics, choosing the right investment vehicles, and maintaining a disciplined approach, you can confidently leverage the power of the U.S. stock market’s largest companies to achieve your financial aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.