In an increasingly complex world, managing personal finances extends far beyond saving for retirement or paying off debt. One of the most significant and often overlooked components of a sound financial plan is healthcare coverage. For millions of Americans, the Affordable Care Act (ACA), often referred to as “Obamacare,” represents a critical pathway to accessible and affordable health insurance. The question “how do I get Obamacare” isn’t merely about signing up for a plan; it’s fundamentally a financial inquiry into understanding costs, leveraging subsidies, and making informed decisions that protect both your health and your wallet.

This guide will demystify the process of obtaining ACA coverage, focusing exclusively on the financial dimensions involved. From understanding the core economic principles of the ACA to navigating the marketplace for optimal value, we’ll equip you with the insights needed to secure healthcare while maintaining financial stability.

Understanding the Financial Landscape of the Affordable Care Act (ACA)

Before diving into the application process, it’s crucial to grasp the financial framework underpinning the Affordable Care Act. The ACA was designed to expand health insurance coverage, primarily by creating a marketplace where individuals and families can shop for plans, and by offering financial assistance to make those plans more affordable.

What is the ACA and Why Does it Matter for Your Wallet?

At its core, the ACA is a federal law aimed at reforming the U.S. healthcare system. From a financial perspective, its key innovations include:

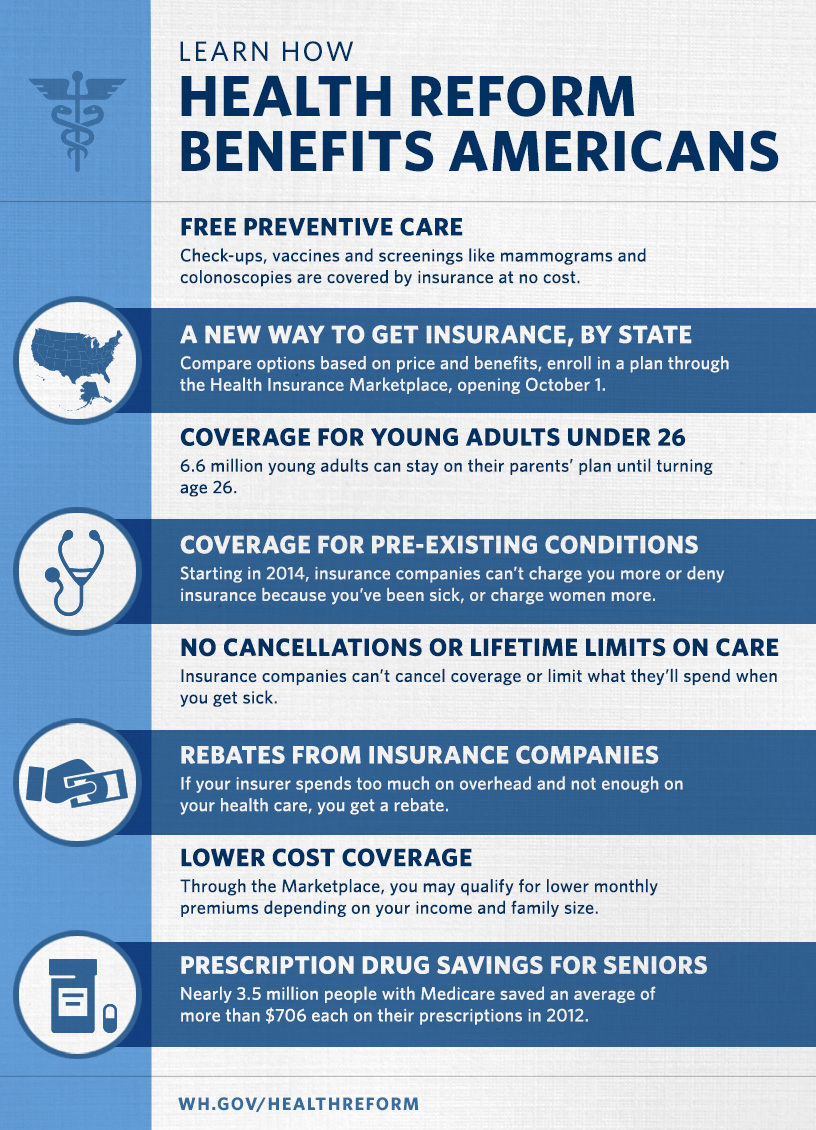

- Guaranteed Issue: Insurers cannot deny coverage based on pre-existing conditions, a monumental financial protection for those with ongoing health needs.

- Essential Health Benefits: All plans offered through the marketplace must cover a comprehensive set of services, ensuring you get meaningful coverage for your premiums. This prevents individuals from purchasing “junk insurance” that offers little real financial protection.

- Financial Assistance: The most significant financial component for most enrollees are the subsidies designed to reduce the cost of premiums and out-of-pocket expenses. Without these, many would find coverage prohibitively expensive.

- Annual Open Enrollment: A dedicated period each year ensures a structured approach to comparing plans and securing the best financial fit for the upcoming year.

For your wallet, the ACA translates into predictable healthcare costs, protection against catastrophic medical bills, and potentially significant savings through government assistance. Understanding these foundational elements is the first step toward financially smart healthcare decisions.

Key Financial Terms: Premiums, Deductibles, Co-pays, and Out-of-Pocket Maximums

Navigating health insurance requires familiarity with specific financial terminology. Each term represents a different facet of how you pay for your healthcare:

- Premium: This is the monthly payment you make to your insurance company to keep your coverage active. It’s a fixed cost, akin to a subscription fee, and is a primary budget item for anyone with health insurance.

- Deductible: The amount of money you must pay for covered healthcare services before your insurance plan starts to pay. For example, if your deductible is $2,000, you’ll pay the first $2,000 of covered medical expenses yourself each year before your insurer contributes. High-deductible plans typically have lower premiums, and vice-versa, presenting a key financial trade-off.

- Co-payment (Co-pay): A fixed amount you pay for a covered healthcare service after you’ve met your deductible. For instance, a $20 co-pay for a doctor’s visit means you pay $20, and your insurer covers the rest for that specific service.

- Co-insurance: Your share of the cost of a healthcare service, calculated as a percentage (e.g., 20%) of the allowed amount for the service, after you’ve met your deductible. If a service costs $100 and your co-insurance is 20%, you pay $20, and the insurer pays $80.

- Out-of-Pocket Maximum: This is the most you’ll have to pay for covered services in a plan year. Once you reach this limit, your health plan pays 100% of the costs of covered benefits for the remainder of the year. This is your ultimate financial safety net, protecting you from crippling medical debt in the event of severe illness or injury.

Understanding these terms is paramount to comparing plans financially and anticipating your potential healthcare expenditures throughout the year.

The Role of Subsidies: Making Coverage Affordable

Perhaps the most critical financial feature of the ACA is the availability of subsidies, designed to reduce the financial burden of health insurance. These come in two main forms:

- Premium Tax Credits (PTC): These are government payments that reduce your monthly insurance premium. Eligibility and the amount of the credit are based on your household income and family size relative to the Federal Poverty Level (FPL). You can choose to have these credits paid directly to your insurer each month, lowering your premium upfront, or claim them on your tax return.

- Cost-Sharing Reductions (CSR): These subsidies reduce the amount you pay out-of-pocket for deductibles, co-payments, and co-insurance. Unlike PTCs, CSRs are only available if you enroll in a “Silver” level plan and have an income below a certain threshold (typically 250% of the FPL). CSRs effectively make Silver plans much more robust, offering “gold-level” coverage for a “silver-level” price for eligible individuals.

These subsidies are the cornerstone of ACA affordability, making health insurance accessible to millions who might otherwise be priced out of the market. Understanding your eligibility for both PTCs and CSRs is crucial for optimizing your healthcare budget.

The Application Process: A Step-by-Step Financial Journey

“How do I get Obamacare” ultimately boils down to navigating the application process on HealthCare.gov (or your state’s marketplace, if applicable). This journey is fundamentally a financial one, requiring you to gather specific income and household information to determine your eligibility for plans and, crucially, for financial assistance.

Gathering Your Financial Information: Income, Household Size, and Tax Filings

Before you even begin to browse plans, the first step is to collect accurate financial data. The marketplace uses this information to determine your eligibility for subsidies and to verify your identity. You’ll need:

- Estimated Household Income for the Coverage Year: This is one of the most important pieces of information. It’s not your past income, but what you reasonably expect to earn (gross income before taxes) in the year you want coverage. Include all sources of taxable income for every member of your tax household. Be as accurate as possible; discrepancies could lead to having to repay tax credits later.

- Household Size: This refers to the number of people you include on your tax return, typically yourself, your spouse, and any tax dependents. This directly impacts your FPL calculation for subsidy eligibility.

- Tax Filing Status: Whether you file as single, married filing jointly, head of household, etc., is relevant. Most notably, if you are married, you generally must file jointly to be eligible for premium tax credits.

- Current Insurance Information (if applicable): While not strictly financial, information about existing coverage helps streamline the transition if you’re switching plans.

- Social Security Numbers (SSNs) or document numbers for legal immigrants: Required for everyone applying for coverage to verify identity and citizenship/immigration status.

Having these details ready will make the application process much smoother and ensure you receive the correct amount of financial aid.

Exploring Coverage Options and Cost Tiers (Bronze, Silver, Gold, Platinum)

The ACA marketplace offers plans categorized into “metal levels” based on how they split costs with you:

- Bronze Plans: These plans typically have the lowest monthly premiums but the highest deductibles and out-of-pocket maximums. They cover roughly 60% of average healthcare costs, with you paying 40%. Best suited for those who anticipate needing minimal care and want protection against catastrophic events.

- Silver Plans: The most popular choice, Silver plans have moderate premiums and deductibles. They cover about 70% of average healthcare costs (you pay 30%). Crucially, these are the only plans eligible for Cost-Sharing Reductions, making them significantly more valuable for eligible individuals.

- Gold Plans: These plans have higher monthly premiums but lower deductibles and out-of-pocket costs. They cover approximately 80% of average costs. Good for those who expect to use a fair amount of healthcare services and prefer predictable, lower costs when care is needed.

- Platinum Plans: These plans have the highest monthly premiums but the lowest deductibles and out-of-pocket costs, covering about 90% of average costs. Ideal for individuals with chronic conditions or those who anticipate frequent medical needs and want minimal financial surprises.

When choosing, consider your health needs and financial comfort with deductibles versus monthly premiums. A lower premium might seem appealing, but a high deductible could expose you to significant out-of-pocket costs if you need care.

Applying for Financial Assistance: Premium Tax Credits and Cost-Sharing Reductions

The marketplace application automatically assesses your eligibility for both Premium Tax Credits (PTC) and Cost-Sharing Reductions (CSR) based on the financial information you provide.

- Premium Tax Credits (PTC): As you compare plans, the marketplace will display the estimated monthly premium after your PTC has been applied. You can then decide how much of this credit you want to apply directly to your premium each month. For instance, if your premium is $400 and you’re eligible for a $300 PTC, you’ll only pay $100 monthly.

- Cost-Sharing Reductions (CSR): If your income qualifies you for CSRs, the marketplace will automatically show you enhanced Silver plans that have lower deductibles, co-pays, and out-of-pocket maximums than standard Silver plans. It’s vital to enroll in a Silver plan to receive CSR benefits. If you qualify for CSRs but choose a Bronze, Gold, or Platinum plan, you will not receive those cost-sharing benefits.

Carefully review these financial assistance options. They can dramatically alter the true cost of your healthcare and are fundamental to making ACA coverage genuinely affordable.

Maximizing Your Financial Benefits and Avoiding Pitfalls

Securing ACA coverage is just the beginning. To truly optimize your healthcare spending, you need to understand how to leverage the system’s flexibility and avoid common financial missteps.

Understanding Special Enrollment Periods and Life Changes (Impact on Subsidies)

While Open Enrollment is the primary window for securing coverage, certain “Qualifying Life Events” trigger a Special Enrollment Period (SEP). These events can include:

- Losing other health coverage (e.g., job loss, turning 26 and coming off a parent’s plan)

- Getting married or divorced

- Having a baby, adopting a child, or placing a child for adoption

- Moving to a new area

- Significant changes in household income

It’s crucial to report these life changes to the marketplace promptly. A change in income or household size can significantly impact your subsidy eligibility. Failing to report an income increase could mean owing money back to the IRS when you file taxes, as you would have received more in PTCs than you were eligible for. Conversely, a decrease in income could make you eligible for larger subsidies, reducing your monthly costs immediately.

Navigating Plan Choices: Balancing Premiums with Out-of-Pocket Costs

The selection of a metal level (Bronze, Silver, Gold, Platinum) is a primary financial decision.

- If you rarely visit the doctor and have significant emergency savings, a Bronze plan with its low premium and high deductible might be financially sensible. You’re protected against catastrophe, and your regular expenses are minimal.

- If you qualify for CSRs, a Silver plan is almost always the financially superior choice due to its dramatically reduced out-of-pocket costs. Even if the premium is slightly higher than a Bronze plan, the savings on deductibles and co-pays often outweigh it.

- If you have chronic conditions or frequently use medical services, a Gold or Platinum plan might be a better value. While premiums are higher, lower deductibles and co-pays mean more predictable, lower costs for each medical encounter, potentially saving you money overall by year-end.

Do a realistic assessment of your health needs and financial risk tolerance. Don’t just look at the premium; consider the total potential cost, including deductibles and out-of-pocket maximums.

The Importance of Annual Re-enrollment for Financial Optimization

Even if you’re happy with your current plan, it is imperative to review your options during Open Enrollment each year. Insurers change their offerings, networks, and prices annually. Your personal financial situation (income, household size) may also have changed.

- Re-evaluating Plan Options: A plan that was the best financial choice last year might not be this year. New, more affordable plans may emerge, or your existing plan’s premium might increase significantly.

- Updating Financial Information: Your income or household size may have changed, affecting your subsidy eligibility. Re-applying ensures your premium tax credit is accurate, preventing surprise tax bills or missed savings.

- Network Changes: Doctors and hospitals can enter or leave networks. Staying informed protects you from unexpected out-of-network costs.

Skipping annual re-enrollment could mean paying more than necessary or missing out on better coverage options. It’s a critical annual financial health check-up.

Beyond Enrollment: Managing Healthcare Costs Throughout the Year

Obtaining ACA coverage is a significant step, but effective financial management of your healthcare extends throughout the year. It involves strategic planning and proactive engagement with your health and your plan.

Budgeting for Healthcare Expenses: From Premiums to Unexpected Care

Integrate healthcare costs into your overall personal budget. This includes:

- Fixed Costs: Your monthly premium is a non-negotiable fixed cost. Budget for this consistently.

- Variable Costs (Anticipated): If you have a chronic condition, regularly see specialists, or take prescription medications, budget for expected co-pays, co-insurance, and prescription costs, particularly before meeting your deductible.

- Emergency Fund: Build or maintain an emergency fund specifically for healthcare. This is crucial for covering your deductible and other out-of-pocket expenses for unexpected illnesses or injuries, preventing medical emergencies from becoming financial catastrophes. Aim to save at least enough to cover your plan’s annual deductible and potentially a portion of your out-of-pocket maximum.

- Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs): If your plan is a High-Deductible Health Plan (HDHP), you might be eligible for an HSA. These tax-advantaged accounts allow you to save money for medical expenses, grow tax-free, and withdraw tax-free for qualified medical costs. FSAs, offered through employers, are similar but have a “use-it-or-lose-it” rule. Leveraging these tools can significantly reduce your taxable income and save you money on healthcare.

Utilizing Preventive Care to Save Money in the Long Run

A financially savvy approach to healthcare includes prioritizing preventive care. Under the ACA, most preventive services—like annual physicals, screenings for blood pressure and cholesterol, mammograms, and immunizations—are covered at no additional cost (no co-pay or deductible) when provided by an in-network provider.

Neglecting preventive care often leads to more serious and expensive health problems down the line. Regular check-ups can detect issues early, when they are easier and cheaper to treat, saving you considerable financial strain in the long run. View preventive care as an investment in your long-term health and financial well-being.

Resources for Financial Planning and Assistance with ACA Coverage

If you find yourself overwhelmed by the financial complexities of the ACA, remember there are resources available:

- Marketplace Navigators and Assisters: These are trained individuals or organizations offering free, unbiased help with the application process, plan selection, and understanding financial assistance. They can help you accurately estimate income and compare plans.

- HealthCare.gov Call Center: The federal marketplace offers a helpline to answer questions about eligibility, plans, and technical issues.

- State Health Insurance Assistance Programs (SHIPs): These programs offer free counseling to Medicare beneficiaries but sometimes have resources or referrals for ACA enrollees as well.

- Tax Professionals: If you have complex income situations or questions about how Premium Tax Credits affect your tax return, a qualified tax professional can provide tailored advice.

Don’t hesitate to seek help. Navigating healthcare finance can be intricate, and expert guidance can ensure you make the most financially beneficial decisions for your situation.

Conclusion

The question “how do I get Obamacare” is not just about gaining access to health insurance; it’s a critical inquiry into personal finance, risk management, and smart budgeting. By understanding the financial structure of the ACA, diligently gathering your income information, strategically selecting plans based on metal levels and your health needs, and proactively managing your coverage year-round, you can secure essential healthcare while safeguarding your financial health. The ACA marketplace, with its subsidies and consumer protections, offers a robust framework for affordable coverage, but its true financial benefit is realized through informed decision-making and a proactive approach to your healthcare investment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.