Car insurance is often viewed through the lens of a legal requirement—a necessary box to check before hitting the road. However, from a personal finance perspective, car insurance is a critical pillar of risk management. It is a financial instrument designed to protect your net worth from the catastrophic costs associated with vehicular accidents, theft, and liability claims. Without the right policy, a single moment of misfortune could derail your long-term financial goals, draining savings accounts or leading to prolonged litigation.

Understanding how to get car insurance is not merely about finding the lowest monthly payment; it is about finding the optimal balance between cost and protection. This guide explores the systematic process of securing coverage while treating your policy as a strategic financial asset.

Assessing Your Financial Risk and Coverage Requirements

Before you begin soliciting quotes from providers, you must perform a self-audit of your financial situation. The goal of insurance is to transfer risk from yourself to a third party (the insurer). To do this effectively, you must understand what risks you are exposed to and how much of that risk you can afford to retain.

Determining the Right Coverage Limits

Most states mandate a minimum amount of liability coverage. While these minimums are the cheapest way to stay legal, they are rarely sufficient for comprehensive financial protection. If you are at fault in an accident that causes $100,000 in medical bills but your policy only covers $25,000, your personal assets—including your home, savings, and future wages—could be targeted to cover the difference. Savvy financial planning suggests choosing limits that align with your total net worth.

The Deductible Dilemma: Balancing Liquidity and Premiums

The deductible is the amount you pay out of pocket before your insurance kicks in. In the world of personal finance, the deductible is a lever used to control your premium costs. A higher deductible typically results in a lower monthly premium. If you have a robust emergency fund, opting for a $1,000 or $1,500 deductible can save you significant money over the life of the policy. Conversely, if your cash flow is tight, a lower deductible ensures that a car accident doesn’t become an immediate liquidity crisis.

Evaluating Optional Protections

Beyond basic liability, you must decide if your financial situation requires Collision and Comprehensive coverage. If you are driving a brand-new vehicle or have an outstanding auto loan, these are usually mandatory. However, if you are driving an older vehicle with a low market value, the cost of the premiums may eventually exceed the potential payout. This is where “self-insuring” for physical damage—dropping collision coverage and setting that money aside in a high-yield savings account—becomes a viable financial strategy.

The Systematic Approach to Securing a Policy

Once you have defined your needs, the next step is the procurement process. This should be approached with the same rigor you would apply to an investment or a major purchase.

Gathering Your Financial and Vehicle Documentation

Efficiency is key when shopping for insurance. To get the most accurate quotes, you need to have specific data points ready. This includes your Vehicle Identification Number (VIN), current mileage, and your driving history. From a financial standpoint, you should also have your current policy’s “Declarations Page” on hand. This allows you to compare new quotes against your existing coverage line-by-line, ensuring you aren’t sacrificing protection for a lower price tag.

The Comparative Shopping Method

The insurance market is highly fragmented, and pricing algorithms vary wildly between companies. Some insurers prefer “low-risk” drivers with high credit scores, while others specialize in “non-standard” drivers. To ensure you are getting the best market rate, you should obtain at least three to five quotes. You can do this through:

- Captive Agents: Who represent a single company (e.g., State Farm or Allstate).

- Independent Brokers: Who can shop across multiple carriers to find the best rate.

- Direct-to-Consumer Portals: Online platforms that allow for immediate digital enrollment.

Understanding the Underwriting Process

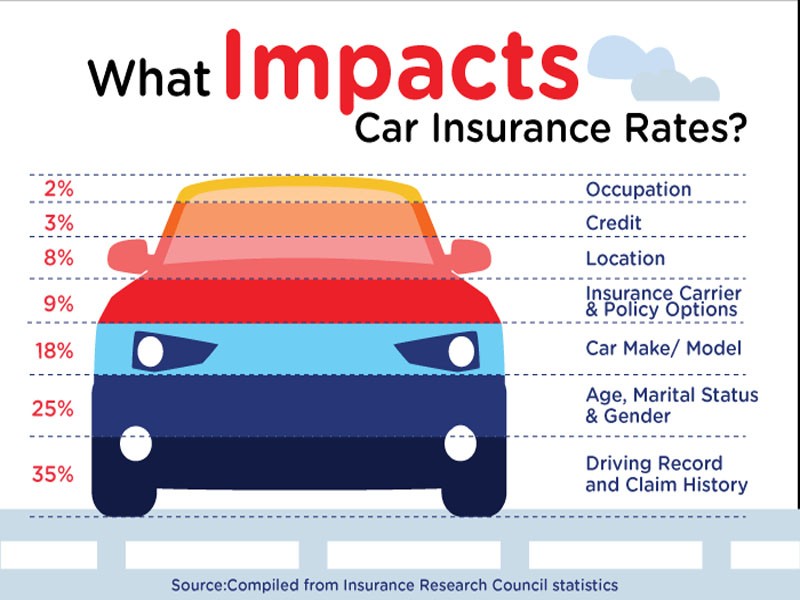

When you apply for a policy, the insurer performs “underwriting”—the process of evaluating the risk you pose. They look at your credit-based insurance score, your history of claims, and even your zip code. Understanding that these factors influence your premium allows you to take steps to improve your “insurability” over time, such as maintaining a clean driving record and improving your credit score to unlock lower rates in the future.

Optimizing Costs Through Financial Discipline

Getting car insurance is not a “set it and forget it” task. To maintain financial efficiency, you must actively manage the factors that influence your premiums.

Leveraging Your Credit Score for Lower Premiums

In many jurisdictions, there is a strong correlation between financial responsibility and driving safety. Insurance companies have found that individuals with higher credit scores tend to file fewer claims. By managing your debt-to-income ratio and ensuring timely payments on other financial obligations, you are indirectly lowering your car insurance costs. If your credit score has improved significantly since you last purchased a policy, it is often worth re-shopping your insurance to capture the “credit-based” discount.

Maximizing Discounts and Bundling Strategies

One of the most effective ways to reduce the “Total Cost of Ownership” for your vehicle is through bundling. Most insurers offer substantial discounts if you carry both your auto and homeowners (or renters) insurance with them. Additionally, look for “affinity discounts.” Many professional organizations, alumni associations, and even specific employers have negotiated group rates with major insurers. These small percentages add up to significant annual savings when compounded over several years.

Telematics and Usage-Based Insurance (UBI)

For those who are confident in their driving habits or who do not drive many miles, telematics offers a way to pay only for the risk you actually create. By using a smartphone app or a plug-in device, insurers track your braking, acceleration, and mileage. If the data shows you are a low-risk driver, you can see premium reductions of 10% to 40%. This is a data-driven way to align your insurance costs with your actual behavior.

Making the Purchase and Post-Purchase Management

The final stage of getting car insurance is the execution and ongoing maintenance of the contract.

Reviewing the Binder and Finalizing the Contract

Once you select a provider, you will receive an “insurance binder.” This is a temporary document that proves you have coverage until the formal policy is issued. It is vital to review this document to ensure that the limits, deductibles, and “Named Insured” individuals are listed correctly. In the world of finance, the “fine print” matters; ensure there are no exclusions that could leave you vulnerable, such as restrictions on “permissive use” (letting a friend drive your car).

Performing Annual Policy Audits

Your life is dynamic, and your insurance should reflect that. A policy that was perfect for you as a single renter might be entirely inadequate once you get married, buy a home, or start a business. An annual financial check-up should include an insurance review. If you have started working from home permanently, your annual mileage has likely dropped, which could qualify you for a “low-mileage” discount. If your car has aged significantly, it might be time to remove collision coverage.

Managing Claims with a Financial Mindset

If an accident occurs, the decision to file a claim is a financial one. If the damage is only slightly above your deductible, it may be more cost-effective to pay for the repairs out of pocket. Filing a claim often leads to a “surcharge” on your premium for the next three to five years. By calculating the “break-even” point—the point where the insurance payout exceeds the cumulative cost of increased future premiums—you can make a rational decision that protects your long-term wealth.

Conclusion: Insurance as a Wealth Preservation Tool

Learning how to get car insurance is an essential skill in the broader context of personal finance. It is not just about legality; it is about building a safety net that allows you to pursue your financial goals without the fear of a single accident causing insolvency. By understanding coverage types, shopping competitively, leveraging your financial habits for discounts, and regularly auditing your policy, you transform a mundane monthly expense into a sophisticated tool for wealth preservation. In the grand scheme of your financial life, the right car insurance policy provides something far more valuable than a payout: it provides the peace of mind to focus on your journey ahead.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.