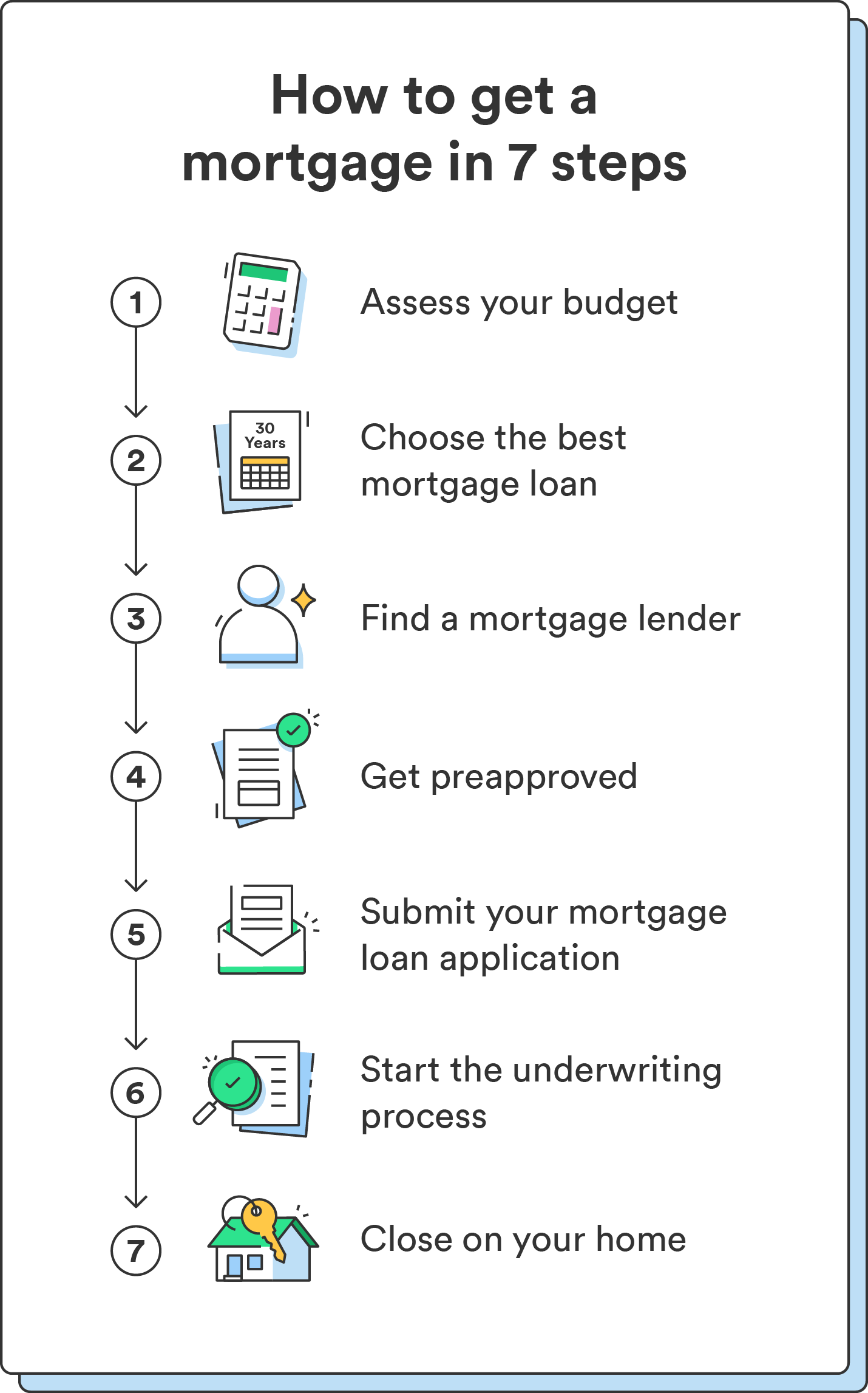

Securing a mortgage is often the single most significant financial transaction an individual will undertake in their lifetime. It is a complex interplay of personal creditworthiness, market conditions, and long-term financial planning. While the prospect of owning a home is a cornerstone of wealth-building, the process of obtaining the necessary financing can be daunting for the uninitiated. To successfully navigate this journey, one must understand that a mortgage is not merely a loan, but a structured financial instrument that requires meticulous preparation, strategic timing, and a deep understanding of one’s own fiscal health.

1. Establishing Your Financial Foundation

Before stepping into a real estate office or browsing online listings, the process of getting a mortgage begins with a rigorous audit of your personal finances. Lenders are risk-averse by nature; their goal is to ensure that you have the stability and the resources to repay a debt that will likely span three decades.

Understanding the Role of Credit Scores

Your credit score is the primary metric lenders use to determine your reliability as a borrower. It influences not only whether you will be approved but also the interest rate you will be offered. A higher score—typically 740 or above—grants access to the most competitive rates, which can save a homeowner tens of thousands of dollars over the life of the loan. Conversely, a score below 620 may limit your options to specific government-backed programs. It is essential to pull your credit reports months in advance to identify and dispute any inaccuracies that could unnecessarily drag down your score.

Calculating the Debt-to-Income (DTI) Ratio

Lenders look closely at your Debt-to-Income (DTI) ratio to gauge how much of your monthly income is already committed to other obligations. This ratio is calculated by dividing your total monthly debt payments (student loans, car notes, credit cards) by your gross monthly income. Ideally, lenders prefer a DTI ratio of 36% or lower, though some programs allow up to 43% or even 50% in certain circumstances. Reducing outstanding high-interest debt before applying for a mortgage not only improves this ratio but also frees up cash flow for your future monthly housing expenses.

Accumulating the Down Payment and Closing Costs

The “20% down payment” is a well-known benchmark, but it is not a strict requirement for many modern mortgage products. However, the size of your down payment remains a critical lever in your financial strategy. A larger down payment reduces the principal loan amount, lowers monthly payments, and eliminates the need for Private Mortgage Insurance (PMI). Beyond the down payment, you must also budget for closing costs, which typically range from 2% to 5% of the home’s purchase price. These funds must be “seasoned,” meaning they have sat in your bank account for several months, allowing lenders to verify the source of the capital.

2. Navigating Loan Types and Pre-Approval

Once your financial house is in order, the next step is to identify the specific type of mortgage that aligns with your financial goals. Not all loans are created equal, and the right choice depends on your long-term residency plans and your risk tolerance.

The Power of Pre-Approval

In a competitive real estate market, a pre-approval letter is your most valuable asset. Unlike pre-qualification—which is a superficial estimate based on self-reported data—pre-approval involves a lender verifying your income, assets, and credit. This process provides you with a specific loan amount for which you are eligible, allowing you to shop with confidence and signaling to sellers that you are a serious, qualified buyer.

Conventional vs. Government-Backed Loans

Borrowers generally choose between two main paths: conventional loans or government-backed loans. Conventional loans are not insured by the federal government and usually require higher credit scores and down payments, but they offer more flexibility and may be cheaper for those with excellent credit. Government-backed options, such as FHA loans (geared toward those with lower credit scores or smaller down payments) and VA loans (reserved for veterans and active-duty service members with 0% down payment options), provide vital pathways to homeownership for those who may not meet the stringent requirements of conventional lending.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The structure of your interest rate is a fundamental financial decision. A fixed-rate mortgage offers stability; your interest rate and monthly principal and interest payments remain the same for the entire 15 or 30-year term. This is often the preferred choice for those planning to stay in their home long-term. An Adjustable-Rate Mortgage (ARM), however, typically starts with a lower “teaser” rate for a set period (such as five or seven years) before adjusting based on market indices. ARMs can be strategic for those who plan to sell or refinance before the adjustment period begins, but they carry the inherent risk of rising payments in a high-interest environment.

3. The Mortgage Application and Underwriting Process

With a pre-approval in hand and a property under contract, you move into the formal application phase. This is where the lender’s scrutiny intensifies, and the “underwriting” process begins.

Compiling Essential Documentation

The documentation required for a mortgage is exhaustive. You will need to provide W-2 statements from the last two years, recent pay stubs covering at least 30 days, and full bank statements for the past two months. If you are self-employed, you will likely need to provide comprehensive federal tax returns for the previous two years and a year-to-date profit and loss statement. Precision is key here; any discrepancy in your paperwork can stall the approval process.

The Role of the Underwriter

The underwriter is the final arbiter of your loan. Their job is to verify every piece of information provided and ensure that the loan meets the lender’s specific criteria. During this phase, they will order an appraisal of the property to ensure its value matches the purchase price. They may also issue “conditions”—requests for additional information, such as an explanation for a large deposit in your bank account or proof that a previous debt has been settled. It is vital to respond to these requests immediately to maintain the momentum of the transaction.

Avoiding Financial Changes During Underwriting

One of the most common mistakes borrowers make is altering their financial profile while the loan is in underwriting. Opening a new credit card, financing a new car, or moving large sums of money between accounts can trigger a re-evaluation of your creditworthiness and potentially lead to a loan denial. From the moment you apply until the moment you sign the final documents at closing, your financial situation should remain as static as possible.

4. Finalizing the Transaction: Closing and Beyond

The final stage of the mortgage process is the “closing” or “settlement,” where the legal transfer of the property occurs and the loan is officially funded.

Reviewing the Closing Disclosure

At least three days before your closing date, your lender is legally required to provide you with a Closing Disclosure (CD). This document outlines the final terms of your loan, including the exact interest rate, the monthly payment, and the “cash to close”—the total amount you must bring to the table. It is crucial to compare this document against the “Loan Estimate” you received at the start of the process to ensure there are no unexpected fees or changes in terms.

The Significance of the Appraisal and Inspection

While the appraisal is for the lender’s protection, the home inspection is for yours. A mortgage is a massive financial commitment, and you must ensure the underlying asset is sound. If the appraisal comes in lower than the purchase price, it creates an “appraisal gap” that must be resolved through negotiation with the seller or by paying the difference out of pocket, as the lender will only provide a loan based on the appraised value, not the contract price.

Embracing the Responsibility of Homeownership

Once the papers are signed and the keys are in hand, the focus shifts from obtaining the mortgage to managing it. Strategic financial management involves more than just making monthly payments. Homeowners should consider the benefits of making extra principal payments to reduce the total interest paid over time or monitoring market trends for future refinancing opportunities that could lower their monthly costs. A mortgage is not just a debt; it is a tool for building equity and long-term financial security.

By understanding these phases—from the initial credit check to the final signature—you transform the mortgage process from a confusing hurdle into a manageable, strategic financial move. Homeownership is a marathon, not a sprint, and a well-structured mortgage is the foundation upon which your financial future is built.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.