For many Americans, the Internal Revenue Service (IRS) is a source of significant financial anxiety. The uncertainty of whether you owe back taxes, interest, or penalties can hover over your personal finances like a dark cloud. Whether you’ve misplaced your records, missed a filing deadline, or simply want to ensure your financial house is in order, knowing exactly where you stand with the federal government is a critical component of healthy financial management.

In the modern financial landscape, the days of waiting weeks for a paper letter to arrive are largely behind us. The IRS has integrated various digital tools and streamlined processes to help taxpayers identify their liabilities in real-time. This guide provides a detailed roadmap on how to determine if you owe the IRS, how to interpret the findings, and what strategic steps to take to resolve your balance.

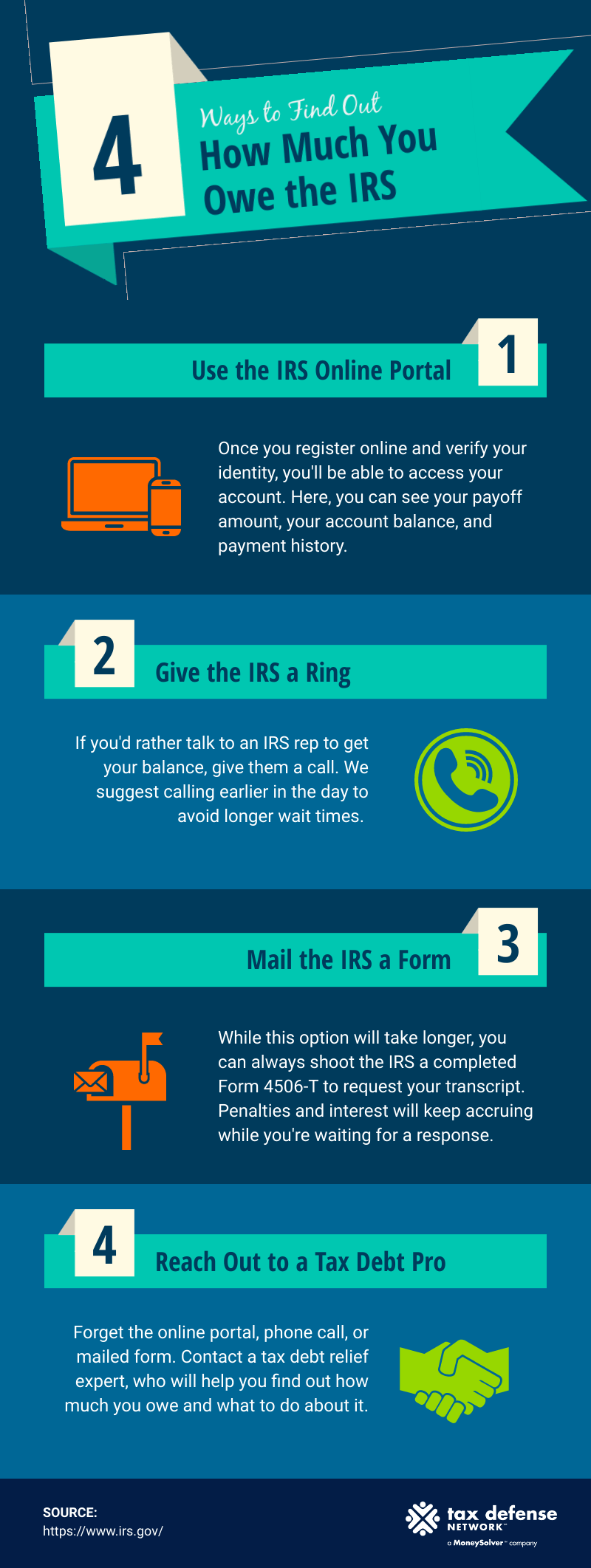

Navigating the IRS Online Portal: The Most Direct Route

The most efficient way to check your tax status is through the official IRS website. In recent years, the agency has invested heavily in its digital infrastructure to provide taxpayers with a “Self-Service” experience that mirrors modern banking.

Creating and Verifying Your ID.me Account

To access your sensitive financial data, the IRS requires a high level of identity verification. They currently partner with ID.me, a third-party service provider that meets federal standards for digital identity protection. To find out if you owe money, you must first create an account. This process involves uploading a government-issued photo ID (like a driver’s license or passport) and performing a “video selfie” to ensure that the person accessing the records is indeed the taxpayer. While this may seem cumbersome, it is a vital security measure to prevent identity theft and fraudulent access to your financial history.

Understanding Your Account Balance and Payment History

Once your identity is verified and you log into your IRS Online Account, the dashboard provides an immediate snapshot of your financial standing. You can see your “Total Amount Owed,” which is broken down by the tax year.

It is important to look closely at the components of this balance. The portal distinguishes between the principal tax amount, the accrued interest, and any assessed penalties (such as late filing or late payment fees). Furthermore, the portal allows you to view your payment history for the last 24 months, including any scheduled or pending payments. This transparency allows you to cross-reference the IRS records with your own bank statements to ensure every dollar you’ve paid has been accurately credited.

Alternative Methods for Checking Your Tax Status

While the online portal is the fastest method, it is not the only way to obtain information. For those who prefer paper trails or are dealing with complex historical issues, other avenues exist to verify tax liability.

Requesting a Tax Transcript

A tax transcript is a summary of your tax return or your overall account status. If you are unsure if you owe money from several years ago, you can request a “Tax Account Transcript.” Unlike a “Return Transcript,” which just shows what you reported on your 1040, the Account Transcript shows any subsequent adjustments made by the IRS, payments made, and any remaining balance.

You can request these transcripts online for immediate viewing or by mail. For those who suspect they might owe money but haven’t received a notice, the Account Transcript is the ultimate “truth document” in the eyes of the IRS. It provides a line-by-line history of every action taken on your account for a specific tax year.

Deciphering Official IRS Notices and Letters

The IRS is legally required to notify you via mail if they believe you owe money or if they have adjusted your return. These notices, such as the CP2000 or the CP501, are often the first sign of a tax liability.

- CP2000: This is an “under-reporting” notice. It occurs when the information reported to the IRS by your employer or bank (via W-2s or 1099s) does not match what you reported on your tax return.

- CP501: This is a formal notice that you have a balance due on one of your tax accounts.

Ignoring these letters is a significant financial mistake. The IRS assumes that if you do not respond within the allotted timeframe (usually 30 to 60 days), you agree with their assessment. Regularly checking your physical mail and maintaining an updated address with the IRS ensures you never miss these critical financial alerts.

Proactive Financial Management: Why Knowing Your Balance Matters

Understanding your tax liability is not just about avoiding trouble; it is a fundamental part of personal financial planning. Unpaid taxes are a form of high-interest debt that can derail your long-term wealth-building efforts.

Avoiding Penalties and Accrued Interest

The IRS charges a “failure to pay” penalty of 0.5% of the unpaid taxes for each month or part of a month the tax remains unpaid, up to 25%. Additionally, the interest rate on underpayments is adjusted quarterly and is currently significantly higher than what you would earn in a standard savings account.

By identifying that you owe money early, you can stop the bleeding. Even if you cannot pay the full amount immediately, filing your return on time reduces the “failure to file” penalty, which is much steeper (5% per month) than the failure to pay penalty. Total financial awareness allows you to prioritize tax debt over lower-interest liabilities.

The Impact on Your Credit and Future Financial Goals

While the IRS no longer reports tax liens to the three major credit bureaus in the same way they used to, a significant tax debt still impacts your financial mobility. For instance, if you are applying for a mortgage or a business loan, lenders will often require tax transcripts. If those transcripts show an outstanding balance without a payment plan, your loan application could be denied.

Furthermore, the IRS has the power to issue a “Notice of Federal Tax Lien,” which is a public document that notifies creditors that the government has a legal right to your property. This can make it nearly impossible to sell a home or refinance debt until the tax issue is resolved.

Strategic Solutions if You Do Owe the IRS

If you use the tools mentioned above and discover that you do, in fact, owe the IRS, do not panic. The IRS is generally more interested in collecting the money over time than in pursuing aggressive legal action, provided you are communicative and proactive.

Short-Term and Long-Term Payment Plans

The IRS offers “Installment Agreements” for taxpayers who cannot pay their balance in full.

- Short-term Payment Plan: If you can pay the full amount within 180 days, you can apply for a short-term extension. This often carries lower setup fees than a long-term plan.

- Long-term Payment Plan (Installment Agreement): If you need more than six months, you can set up a monthly payment plan. This can last for up to 72 months. Setting this up via direct debit from your bank account can sometimes reduce the administrative fees associated with the agreement.

Offer in Compromise and Currently Not Collectible Status

For individuals facing extreme financial hardship, the IRS offers more drastic forms of relief.

- Offer in Compromise (OIC): This allows you to settle your tax debt for less than the full amount you owe. However, the IRS has very strict criteria for this; they will look at your income, expenses, and asset equity to determine if the amount they are asking for is truly uncollectible.

- Currently Not Collectible (CNC): If you can prove that paying the tax debt would prevent you from meeting basic living expenses, the IRS may place your account in CNC status. This doesn’t wipe away the debt, but it temporarily stops collection activities like wage garnishments or bank levies.

Modern Financial Tools for Ongoing Tax Compliance

The best way to find out you owe the IRS is to never owe them in the first place. Incorporating tax planning into your monthly financial routine is the hallmark of a savvy investor or business owner.

Using Tax Withholding Estimators

The IRS provides a “Tax Withholding Estimator” tool on their website. This is particularly useful for W-2 employees who have seen changes in their life circumstances—such as marriage, the birth of a child, or a significant raise. By inputting your current pay stubs, the tool helps you determine if you are withholding enough from your paycheck to cover your year-end liability. Adjusting your W-4 based on these results can prevent a “surprise” bill in April.

![]()

Quarterly Payments for Freelancers and Business Owners

In the era of the side hustle and gig economy, many people find themselves owing money because they forget that taxes are not automatically withheld from 1099 income. If you expect to owe more than $1,000 in taxes for the year, you are generally required to make quarterly estimated tax payments.

Using financial software to track your business expenses and income in real-time allows you to set aside a percentage of every dollar earned (typically 25-30%) into a high-yield savings account dedicated solely to taxes. This ensures that when the quarterly deadlines arrive, the funds are already available, and you aren’t forced to dip into your personal savings or emergency fund to satisfy the IRS.

By utilizing the digital tools provided by the IRS, maintaining a vigilant eye on your mail, and treating tax liability as a core component of your personal balance sheet, you can navigate the complexities of federal taxes with confidence. Knowledge is the first step toward financial freedom; knowing exactly what you owe allows you to build a strategy to pay it off and move forward with your broader financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.