For many, the question “How do i file my taxes?” is met with a mix of anxiety and procrastination. However, in the realm of personal finance, tax filing is not merely a legal obligation; it is a critical pillar of wealth management and financial health. Navigating the complexities of the tax code requires more than just filling out forms—it requires a strategic understanding of how your income, investments, and expenses interact with current legislation.

This comprehensive guide breaks down the filing process into actionable steps, ensuring you not only remain compliant with the law but also maximize your potential for a refund or minimize your liability through savvy financial planning.

1. Establishing the Foundation: Documentation and Organization

The quality of your tax return is directly proportional to the quality of your record-keeping. Before you even open a filing software or meet with a professional, you must aggregate the data that defines your financial year. In the “Money” niche, we view this as an annual audit of your personal cash flow.

Gathering Income Statements

Your first task is to collect all documents that prove your “gross income.” For most employees, this is the W-2 form. However, in an increasingly diversified economy, you may have multiple streams of income. This includes 1099-NEC forms for freelance work, 1099-INT for interest earned in savings accounts, and 1099-DIV for dividends from your investment portfolio. If you have sold assets, such as stocks or real estate, you will also need your 1099-B forms to calculate capital gains or losses.

Tracking Adjustments and Deductions

To arrive at your Adjusted Gross Income (AGI), you must identify “above-the-line” deductions. These are powerful financial tools because they reduce your taxable income regardless of whether you itemize. Common adjustments include contributions to a traditional IRA, interest paid on student loans, and contributions to a Health Savings Account (HSA). Having these receipts and statements ready is the difference between a high tax bill and a lean one.

Determining Your Filing Status

Your filing status is a foundational financial decision. Whether you file as Single, Married Filing Jointly, Married Filing Separately, or Head of Household dictates your standard deduction amount and your tax brackets. For example, the “Head of Household” status offers more favorable rates and a higher standard deduction than filing as “Single,” but it requires strict adherence to dependency and household maintenance rules.

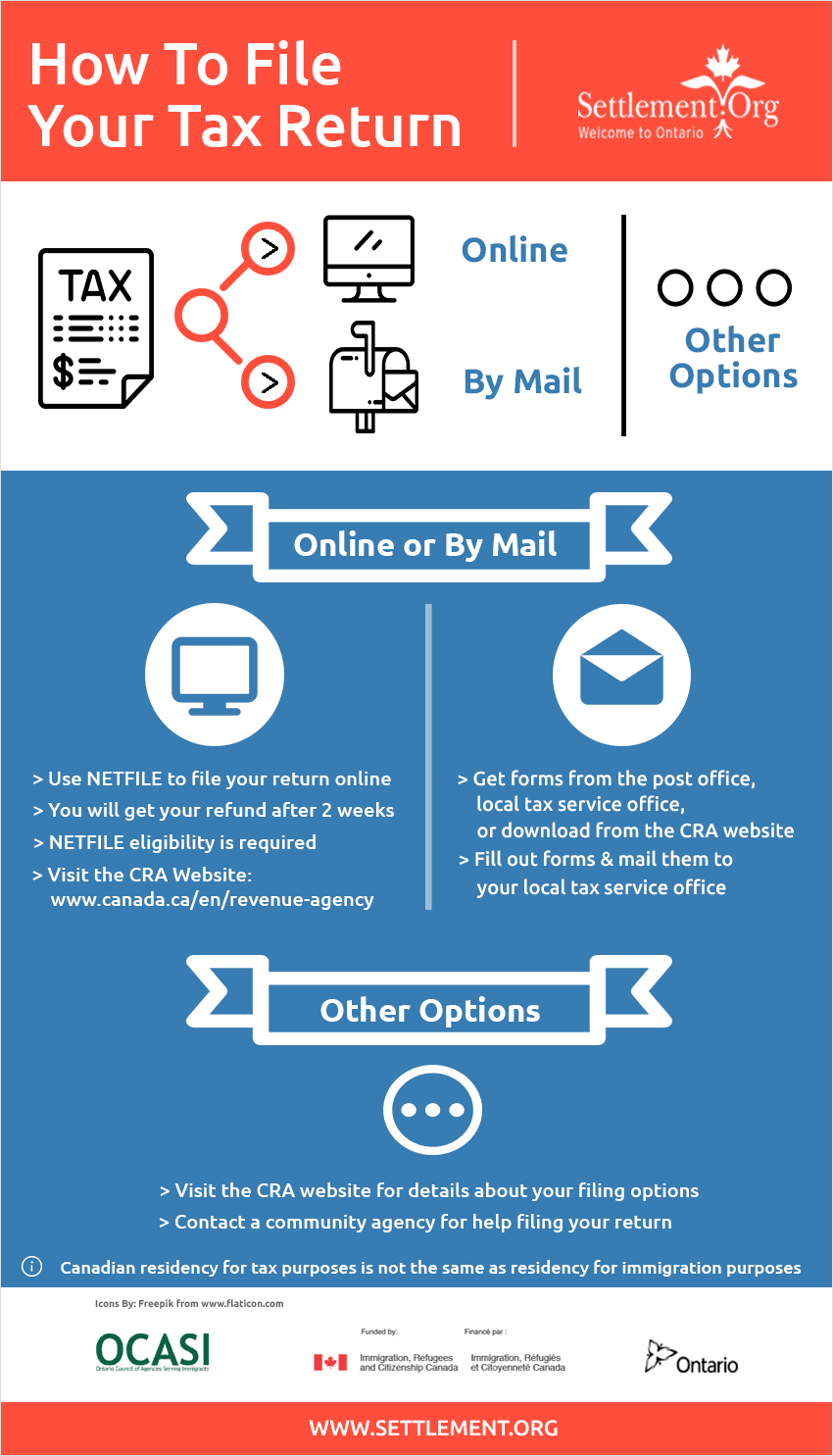

2. Strategic Choosing: Deciding How to File

Once your documentation is in order, the next strategic move is choosing the delivery method for your return. This decision should be based on the complexity of your financial life and the value you place on your time versus the cost of professional expertise.

The DIY Approach: Tax Software and Free File

For individuals with straightforward financial situations—such as a single W-2 and no complex investments—tax software is often the most cost-effective route. The IRS “Free File” program provides access to brand-name software for those under a certain income threshold. From a financial perspective, this method is efficient, but it places the burden of accuracy entirely on the taxpayer. It is best suited for those who are comfortable navigating digital interfaces and have basic financial literacy.

The Professional Route: CPAs and Enrolled Agents

As your net worth grows and your financial portfolio diversifies, the “ROI” (Return on Investment) of hiring a Certified Public Accountant (CPA) or an Enrolled Agent (EA) increases. If you own a business, manage rental properties, or have complex international investments, a professional can identify nuances in the tax code that software might miss. They offer more than just filing; they provide year-round tax planning strategies that can save you thousands of dollars in the long run.

Manual Filing: The Paper Method

While still an option, filing via paper is generally discouraged in modern finance. It significantly increases the risk of calculation errors and delays the processing of any potential refund. From a digital security and financial efficiency standpoint, e-filing with direct deposit is the gold standard for modern money management.

3. Maximizing the Return: Deductions vs. Tax Credits

Understanding the mechanics of how the government reduces your tax liability is essential for long-term wealth building. Many taxpayers confuse deductions with credits, but they function very differently within your financial ecosystem.

Standard Deduction vs. Itemized Deductions

Every year, you must choose between taking the standard deduction (a flat amount set by the IRS) or itemizing your deductions (listing specific expenses). In recent years, the standard deduction has increased significantly, making itemization less common. However, if your mortgage interest, state and local taxes (SALT), and charitable contributions exceed the standard deduction threshold, itemizing is the superior financial move. This requires meticulous receipt-tracking throughout the year.

The Power of Tax Credits

If a deduction is a “discount” on the income you are taxed on, a credit is a “gift card” applied directly to the tax you owe. Credits are far more valuable.

- The Earned Income Tax Credit (EITC): A significant boon for low-to-moderate-income working individuals.

- The Child Tax Credit: Provides substantial relief for families.

- Education Credits: The American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) help offset the high costs of higher education.

Strategically qualifying for these credits can effectively bring a taxpayer’s liability down to zero or even result in a “refundable” payment from the government.

Managing Capital Gains and Losses

For investors, filing taxes involves the strategic use of Tax-Loss Harvesting. If you have sold stocks at a loss, you can use those losses to offset your capital gains. If your losses exceed your gains, you can even use up to $3,000 of the excess loss to offset your ordinary income. This is a sophisticated financial maneuver that turns a market downturn into a tax advantage.

4. Navigating the Modern Economy: Side Hustles and Small Business

The rise of the “gig economy” has changed the way millions of people file taxes. If you earn income outside of a traditional employer-employee relationship, your tax responsibilities shift from passive to active.

Self-Employment Tax

When you work for an employer, they pay half of your Social Security and Medicare taxes. When you are self-employed (a freelancer, driver, or consultant), you are responsible for both the employer and employee portions, totaling 15.3%. In the “Money” niche, we refer to this as the “Self-Employment Tax.” Understanding this is vital for pricing your services; if you don’t account for this 15.3% in your rates, you are effectively taking a massive pay cut.

Business Expense Deductions

The silver lining of self-employment is the ability to deduct “ordinary and necessary” business expenses. This includes a portion of your home office, equipment, marketing costs, and even professional development. By lowering your business’s net profit, you lower both your income tax and your self-employment tax. This is where the intersection of business finance and personal filing becomes most profitable.

Estimated Quarterly Payments

The U.S. tax system is a “pay-as-you-go” system. If you expect to owe more than $1,000 in taxes from your side hustle, you are generally required to make quarterly estimated payments. Failing to do so can result in underpayment penalties. Managing these payments is a core skill in business finance, ensuring you don’t face a massive, unmanageable bill come April.

5. Post-Filing Strategy: Looking Toward Future Wealth

Filing your taxes shouldn’t be an isolated event that ends on April 15th. Instead, it should serve as a diagnostic tool for your overall financial strategy for the coming year.

Analyzing Your Refund or Balance Due

A large refund is often celebrated, but in the world of personal finance, it is essentially an interest-free loan you gave to the government. Conversely, a large balance due can lead to penalties. The goal of a savvy financial manager is to get as close to $0 as possible. If your refund was substantial, consider adjusting your W-4 withholding at work to increase your take-home pay throughout the year, allowing you to invest that money sooner.

Audit Protection and Record Retention

Once you hit “submit,” your job isn’t entirely over. You must maintain your records for at least three to seven years, depending on the complexity of your return. This includes digital copies of all 1099s, W-2s, and receipts for itemized deductions. Organization today prevents a financial catastrophe in the event of an IRS audit tomorrow.

Tax-Advantaged Investing for the New Year

Use the insights gained from your tax return to plan your investment strategy. If you found your taxable income was too high, look into increasing contributions to a 401(k) or 403(b) to lower your future AGI. If you expect to be in a higher tax bracket in the future, consider a Roth IRA, where you pay taxes now to enjoy tax-free withdrawals in retirement.

By viewing the question of “how do i file my taxes” through the lens of comprehensive money management, you transform a tedious chore into a powerful mechanism for building and protecting your wealth. Understanding the nuances of the code, choosing the right filing method, and leveraging credits and deductions ensures that you keep more of what you earn, providing a solid foundation for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.