Understanding how to calculate percent reduction is more than just a mathematical exercise; it is a fundamental skill in the world of finance. Whether you are tracking the progress of a debt repayment plan, evaluating the performance of an investment portfolio during a market downturn, or trimming operational costs in a growing business, the ability to quantify a decrease in value as a percentage provides a clear, standardized metric for success.

In the realm of money management, percentages offer a perspective that raw numbers often obscure. A $500 reduction in expenses means something very different to a household with a $2,000 monthly budget than it does to a corporation with a $2,000,000 budget. By converting these changes into percentages, we gain the ability to compare performance across different scales and timeframes.

The Fundamentals of Percent Reduction in Personal Finance

At its core, percent reduction measures the extent to which a value has decreased relative to its original starting point. In personal finance, this is the primary tool used to measure progress toward financial freedom and efficiency.

The Basic Formula for Financial Calculations

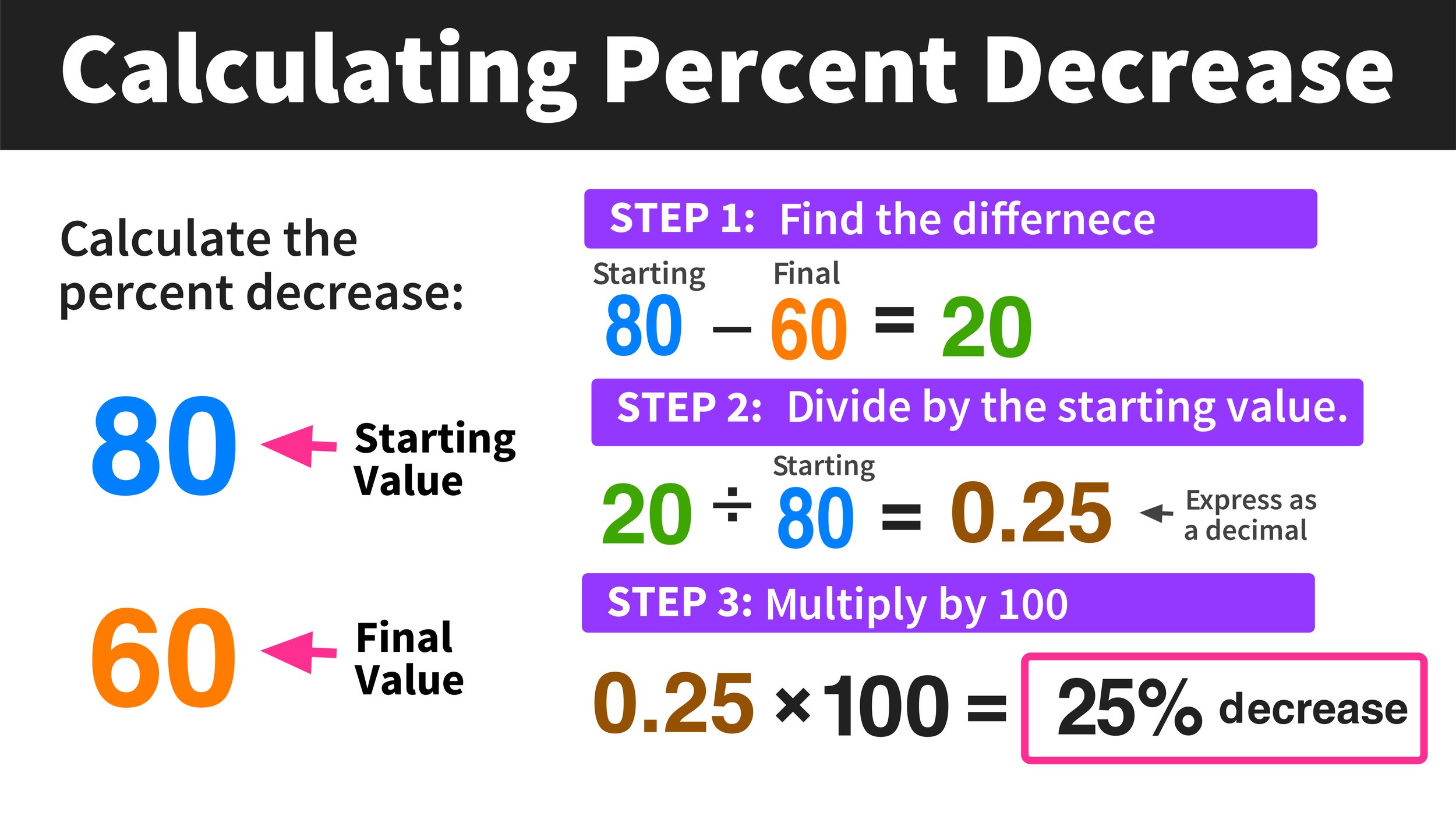

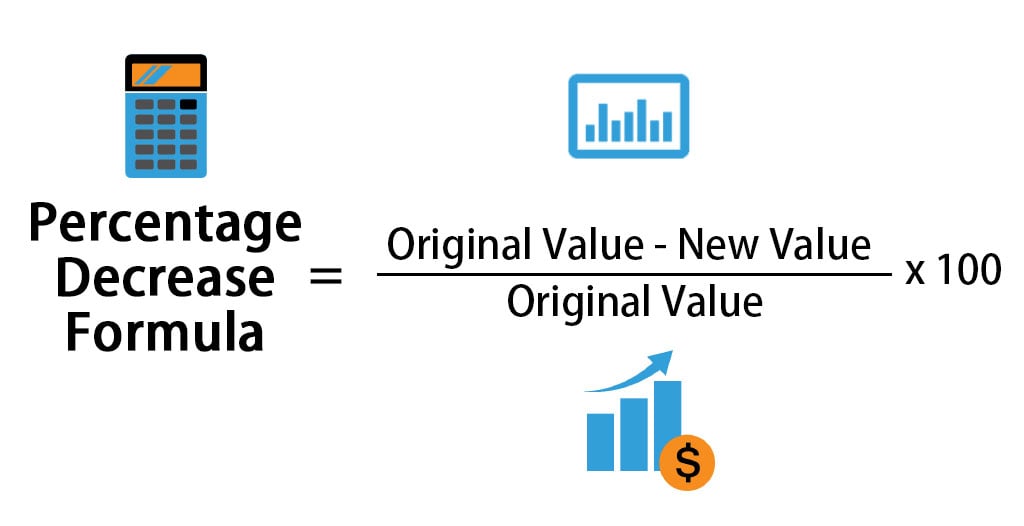

To calculate percent reduction, you need two figures: the original value and the new (lower) value. The formula is straightforward:

((Original Value – New Value) / Original Value) × 100 = Percent Reduction

For example, if your monthly grocery bill was $800 and you managed to lower it to $600 through disciplined meal planning, the calculation would be:

($800 – $600) / $800 = 0.25.

Multiplying by 100 gives you a 25% reduction. This percentage serves as a Key Performance Indicator (KPI) for your household management, allowing you to see exactly how much “waste” has been eliminated.

Tracking Debt Reduction and Interest Savings

One of the most impactful applications of this calculation is in debt management. When following strategies like the “Debt Snowball” or “Debt Avalanche,” tracking the percent reduction of your total principal provides a psychological boost.

Beyond just the principal, calculating the percent reduction in interest paid is vital. If you refinance a mortgage from a 7% interest rate to a 5% rate, you aren’t just saving 2 percentage points; you are calculating the reduction in the cost of the loan. On a large balance, a small percent reduction in the interest rate can equate to a massive percent reduction in the total interest paid over the life of the loan, often reaching 20% or 30% of the total debt cost.

Analyzing Budgetary Expense Cuts

Effective wealth building is often less about how much you earn and more about the “burn rate” of your capital. By applying percent reduction analysis to your recurring subscriptions, utility bills, and discretionary spending, you can identify which areas of your life offer the most significant opportunities for optimization. A 10% reduction across five major spending categories often yields more long-term wealth than a 50% reduction in a single, minor category.

Evaluating Investment Performance and Risk Management

In the world of investing, percent reduction—often referred to as “drawdown”—is a critical metric for assessing risk and volatility. Understanding these numbers helps investors stay rational during market fluctuations.

Calculating Portfolio Drawdowns

A drawdown is the percent reduction from a portfolio’s peak value to its lowest point before a new peak is achieved. For instance, if an investment account hits a high of $100,000 and subsequently drops to $80,000 during a market correction, it has experienced a 20% reduction.

Investors must monitor these percentages closely because they dictate the “math of recovery.” It is a sobering reality of finance that the percent increase required to recover from a reduction is always higher than the reduction itself. A 10% drop requires an 11.1% gain to break even, but a 50% drop requires a 100% gain. Understanding this relationship is essential for setting stop-loss orders and managing risk exposure.

The Impact of Volatility on Compounded Returns

Percent reduction also plays a role in understanding “variance drain.” If an investment fluctuates wildly—gaining 20% one year and losing 20% the next—the net result is actually a 4% reduction from the original principal ($100 + 20% = $120; $120 – 20% = $96). By calculating the percent reduction caused by volatility, sophisticated investors can opt for “boring” assets with lower reductions, which often outperform volatile assets over long horizons due to the power of compounding.

Understanding Tax Efficiency and Net Reductions

For high-net-worth individuals, the focus shifts from gross returns to net returns after taxes. Calculating the percent reduction in your returns caused by capital gains taxes or management fees is crucial. If your portfolio grows by 10%, but taxes and fees account for a 3% reduction of that total value, your effective growth rate is significantly hampered. Professional wealth management focuses heavily on minimizing these specific percent reductions to maximize the “internal rate of return.”

Business Finance and Operational Efficiency

For business owners and financial officers, percent reduction is the language of efficiency. It is used to justify investments in new technology, negotiate with suppliers, and streamline operations.

Measuring Cost of Goods Sold (COGS) Reductions

In a business context, the “bottom line” is often protected by reducing the “top of the funnel” costs. If a manufacturer can find a new raw material supplier that reduces the cost per unit from $10.00 to $8.50, they have achieved a 15% reduction in COGS. While $1.50 might seem small, a 15% reduction in costs can lead to a 50% or even 100% increase in net profit margins, depending on the business’s existing overhead.

Benchmarking Overhead and Operating Expenses

Operational efficiency is frequently measured by comparing current spending against historical benchmarks using percent reduction. Companies often set “efficiency targets,” such as a 5% year-over-year reduction in energy consumption or a 10% reduction in administrative waste. These targets are easier to communicate to department heads as percentages rather than raw dollar amounts, as they scale according to the size of the department’s budget.

Identifying Revenue Churn and Customer Loss

Not all reductions are positive. In subscription-based business models (SaaS), calculating the percent reduction in the customer base—known as churn—is the single most important metric for long-term viability. If a company starts the month with 1,000 subscribers and ends with 950 (excluding new sign-ups), they have a 5% churn rate. Analyzing why this reduction is occurring and implementing strategies to lower that percentage is the key to achieving exponential growth.

Advanced Financial Tools and Strategy

While the math can be done on a napkin, modern finance relies on digital tools to track and visualize these reductions over time.

Leveraging Spreadsheets for Automated Tracking

For personal finance enthusiasts and business analysts alike, Excel and Google Sheets are the standard tools for calculating percent reduction. Using the formula = (B2 - C2) / B2 (where B2 is the original value and C2 is the new value) and formatting the cell as a percentage allows for real-time tracking of financial goals. Automated dashboards can highlight cells in red or green based on whether a reduction is favorable (like an expense) or unfavorable (like a revenue dip).

The Psychology of Percentages in Wealth Building

There is a significant psychological component to how we perceive percentages. In behavioral finance, the “unit effect” suggests that people are often more motivated by seeing a “20% reduction in debt” than “a $2,000 reduction in debt.” Percentages provide a sense of completion and a clear trajectory toward zero (for debt) or toward a target efficiency goal.

By consistently applying the percent reduction formula to your financial life, you move away from reactive money management and toward a proactive, analytical approach. You begin to see your finances as a series of levers that can be adjusted. Whether you are cutting the “fat” from a corporate budget or recovering from a market dip, the percent reduction calculation is your primary compass for navigating the complexities of the financial world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.