In the current economic landscape, the ability to accept credit card payments is no longer a luxury for businesses; it is a fundamental requirement for survival and growth. Whether you are launching a side hustle, scaling an e-commerce platform, or managing a traditional brick-and-mortar storefront, your financial infrastructure dictates your capacity for revenue generation. Moving beyond the simple act of “swiping a card,” understanding the mechanics of payment processing allows a business owner to optimize cash flow, minimize overhead costs, and protect their bottom line. This guide explores the financial landscape of credit card acceptance, focusing on the tools and strategies that drive business finance.

Understanding the Financial Infrastructure of Payment Processing

Before a single dollar reaches your business bank account, it travels through a complex web of financial institutions. Navigating this infrastructure is the first step in choosing a system that aligns with your financial goals. There are two primary avenues for accepting payments: Merchant Accounts and Payment Service Providers (PSPs).

Merchant Accounts vs. Payment Service Providers (PSPs)

A merchant account is a dedicated business bank account that allows you to accept credit and debit card payments. When you have a dedicated merchant account, you are assigned your own merchant ID (MID), which offers greater stability and often lower transaction fees for high-volume businesses. However, the underwriting process for these accounts is rigorous, involving credit checks and financial history audits.

Conversely, Payment Service Providers (PSPs), such as Square, Stripe, or PayPal, aggregate thousands of small businesses under a single “master” merchant account. This model is ideal for new entrepreneurs and small businesses because it offers near-instant approval and a simplified fee structure. While PSPs provide convenience, they lack the personalized financial underwriting of a dedicated account, which can sometimes lead to sudden account freezes if the provider detects unusual transaction patterns.

The Role of the Acquiring Bank and Issuing Bank

Every transaction is a digital dialogue between the acquiring bank (your bank) and the issuing bank (the customer’s bank). When a customer presents a card, your payment processor requests authorization from the issuing bank. The issuing bank checks for available funds and fraud markers before sending an approval code back through the network. Understanding this flow is vital because each entity in the chain takes a small percentage of the transaction. For a business owner, the goal is to work with an acquiring partner that offers the most efficient path for these funds to settle into your operational account.

Analyzing the Costs: Fee Structures and Revenue Impact

The most critical aspect of accepting credit cards from a financial management perspective is the cost. Merchant fees can significantly erode profit margins if they are not properly audited and understood. Most processors use one of two primary pricing models.

Interchange-Plus vs. Flat-Rate Pricing

Interchange-plus pricing is widely considered the most transparent and cost-effective model for growing businesses. In this scenario, you pay the “interchange” rate—which is the wholesale cost set by card networks like Visa and Mastercard—plus a small, fixed markup from your processor. Because interchange rates vary depending on the type of card (e.g., a basic debit card vs. a high-end rewards credit card), this model ensures you only pay the true cost of each specific transaction.

Flat-rate pricing, on the other hand, charges a consistent percentage for every transaction (e.g., 2.9% + $0.30), regardless of the card type. While this provides predictable costs and simplifies bookkeeping, it is often more expensive for the merchant in the long run. The “spread” between the actual interchange cost and the flat rate is kept by the processor as profit. For businesses with high transaction volumes, switching from flat-rate to interchange-plus pricing can save thousands of dollars annually.

Identifying Hidden Costs and Ancillary Fees

Beyond the per-transaction percentage, business owners must account for various “hidden” fees that can affect their monthly financial statements. These may include:

- PCI Compliance Fees: Charged to ensure your business meets security standards.

- Statement Fees: Monthly charges for the preparation of financial reports.

- Gateway Fees: Costs associated with the software that connects your online store to the payment network.

- Minimum Processing Fees: A charge applied if your monthly transaction volume falls below a certain threshold.

To maintain a healthy financial outlook, it is essential to request a full fee schedule from any prospective processor and negotiate the removal of “junk fees” that do not provide direct value to your operations.

Choosing the Right Financial Tools for Your Business Model

The tools you use to accept payments should be viewed as financial assets. The right software and hardware can automate your accounting, manage your inventory, and provide data-driven insights into your revenue trends.

Solutions for E-commerce and Online Side Hustles

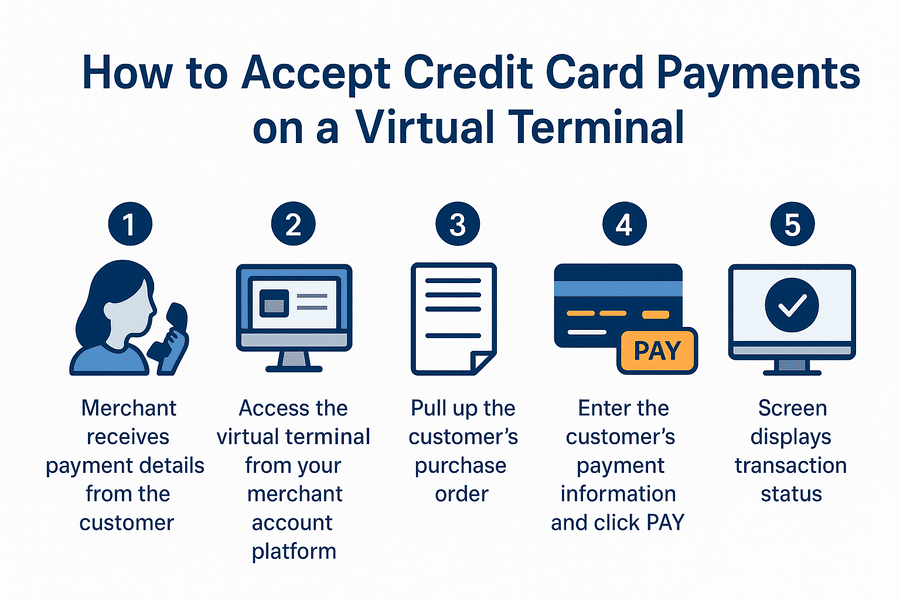

For digital businesses, the payment gateway is the heart of the operation. Modern gateways are designed to integrate seamlessly with shopping carts and website builders. Tools like Stripe have become the industry standard for online income because of their robust reporting features and ability to handle recurring subscriptions. From a financial management standpoint, these tools allow for automated tax calculations and multi-currency support, which are essential for businesses looking to scale internationally without increasing their administrative burden.

Point-of-Sale (POS) Systems for Physical Retail

In a physical retail environment, the Point-of-Sale (POS) system does more than just process cards; it acts as a central hub for business finance. Advanced systems like Clover or Toast integrate payment processing with inventory management and labor cost tracking. By syncing your sales data directly with your inventory, you can identify which products have the highest profit margins and which are “dead stock,” allowing for better capital allocation.

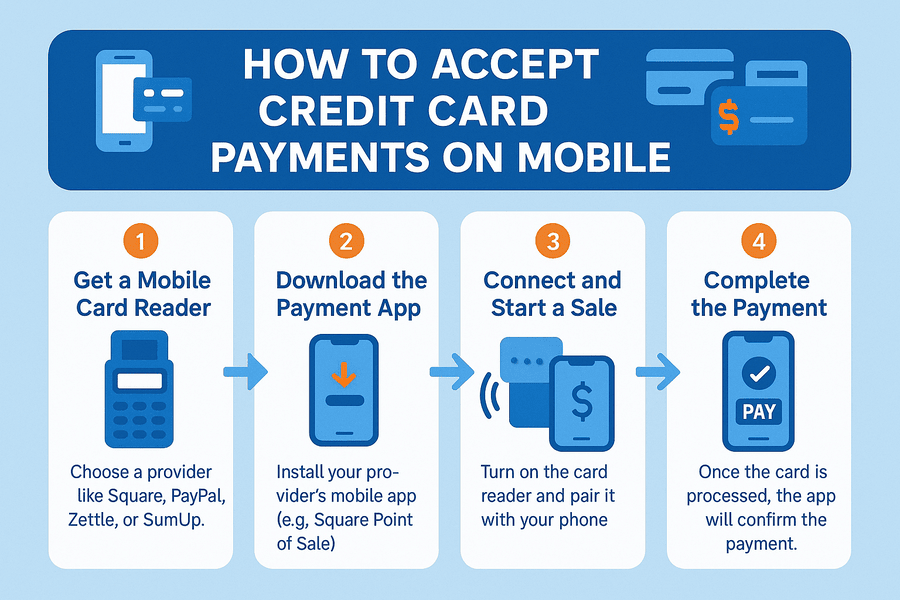

Mobile Payments and Invoicing Tools

For service-based businesses, such as consultants, contractors, or freelancers, mobile payment tools and digital invoicing are paramount. Accepting credit cards via a mobile app or a secure digital link sent through an invoice can dramatically reduce the “Days Sales Outstanding” (DSO). Instead of waiting for a check to arrive in the mail and clear the bank, businesses can receive funds within 24 to 48 hours, significantly improving short-term liquidity.

Risk Management and Protecting Your Bottom Line

Accepting credit cards introduces financial risks that must be managed with the same rigor as any other business liability. The two greatest threats to your processing revenue are chargebacks and fraudulent transactions.

Chargebacks: The Cost of Disputed Transactions

A chargeback occurs when a customer disputes a transaction directly with their bank rather than seeking a refund from the merchant. For the business owner, this is a double financial blow: the original sale amount is clawed back from your account, and you are hit with a chargeback fee (ranging from $15 to $100). Furthermore, if your chargeback ratio exceeds 1% of your total transactions, you risk being placed in a “high-risk” category by the card networks, which leads to higher fees or even the termination of your merchant account. Implementing clear refund policies and using delivery confirmation are essential financial safeguards.

Fraud Prevention as a Financial Strategy

Fraudulent transactions are not just a security issue; they are a direct loss of inventory and capital. Utilizing Address Verification Service (AVS) and Card Verification Value (CVV) checks are the bare minimum for online transactions. More advanced financial tools use AI-driven risk scoring to flag suspicious orders before they are processed. By investing in robust fraud prevention, you protect your cash flow and ensure that your revenue represents actual, settled sales rather than temporary entries that might be reversed later.

Optimizing Cash Flow and Settlement Cycles

The final stage of accepting credit card payments is the settlement—the moment the funds are actually deposited into your business bank account. Understanding this cycle is critical for managing payroll, rent, and inventory purchases.

Navigating Payout Timelines

Standard settlement cycles typically range from T+1 to T+3 (transaction day plus one to three business days). However, some processors now offer “Instant Deposit” for a small additional fee. While the convenience of instant funds is tempting, a savvy financial manager will weigh the cost of that convenience against the business’s actual liquidity needs. In most cases, establishing a reliable T+1 cycle is sufficient for maintaining operational cash flow without incurring unnecessary “speed” fees.

Integrating Payments with Accounting Software

To achieve true financial efficiency, your payment processing system should “talk” to your accounting software (e.g., QuickBooks, Xero, or FreshBooks). Manual data entry is not only time-consuming but prone to errors that can complicate tax filings and financial audits. By automating the reconciliation process, you ensure that every credit card transaction is accurately recorded, categorized, and reconciled against your bank statements in real-time. This level of integration provides a clear, up-to-the-minute view of your business’s financial health, empowering you to make informed decisions about future investments and growth strategies.

In conclusion, accepting credit card payments is a multi-faceted financial operation. By understanding the infrastructure, scrutinizing the fee structures, choosing the right tools, and managing risk, you transform payment processing from a simple business expense into a strategic advantage that fuels long-term financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.