The year 1929 stands as a stark reminder in financial history, marking the devastating stock market crash that precipitated the Great Depression. Far from being a sudden, isolated event, the crash was the culmination of years of speculative excess, underlying economic vulnerabilities, and a fragile financial system. Understanding the intricate tapestry of factors that led to this cataclysmic event offers invaluable lessons for modern investors, policymakers, and anyone interested in the dynamics of market booms and busts. This deep dive into the 1929 crash will unravel its origins, the mechanisms of its downfall, its profound aftermath, and the enduring financial wisdom it imparts.

The Roaring Twenties: A Precursor to Collapse

The decade preceding the crash, famously known as the “Roaring Twenties,” was characterized by unprecedented economic growth, technological innovation, and a vibrant cultural shift. Post-World War I prosperity fueled an era of widespread optimism, leading many to believe that the economic boom was perpetual. This period, however, simultaneously sowed the seeds of future financial instability.

Unbridled Optimism and Speculation

The economic boom of the 1920s fostered an environment of immense confidence. New industries like automobiles, radio, and aviation captured the public imagination and drove significant investment. Corporate profits soared, and the stock market seemed to offer a guaranteed path to wealth. This widespread optimism, while seemingly benign, gradually morphed into irrational exuberance, divorcing stock prices from their underlying fundamental values. People increasingly bought stocks not for their long-term value or dividend potential, but in the expectation that they could sell them quickly to someone else at an even higher price.

The Allure of Easy Money

The perception of an ever-rising market attracted millions of new investors, many of whom had little to no prior experience with financial markets. The accessibility of credit further fueled this speculative fervor. Banks and brokers were eager to lend money for stock purchases, creating a feedback loop where rising stock prices encouraged more borrowing, which in turn pushed prices even higher. The promise of “easy money” became a powerful siren song, luring individuals from all walks of life into the speculative frenzy.

Economic Bubbles and Overproduction

While certain sectors thrived, the overall economic picture was more complex. There were signs of overproduction in several industries, particularly agriculture. Farmers, who had expanded production during World War I to feed Europe, found themselves facing falling prices and surplus goods in the post-war era. This agricultural distress, coupled with increasing income inequality, meant that while some segments of society prospered, a significant portion struggled, dampening overall consumer demand and creating an unstable foundation beneath the booming stock market. The asset bubble in stocks was thus growing in an environment where not all sectors of the real economy were as robust as the market suggested.

The Mechanisms of the Crash: Black Thursday and Black Tuesday

The stock market’s ascent began to falter in the late summer and early autumn of 1929. Initial tremors gave way to outright panic, culminating in two of the most infamous days in financial history.

Margin Buying: Fueling the Fire

A critical mechanism amplifying the crash was the widespread practice of “buying on margin.” This allowed investors to purchase stocks by paying only a small percentage of the stock’s price (often as little as 10-20%) and borrowing the rest from their broker. As long as stock prices rose, this strategy magnified returns. However, the reverse was also true: even a small drop in price could wipe out an investor’s equity and trigger a “margin call” – a demand from the broker for immediate payment of the loan. If the investor couldn’t meet the margin call, their stocks would be sold, irrespective of market conditions, to cover the debt. This mechanism created an extremely fragile market highly susceptible to rapid, cascading sell-offs.

The Initial Tremors: September and October 1929

The market reached its peak on September 3, 1929, after which it began a gradual, albeit choppy, decline. Concerns about overvaluation and the sustainability of the boom started to surface. On October 24, 1929, known as “Black Thursday,” the market experienced its first major collapse. Trading volume was unprecedented, with nearly 13 million shares exchanged as panic selling gripped investors. Major industrial stocks plummeted, and the tickers struggled to keep up with the deluge of transactions.

Failed Interventions and Continued Panic

In an attempt to stem the bleeding on Black Thursday, a consortium of leading bankers, including figures like Richard Whitney of the New York Stock Exchange, pooled resources to buy large blocks of blue-chip stocks at above-market prices. This coordinated effort provided a temporary reprieve, stabilizing the market by the end of the day and even leading to a modest recovery on Friday and Saturday. However, this intervention proved insufficient to counteract the underlying fear and selling pressure that had taken root. The psychological damage was done, and confidence had evaporated.

Black Tuesday: The Final Plunge

The brief respite was shattered on Monday, October 28, as the market continued its slide. The true nadir arrived on Tuesday, October 29, 1929 – “Black Tuesday.” The selling frenzy escalated dramatically, surpassing Black Thursday’s record. A staggering 16.4 million shares were traded, and the Dow Jones Industrial Average fell by an astonishing 12%. This day marked the complete capitulation of investor confidence, as virtually everyone who could sell, did. The market’s plunge was relentless, and there was no effective mechanism to halt the freefall. Fortunes were wiped out in hours, and the dreams of easy wealth turned into nightmares of insurmountable debt.

Underlying Economic Weaknesses and Contributing Factors

While the stock market crash was the immediate catalyst for widespread financial ruin, several fundamental weaknesses in the American and global economies had been festering for years, making the system uniquely vulnerable.

Unequal Distribution of Wealth

The prosperity of the Roaring Twenties was not evenly distributed. A significant portion of the nation’s wealth was concentrated in the hands of a small percentage of the population. This meant that the vast majority of Americans had limited purchasing power, preventing robust consumer demand that could sustain economic growth. When the affluent stopped investing or lost their fortunes, there was little broader consumer base to cushion the blow.

Agricultural Distress

As mentioned, the agricultural sector had been in a depression for much of the 1920s. Overproduction and declining global demand led to plummeting crop prices, leaving farmers heavily indebted and unable to purchase industrial goods. This significant segment of the population was already in financial crisis long before the stock market crash, further undermining the nation’s economic stability.

Fragile Banking System

The banking system of the 1920s was decentralized and largely unregulated. Thousands of small, independent banks operated without federal deposit insurance. Many of these banks had heavily invested in the stock market or lent money to speculators, making them highly susceptible to market fluctuations. When the crash hit, panic-stricken depositors rushed to withdraw their funds, leading to a wave of bank runs and failures. These failures not only wiped out savings but also constricted the credit supply, exacerbating the economic downturn.

International Economic Instability

The global economy was also intertwined with America’s fate. The system of war debts and reparations following World War I created a precarious financial cycle. Germany struggled to pay reparations to Allied powers, who in turn relied on these payments to repay war loans to the United States. American loans to Germany were essential to keep this cycle going. When the U.S. financial system faltered, American lending dried up, disrupting the entire international financial framework and transmitting the crisis worldwide.

Lack of Regulatory Oversight

The era preceding the crash was marked by minimal government regulation of financial markets. There were no robust mechanisms to prevent manipulative practices, control margin lending, or ensure transparency. The Federal Reserve, still a relatively young institution, failed to effectively rein in speculative lending or act decisively to stabilize the banking system in the crisis’s early stages. This hands-off approach allowed the speculative bubble to inflate unchecked and left the financial system without adequate shock absorbers when the inevitable correction arrived.

The Immediate Aftermath and Long-Term Repercussions

The impact of the 1929 stock market crash extended far beyond Wall Street, triggering a cascade of economic and social crises that reshaped American society and global financial governance.

Widespread Financial Ruin and Bank Runs

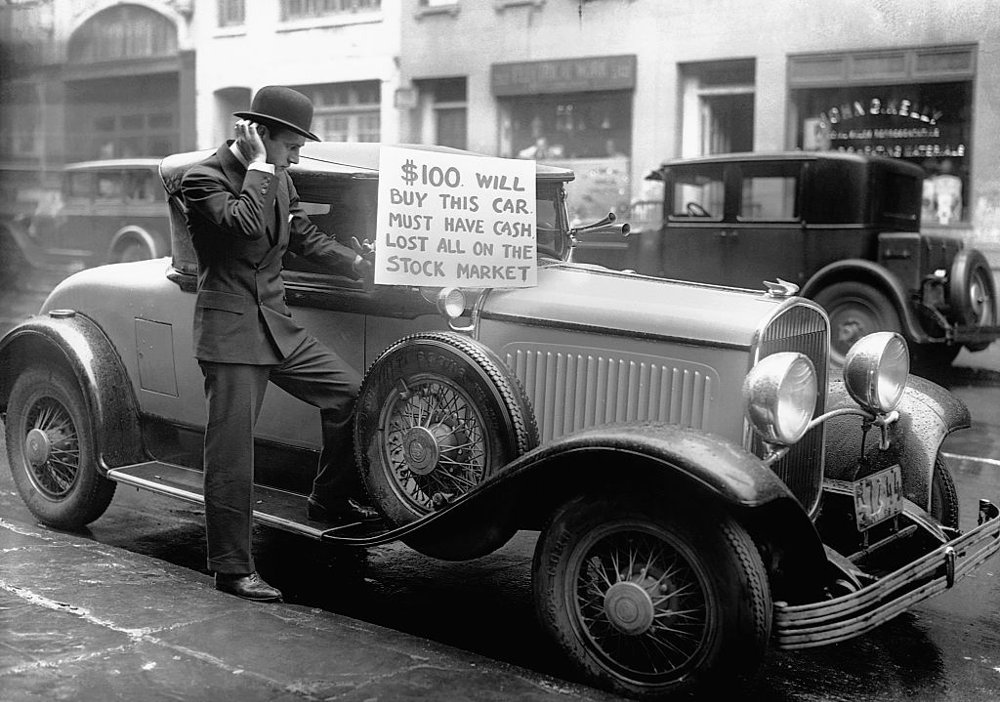

The immediate aftermath saw millions of investors, from seasoned financiers to ordinary citizens, lose their life savings. The phenomenon of margin calls bankrupted countless individuals and families. As the value of bank assets (often investments in stocks or loans to brokers) plummeted, and public confidence eroded, a wave of bank runs began. People rushed to withdraw their deposits, leading to mass bank failures. In the absence of federal deposit insurance, these failures wiped out the savings of millions more, deepening the economic despair. Businesses faced a severe credit crunch, leading to bankruptcies and widespread unemployment.

The Onset of the Great Depression

While economists still debate whether the crash was the sole cause or merely the trigger, there is no doubt it ushered in the Great Depression. The destruction of wealth, loss of consumer confidence, banking collapse, and subsequent credit contraction paralyzed the economy. Consumer spending plummeted, businesses cut production, and unemployment soared, eventually reaching an estimated 25% of the workforce. The Great Depression became a decade-long economic catastrophe, with profound social and political consequences both domestically and internationally.

Regulatory Reforms: Lessons Learned

The scale of the disaster spurred significant government intervention and regulatory reforms aimed at preventing a recurrence. The New Deal era introduced landmark legislation:

- Securities Act of 1933 and Securities Exchange Act of 1934: These established the Securities and Exchange Commission (SEC) to regulate stock exchanges, combat fraud, and ensure transparency in financial markets.

- Glass-Steagall Act (Banking Act of 1933): This separated commercial and investment banking (though later repealed) and, crucially, established the Federal Deposit Insurance Corporation (FDIC) to insure bank deposits, restoring public confidence in the banking system.

- Federal Reserve Reforms: The Fed’s role in managing monetary policy and acting as a lender of last resort was clarified and strengthened over time.

These reforms fundamentally reshaped the financial landscape, creating a more regulated and robust system.

Enduring Lessons for Modern Investors

The 1929 stock market crash remains a crucial case study, offering timeless lessons that are highly relevant for today’s investors in the “Money” sphere.

The Dangers of Speculative Bubbles

The crash vividly illustrates the perils of asset bubbles, where prices detach from underlying value driven by speculative enthusiasm and the “fear of missing out.” Modern markets, too, can experience bubbles (e.g., dot-com bubble, housing bubble). Investors must exercise discipline, conduct thorough due diligence, and resist the temptation to chase irrational gains based on hype rather than fundamentals.

Importance of Diversification and Risk Management

The concentrated portfolios and highly leveraged positions common in 1929 amplified losses dramatically. Today, the principles of diversification across different asset classes, industries, and geographies are paramount. Risk management strategies, including setting stop-losses, understanding one’s risk tolerance, and avoiding excessive leverage (margin), are essential safeguards against catastrophic losses.

The Role of Regulation in Market Stability

The regulatory framework that emerged from the 1929 crash highlights the critical role of government oversight in maintaining market integrity and stability. While regulation is often debated, its purpose is to protect investors, ensure fair markets, and prevent systemic risks that could undermine the entire financial system. Understanding regulatory changes and their implications is vital for investors.

Understanding Market Psychology

The 1929 crash was as much a psychological event as an economic one. Fear and greed are powerful forces that can drive markets to extremes. Investors who can recognize and manage their own emotions, avoiding panic selling during downturns and resisting euphoric exuberance during upturns, are better positioned for long-term success. The ability to think independently and avoid herd mentality is a timeless virtue in investing.

The 1929 stock market crash was a watershed moment that forever altered the landscape of finance and economics. By studying its causes and consequences, modern investors can glean invaluable insights into market dynamics, the importance of prudence, the role of regulation, and the enduring power of human psychology in financial decision-making. These lessons serve as a perpetual reminder that while markets can offer immense opportunities for wealth creation, they also harbor significant risks that demand respect and informed navigation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.