Today, the financial markets concluded a session marked by a complex interplay of macroeconomic data, corporate developments, and shifting investor sentiment. Understanding the closing bell’s implications requires a deep dive into the various forces that shaped the day’s trajectory, offering crucial insights for both short-term traders and long-term investors. From major indices to specific sectors, and from domestic economic reports to global geopolitical currents, the market’s performance is a tapestry woven from countless threads, each contributing to the final picture.

A Day of Volatility and Key Economic Indicators

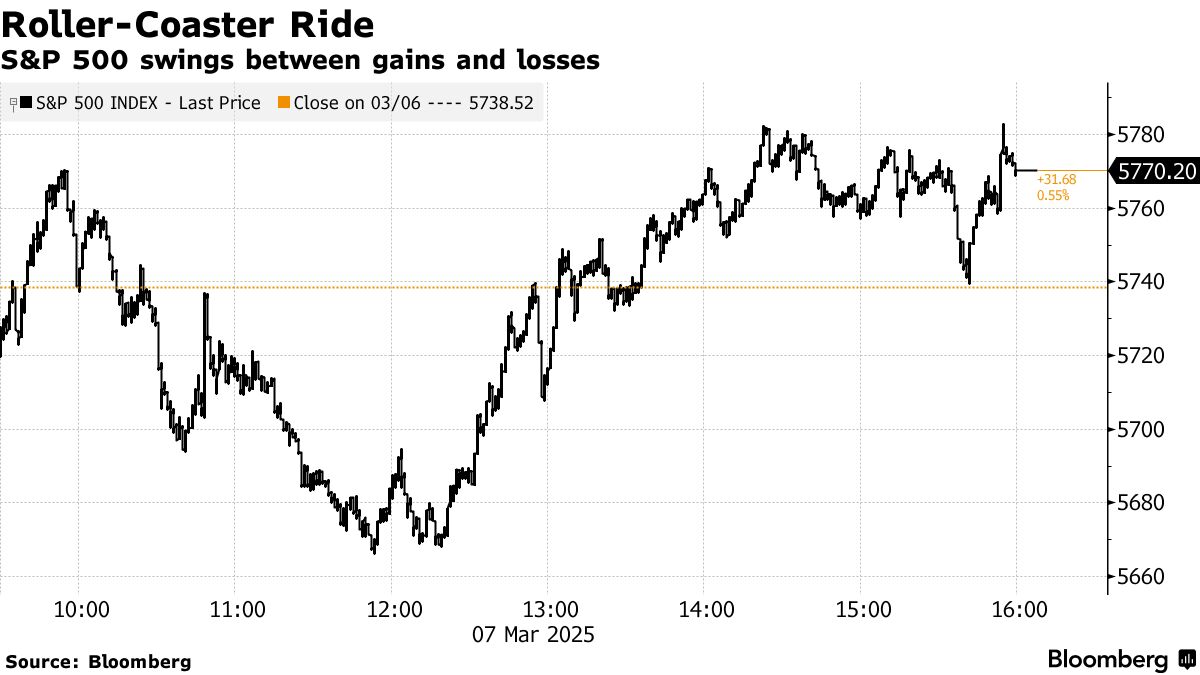

The closing numbers today reflected a dynamic session where early gains were tempered by mid-day profit-taking, only to see a late surge in specific segments. This pattern is often indicative of underlying uncertainty coupled with targeted buying opportunities. The overall market sentiment fluctuated significantly, influenced heavily by a series of economic reports released throughout the morning.

Major Indices Performance

The S&P 500, widely considered the broadest gauge of U.S. equities, experienced a modest uptick, ending the day marginally higher. This upward movement was primarily driven by strength in defensive sectors and a late-session rally in mega-cap technology stocks. While positive, the index struggled to break above a key resistance level, suggesting that while bullish sentiment exists, it remains cautious.

The Dow Jones Industrial Average, representing 30 large, publicly owned companies based in the United States, showed slightly more resilience, closing firmly in positive territory. Industrial and financial components within the Dow exhibited particular strength, benefiting from optimistic forecasts regarding infrastructure spending and interest rate expectations. This performance suggests a segment of the market is betting on a traditional economic recovery, supported by robust corporate earnings in specific sectors.

In contrast, the Nasdaq Composite, heavily weighted towards technology and growth stocks, saw more pronounced swings. After an initial dip, the index staged a strong comeback, closing with significant gains. This resurgence was fueled by renewed interest in high-growth tech companies, particularly those in the artificial intelligence and cloud computing spaces, following a period of consolidation. The volatility in Nasdaq underscores the ongoing debate between value and growth investing in the current economic climate, with growth stocks demonstrating their capacity for rapid recovery despite broader market pressures. Overall, the mixed performance across these major indices paints a picture of a market grappling with diverse pressures and opportunities.

The Influence of Macroeconomic Data

A significant driver of today’s market action was the release of several key macroeconomic reports. The morning began with the publication of the latest Consumer Price Index (CPI) figures, which showed inflation remaining elevated but with some signs of moderating in certain categories. This report had an immediate impact, causing initial apprehension as investors weighed the implications for future monetary policy. A higher-than-expected inflation print would typically signal a more aggressive stance from the central bank, potentially leading to higher interest rates and a drag on corporate profitability.

Following the inflation data, a new jobs report indicated a robust labor market, with unemployment figures continuing to trend downwards and wage growth showing a steady increase. While positive for the broader economy, a strong labor market can sometimes be a double-edged sword for financial markets, as it can contribute to inflationary pressures and prompt central banks to maintain hawkish policies. The market digested these conflicting signals throughout the day, leading to the aforementioned volatility. Investors are constantly trying to decipher the Federal Reserve’s next move, and these data points provide crucial, albeit sometimes confusing, clues. The balancing act between economic growth and inflation control remains a central theme guiding market sentiment.

Sectoral Shifts and Corporate Earnings Insights

Beyond the broad market indices, a deeper look into individual sectors reveals the nuanced dynamics that characterized today’s trading. Different industries reacted distinctly to economic news and company-specific announcements, leading to clear winners and losers by the closing bell. Understanding these sectoral shifts is critical for investors looking to optimize their portfolios.

Leading and Lagging Sectors

Today, the Technology sector, particularly sub-segments focused on cloud infrastructure and semiconductors, demonstrated remarkable resilience and finished strong. This was largely driven by continued enthusiasm for artificial intelligence advancements and robust demand for digital transformation solutions. Large-cap tech giants, with their strong balance sheets and diversified revenue streams, acted as anchors, pulling the broader technology index higher despite earlier concerns about valuation.

Conversely, the Energy sector experienced a more subdued day. While crude oil prices saw minor fluctuations, geopolitical developments provided mixed signals, preventing a significant rally. Investors in energy stocks often look to global supply-demand dynamics and geopolitical stability, and today’s environment offered little fresh impetus for substantial upward movement, leading to a largely flat close for the sector.

The Healthcare sector, often considered defensive, displayed consistent strength throughout the day. Pharmaceutical companies and medical device manufacturers, in particular, benefited from positive clinical trial news and robust earnings outlooks. The inherent stability of healthcare demand, irrespective of broader economic cycles, made it an attractive safe haven for some investors amidst the day’s volatility. This steady performance underscores the sector’s role in providing portfolio stability during uncertain times.

Meanwhile, the Real Estate sector faced headwinds, concluding the day in negative territory. Concerns over rising interest rates, which directly impact borrowing costs for developers and homebuyers, weighed heavily on real estate investment trusts (REITs) and related companies. While specific segments like data centers showed some resilience, the broader sentiment in real estate remained cautious, reflecting fears of a potential slowdown in property markets should financing costs continue to climb. This divergence highlights how different sectors react uniquely to the same macroeconomic pressures, emphasizing the importance of diversified portfolios.

Impact of Recent Earnings Reports

A handful of significant corporate earnings reports released either yesterday after the close or this morning had a palpable effect on today’s market. One major technology firm reported stronger-than-expected revenue growth and an optimistic outlook for its cloud computing division, sending its stock soaring and providing a halo effect for other companies in the software and services space. This positive surprise helped to alleviate some of the earlier concerns about overvaluation in tech.

Conversely, a prominent consumer discretionary company issued a cautious outlook, citing persistent supply chain disruptions and softening consumer demand in certain product lines. This led to a sharp sell-off in its shares and dragged down other retailers and consumer brands, signaling potential headwinds for the broader consumer sector as inflation continues to impact purchasing power. These specific earnings reports serve as micro-level indicators, often providing early insights into macro-level trends and influencing investor decisions across entire industries. The market often takes its cues from these bellwether companies, adjusting expectations and valuations accordingly.

Global Cues and Geopolitical Undercurrents

While domestic factors played a dominant role, today’s market performance was also subtly influenced by developments on the international stage. Global markets are increasingly interconnected, and events in one region can ripple across continents, impacting commodity prices, currency valuations, and investor confidence worldwide.

International Market Performance

European markets generally closed mixed, with some indices showing minor gains driven by positive industrial production data, while others lagged due to ongoing concerns about energy security and inflationary pressures. Asian markets, having closed before U.S. trading commenced, had mostly ended higher, buoyed by signals of potential stimulus measures in major economies. This positive handover from Asia provided some initial optimism for U.S. traders. However, later in the day, news from emerging markets regarding currency depreciation and capital outflows introduced a degree of caution, reminding investors of the fragilities in global finance. The varying performances across different geographies highlight the localized impacts of global economic trends, as each region contends with its unique set of challenges and opportunities.

Commodity Prices and Currency Movements

Commodity markets presented a mixed picture today. Crude oil prices, after an initial dip, stabilized and ended slightly higher. This was a response to geopolitical tensions in a key producing region, which overshadowed concerns about global demand slowdowns. The price of natural gas, however, saw a more significant increase, driven by colder weather forecasts and inventory reports.

Gold, often seen as a safe-haven asset, experienced moderate buying interest throughout the day. This upward movement in gold prices suggests that despite some overall market gains, a segment of investors remains wary of broader economic uncertainties and potential future inflation.

In the foreign exchange market, the U.S. dollar strengthened against a basket of major currencies. This dollar appreciation was partly attributable to the relatively stronger U.S. economic data released today, reinforcing the perception of the dollar as a stable asset. A stronger dollar can have mixed implications for the U.S. market; while it makes imports cheaper, it can also make U.S. exports more expensive, potentially impacting the earnings of multinational corporations. The interplay of these global factors, from commodity prices to currency valuations, often provides an underlying current that influences daily market dynamics, even if not immediately apparent in headline figures.

What This Means for the Prudent Investor

Today’s market activity underscores the perennial importance of a disciplined, long-term investment strategy. Daily fluctuations, while captivating, are often noise when viewed through the lens of sustained wealth creation. For the prudent investor, today’s close offers several key takeaways that should inform, rather than dictate, portfolio decisions.

Rebalancing and Risk Assessment

A day like today, characterized by sectoral divergence and shifting sentiment, serves as an opportune moment for investors to review their portfolio’s asset allocation. If certain sectors, like technology, have seen significant gains, they might now represent a larger proportion of the portfolio than initially intended. This could necessitate a rebalancing act to bring the portfolio back in line with the investor’s target asset allocation and risk tolerance. Rebalancing isn’t about chasing daily winners or panic selling losers; it’s about systematically managing risk and ensuring the portfolio remains diversified across various asset classes and industries. For instance, if the recent rally in growth stocks has overweight a portfolio in that area, an investor might consider trimming some of those positions and reallocating to value stocks or defensive sectors like healthcare, which showed resilience today. This proactive approach helps to lock in gains and mitigate potential future downside risks.

Furthermore, investors should reassess their exposure to specific risks. If global geopolitical tensions are escalating, is the portfolio overly concentrated in regions or companies particularly vulnerable to such events? If inflation remains sticky, are there sufficient inflation hedges in place, such as real assets or inflation-protected securities? Regularly questioning these exposures ensures the portfolio is robust enough to withstand various market environments, rather than being overly reliant on a single positive outcome or vulnerable to a specific negative event.

Long-Term Strategy vs. Daily Fluctuations

The most crucial lesson from any single market day is to maintain a long-term perspective. The urge to react to every headline, every percentage point swing, can be detrimental to an investor’s financial goals. Today’s market close, whether up or down, represents just one data point in a much larger economic cycle. For those with investment horizons stretching over years or decades, short-term market movements are primarily distractions.

Instead of focusing on today’s closing numbers as a verdict, investors should consider them as feedback. This feedback should be used to validate or adjust their understanding of underlying economic trends, corporate fundamentals, and geopolitical risks, rather than prompting impulsive trades. Maintaining a diversified portfolio, regularly contributing to investment accounts, and sticking to a well-defined financial plan are far more impactful than attempting to time the market. The power of compounding, coupled with a consistent investment approach, significantly outweighs the fleeting gains or losses from daily market gyrations. By focusing on quality assets and a strategic allocation, investors can filter out the daily noise and concentrate on achieving their enduring financial objectives.

Looking Ahead: Anticipated Catalysts

As the market closes today, participants are already setting their sights on upcoming events and data releases that could shape tomorrow’s trading and influence broader market trends in the coming weeks. Anticipating these catalysts is a critical component of informed investing, allowing for proactive adjustments and strategic positioning.

Upcoming Economic Reports

The immediate focus will shift to several key economic reports scheduled for release in the coming days. These include the latest manufacturing Purchasing Managers’ Index (PMI) data, which provides a snapshot of the health of the industrial sector, and new housing starts figures, offering insights into the construction and real estate markets. Any significant deviation from analyst expectations in these reports could trigger substantial market reactions, either affirming current trends or signaling a shift in economic momentum. Furthermore, another round of inflation data, specifically focusing on producer prices, will be closely watched for any indications of easing cost pressures further down the supply chain. These economic indicators act as a continuous feedback loop, providing essential context for market participants to gauge the pace and direction of economic growth.

Central Bank Policies

Perhaps the most influential catalyst on the horizon is the upcoming meeting of the central bank. While no immediate rate decision is expected, the accompanying statements and press conference will be scrutinized for clues regarding the future trajectory of monetary policy. Any hints about quantitative tightening, interest rate hikes, or changes in economic forecasts could send ripples through equity, bond, and currency markets. Investors will be keen to understand the central bank’s interpretation of recent inflation and employment data, and how that might translate into policy actions. The balancing act between controlling inflation and supporting economic growth remains precarious, and the central bank’s guidance will be paramount in shaping market expectations for the months ahead, underscoring the ongoing influence of monetary policy on asset valuations and investor sentiment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.