In an increasingly interconnected and fast-paced world, the need for immediate money transfers has become more critical than ever. Whether it’s an urgent family matter, splitting a dinner bill with friends, paying a freelancer, or sending aid across borders, the ability to move funds swiftly and securely is no longer a luxury but a fundamental expectation. The days of waiting for checks to clear or relying solely on slow bank transfers are largely behind us, as a plethora of innovative financial tools and services have emerged to facilitate instant monetary exchanges.

However, the sheer volume of options can be overwhelming, each with its own advantages, disadvantages, fee structures, and limitations. Understanding these nuances is crucial to making an informed decision that balances speed, cost, security, and convenience for both the sender and the recipient. This guide delves into the various avenues available for sending money immediately, empowering you to choose the most suitable method for your specific needs.

The Imperative for Instant Transfers in Modern Finance

The shift towards instant financial transactions reflects broader trends in digital transformation and consumer expectations. Our lives are often unpredictable, and financial emergencies or spontaneous needs can arise at any moment, demanding an equally spontaneous financial response.

The Evolving Landscape of Personal Transactions

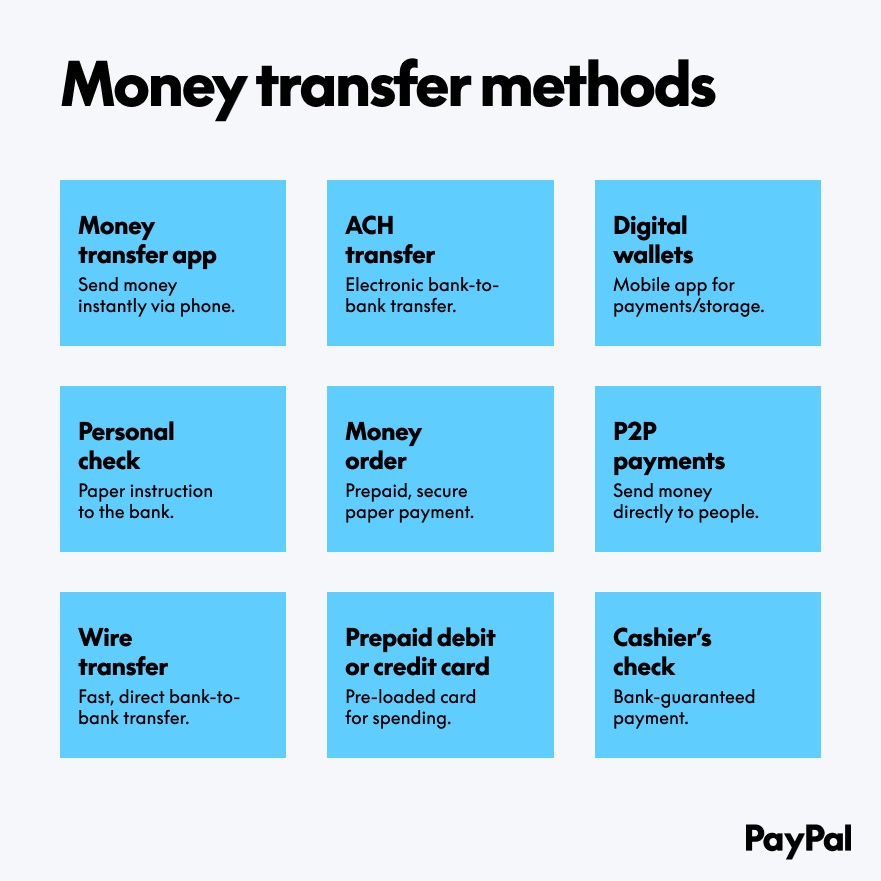

For decades, traditional banking systems, while robust and secure, were designed with inherent processing times. Automated Clearing House (ACH) transfers, for instance, are widely used for direct deposits and bill payments but typically take 1-3 business days. Wire transfers offered faster same-day processing but came with higher costs and more cumbersome procedures. The advent of the internet and mobile technology, however, catalyzed a revolution in personal finance, introducing digital platforms that prioritize speed and user experience above all else. This evolution has democratized immediate transfers, making them accessible to a wider demographic through intuitive interfaces.

When Speed Matters Most: Emergency vs. Everyday Needs

The urgency of a money transfer can vary significantly. In emergency situations – such as a loved one stranded without cash, an unexpected medical bill, or a critical payment deadline – speed is paramount, often outweighing cost concerns. Here, services guaranteeing near-instant delivery are invaluable.

Conversely, for more routine immediate needs, like paying a babysitter, splitting dinner, or making a quick payment to a small business, convenience and low-to-no fees become key. While speed is still desired, a minute or two of delay for a free service is often acceptable. Understanding this distinction helps in selecting the appropriate tool; an expensive wire transfer might be overkill for a casual transaction, just as a P2P app might be insufficient for a large, critical international transfer.

Navigating the Digital Frontier: Instant Payment Applications

Digital payment apps have revolutionized how individuals send and receive money, making immediate transfers between peers incredibly simple and often free. These platforms leverage modern technology to bypass traditional banking delays, offering a user-friendly experience primarily through mobile devices.

Peer-to-Peer (P2P) Payment Apps: Zelle, Venmo, Cash App, PayPal

-

Zelle: Integrated directly into many US banking apps, Zelle allows users to send money from their bank account to another Zelle-enrolled bank account, typically within minutes. It’s often free for consumers as it operates within the existing banking infrastructure. The main advantage is its seamless integration with banking, eliminating the need for a separate app for many users. However, it’s primarily for domestic transfers within the US, and transaction limits are set by individual banks.

-

Venmo: Popular for its social features, Venmo allows users to send and receive money, share payments, and even make purchases. Transfers from a Venmo balance or linked bank account to another Venmo user are usually instant and free. However, if you want to transfer funds from your Venmo balance to your bank account immediately, there’s typically a small fee (e.g., 1.75%, minimum $0.25, maximum $25). Standard transfers to a bank account are free but take 1-3 business days.

-

Cash App: Similar to Venmo, Cash App offers instant peer-to-peer transfers, direct deposit, and even allows users to buy and sell Bitcoin and stocks. Sending money from a Cash App balance or linked debit card to another Cash App user is generally free and instant. Like Venmo, instant transfers from your Cash App balance to an external bank account incur a small fee (e.g., 0.5-1.75%).

-

PayPal: A veteran in the digital payment space, PayPal offers extensive capabilities, including domestic and international P2P transfers. Sending money to friends and family using a PayPal balance or linked bank account is free within the US. For instant transfers to a bank account, a fee applies (e.g., 1.75% for debit card transfers, up to $25). PayPal also supports a wider range of transactions, including payments for goods and services, which often carry fees. Its global reach makes it a versatile option for international P2P transactions, though currency conversion fees may apply.

Understanding Limits, Fees, and Security Features

While immensely convenient, P2P apps come with limitations. Transaction limits vary by service and verification level, which can be an issue for larger transfers. Instant payout options to external bank accounts almost always incur a small fee, which users must factor into their decision. Security is paramount; these apps employ encryption, fraud detection, and multi-factor authentication. However, since transactions are often irreversible, it’s crucial to double-check recipient details meticulously. Once sent, recovering funds from an incorrect recipient can be challenging, if not impossible.

Traditional Pathways Reimagined: Bank and Wire Transfers

While digital apps dominate the casual P2P space, traditional banking methods continue to evolve, offering robust solutions for immediate transfers, particularly for larger sums or when digital apps aren’t suitable.

Wire Transfers: The Gold Standard for Urgency (and Cost)

Wire transfers are perhaps the oldest method for near-instant bank-to-bank transfers. They are direct, real-time electronic transfers of funds from one bank to another, often within the same day, sometimes within hours. They are highly secure and, once initiated, are very difficult to reverse, making them suitable for time-sensitive, high-value transactions like real estate closings or international business payments.

The primary downsides are their cost, which can range from $25-$50 for domestic wires and more for international ones, and the process, which typically requires a visit to a bank branch or specific online banking permissions. For international wires, currency conversion fees also apply, and the recipient’s bank may charge a fee to receive the funds. Despite the cost, for guaranteed speed and security, especially across borders, wire transfers remain a reliable choice.

Expedited ACH and Real-Time Payments (RTP)

The traditional ACH network, while reliable, wasn’t built for speed. However, advancements have led to “same-day ACH” options in many countries, allowing funds to settle within the same business day for a small fee. This is faster than standard ACH but not truly “instant” like a wire or P2P app.

A more significant development is the rise of Real-Time Payments (RTP) networks. In the US, The Clearing House’s RTP network offers immediate, irrevocable, 24/7/365 interbank payments. This allows businesses and consumers to send and receive funds instantly, with immediate confirmation. As more banks and financial institutions connect to RTP, it is poised to become a standard for truly instant bank-to-bank transfers, bridging the gap between slow ACH and expensive wires, often at a lower cost than wires.

The Role of International Money Transfer Services (Wise, Remitly, Western Union)

For sending money across borders immediately, specialized international money transfer services often offer a more cost-effective and faster alternative to traditional bank wire transfers.

-

Wise (formerly TransferWise): Known for its transparent, low fees and use of the mid-market exchange rate, Wise enables fast international transfers. While some transfers can be instant, many arrive within hours or one business day, depending on the currencies and payout method. It’s ideal for bank-to-bank transfers.

-

Remitly: Focused on remittances, Remitly offers various speed options, including “Express” transfers that can be instant, typically using a debit card for funding. It supports bank deposits, mobile money, and cash pickup in many countries, often with competitive exchange rates and lower fees for slower transfers.

-

Western Union / MoneyGram: These services are renowned for their extensive global networks and cash pickup options, making them ideal when a recipient doesn’t have a bank account or needs physical cash immediately. Funds can often be available for pickup within minutes, though fees can be higher, especially for immediate services, and exchange rates may not always be the most competitive.

These services differentiate themselves by offering a range of funding and payout options (bank account, debit/credit card, mobile wallet, cash pickup) and varying speed tiers, allowing users to choose between immediate delivery at a higher cost or slower delivery at a lower fee.

Emerging Solutions and Critical Considerations for Immediate Transfers

As technology advances, new methods for immediate money transfers continue to emerge, alongside crucial factors to weigh before initiating any transaction.

Cryptocurrency and Blockchain: The Ultimate Instant (with Caveats)

Blockchain technology, underpinning cryptocurrencies like Bitcoin and Ethereum, offers the potential for near-instant, borderless transfers. However, volatility makes most cryptocurrencies unsuitable for everyday payments. Stablecoins, such as USDT or USDC, which are pegged to fiat currencies like the US dollar, offer the speed and low transaction costs of crypto without the price fluctuations. Sending stablecoins can be almost instantaneous (depending on network congestion) and cost fractions of a cent, regardless of the amount or distance.

The caveat here is complexity and accessibility. Both sender and recipient need a cryptocurrency wallet, and understanding how to acquire, send, and receive stablecoins requires a higher degree of technical literacy than using a P2P app or bank. Regulatory landscapes are also evolving, and convertibility back to fiat currency can add steps and costs. While offering unparalleled speed and low cost for large international transfers for those comfortable with the technology, it’s not yet a mainstream solution for the average user seeking immediate money transfers.

Key Factors for Choosing Your Immediate Transfer Method

When deciding how to send money immediately, several factors should guide your choice:

- Speed: How critical is instant delivery? “Immediate” can mean minutes, hours, or within the business day, depending on the service.

- Cost: What are the fees for the service, including any instant payout fees or currency conversion charges?

- Security: How secure is the platform? What measures are in place to protect your funds and personal information?

- Transfer Limits: Are there daily, weekly, or monthly limits that might restrict the amount you need to send?

- Recipient’s Access: Does the recipient have a bank account? Do they need cash? Do they use a specific digital wallet or app?

- International vs. Domestic: Different services specialize in different geographies, impacting speed and cost.

- Amount: For very large sums, traditional wires might be preferable due to higher limits and enhanced security protocols. For small amounts, P2P apps are usually best.

Best Practices for Secure and Successful Immediate Transactions

No matter the method, adhering to best practices ensures your immediate transfer is both swift and secure:

- Double-Check Recipient Details: This is the most crucial step. A single incorrect digit in an account number, email, or phone number can send money to the wrong person, and immediate transfers are often irreversible.

- Verify Recipient Identity: If you’re sending money to someone you don’t know well, especially in response to an urgent request, be wary of scams. Verify the person’s identity through another channel if possible.

- Use Strong Passwords and 2FA: Protect your accounts with robust, unique passwords and enable two-factor authentication (2FA) wherever available.

- Use Secure Networks: Only initiate transfers on secure, private Wi-Fi networks, not public ones, to prevent data interception.

- Understand Fees Upfront: Always review the total cost, including all fees and exchange rates, before confirming a transfer.

- Keep Records: Retain transaction confirmations, reference numbers, and any communication related to the transfer for your records.

- Know Your Limits: Be aware of the sending and receiving limits of your chosen service and your bank.

![]()

The Future of Instant Money Movement

The trajectory of immediate money transfers points towards even greater speed, lower costs, and enhanced interoperability. Real-time payment systems are expanding globally, aiming to connect banks and financial institutions across borders for truly instantaneous international transfers. Innovations in AI and machine learning will further bolster fraud detection and security, making instant transactions even safer. Meanwhile, the integration of biometric authentication (like fingerprint or facial recognition) and advanced encryption will simplify the user experience while maintaining robust security.

The ultimate goal is a seamless, friction-less global financial ecosystem where sending money across town or across the world is as simple and instantaneous as sending a text message, all while maintaining the integrity and security of the financial system. For individuals and businesses alike, understanding the current landscape and embracing best practices will ensure they can always meet the demands for immediate financial solutions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.